Table of Contents

- Why T-Bill Myths Persist in 2025

- Accessibility and Investment Myths

- Safety and Government Backing Concerns

- Comparison with Other Investment Options

- Age and Demographic Misconceptions

- Liquidity and Flexibility Myths

- How to Start Investing in T-Bills Today

- Frequently Asked Questions

Why T-Bill Myths Persist in 2025

The Current T-Bill Opportunity

According to TreasuryDirect.gov, 3-month Treasury Bills are yielding approximately 5.1% as of July 2025—rates not seen since before the 2008 financial crisis. Yet despite these attractive returns, many investors remain on the sidelines due to persistent misconceptions.

Why These Myths Matter

These outdated beliefs cost Americans and Canadians millions in potential earnings. While traditional savings accounts offer 0.01% to 0.6% APY, T-Bills provide government-guaranteed returns that significantly outpace inflation and most “high-yield” savings options.

The Economic Context of 2025

With the Federal Reserve maintaining rates between 5.25-5.50% and inflation at 2.4%, T-Bills offer real returns above inflation—a rare combination of safety and profitability.

Accessibility and Investment Myths

Myth #1: “You Need Thousands to Get Started”

Reality: T-Bills require just $100 minimum investment through TreasuryDirect.gov.

This myth likely stems from the pre-internet era when T-Bills required broker intermediaries with high minimums. Today’s digital platforms have democratized access:

Direct Purchase Options:

- TreasuryDirect.gov: $100 minimum, no fees

- Fidelity: $100 minimum, commission-free

- Vanguard: $1,000 minimum for T-Bills

- Charles Schwab: $1,000 minimum

Real-World Example:

Sarah, a 26-year-old teacher from Phoenix, started with $500 in 4-week T-Bills. After seeing the simple process and guaranteed returns, she now invests $1,000 monthly in a T-Bill ladder, earning over $600 annually in risk-free interest.

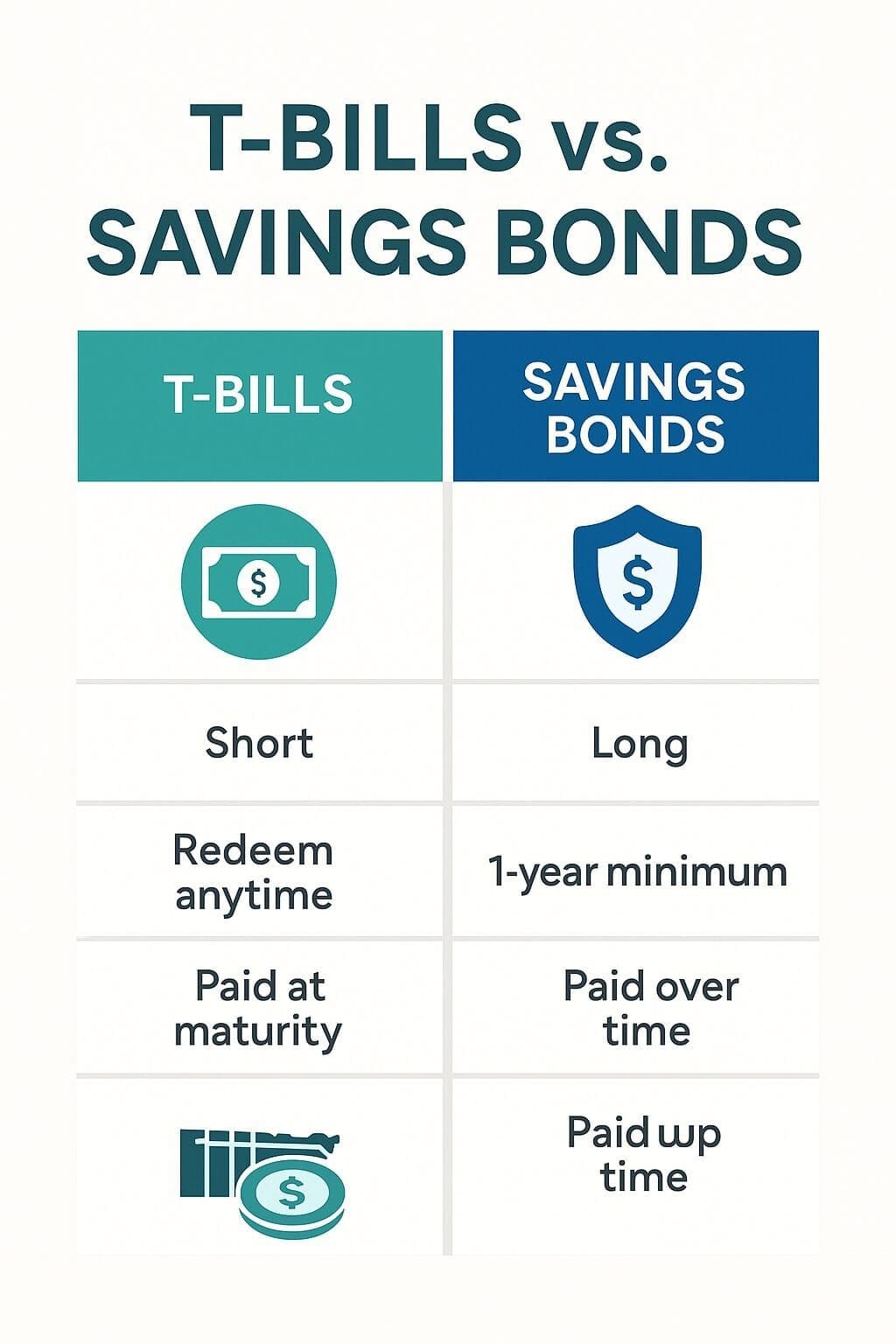

Myth #2: “T-Bills Are Just Like Savings Bonds”

Reality: T-Bills offer much greater flexibility and shorter terms than savings bonds.

| Feature | T-Bills | Series I Bonds | Series EE Bonds |

|---|---|---|---|

| Minimum Term | 4 weeks | 12 months | 12 months |

| Maximum Term | 52 weeks | 30 years | 30 years |

| Early Access | At maturity (4-52 weeks) | After 12 months (with penalty) | After 12 months (with penalty) |

| Purchase Limit | No limit | $10,000 annually | $10,000 annually |

| Interest Rate | Fixed at purchase | Variable (inflation-adjusted) | Fixed (doubles in 20 years) |

Key Difference: T-Bills work like a “financial boomerang”—you buy at a discount and receive full face value at maturity. For example, you might pay $975 for a $1,000 T-Bill maturing in 13 weeks, earning $25 guaranteed profit.

Myth #3: “You Need to Understand Complex Bond Markets”

Reality: Buying T-Bills is simpler than online shopping.

The TreasuryDirect.gov process takes less than 10 minutes:

- Create Account: Basic personal information and bank details

- Choose Term: 4, 8, 13, 17, 26, or 52 weeks

- Enter Amount: Minimum $100, increments of $100

- Submit Purchase: Funds automatically deducted on auction date

- Receive Payment: Full face value deposited at maturity

No complex decisions required: Unlike corporate bonds with credit ratings and varying terms, all T-Bills carry identical government backing regardless of term length.

Safety and Government Backing Concerns

Myth #4: “Can I Really Trust the Government to Pay Me Back?”

Reality: T-Bills are backed by the “full faith and credit” of the U.S. government—the same guarantee that underpins the global financial system.

Historical Track Record:

- Zero defaults: The U.S. Treasury has never missed a T-Bill payment in over 200 years

- Global confidence: Foreign governments hold over $7 trillion in U.S. Treasury securities

- Crisis performance: T-Bills maintained payments through the Great Depression, 2008 financial crisis, and COVID-19 pandemic

What “Full Faith and Credit” Means:

This constitutional guarantee means the U.S. government pledges all its resources—including taxation power—to honor T-Bill obligations. According to the Congressional Budget Office, this makes T-Bills the world’s safest investment.

For Canadian Investors:

While Canadians can’t purchase directly through TreasuryDirect.gov, they can buy U.S. T-Bills through Canadian brokers like TD Direct Investing or RBC Direct Investing, though they should consider currency exchange costs.

Myth #5: “Political Uncertainty Makes T-Bills Risky”

Reality: Political drama actually increases T-Bill demand as investors seek safety.

Recent Examples:

- 2023 Debt Ceiling Crisis: T-Bill demand surged as investors fled riskier assets

- Government Shutdowns: T-Bills continued paying on schedule

- Election Volatility: T-Bills provide stability during political uncertainty

Why Politics Don’t Matter:

T-Bill payments are considered “mandatory spending” under federal law, meaning they continue regardless of political gridlock or government shutdowns.

Comparison with Other Investment Options

Myth #6: “High-Yield Savings Accounts Are Better”

Reality: T-Bills currently offer higher, guaranteed rates compared to most savings accounts.

July 2025 Rate Comparison:

- 3-Month T-Bills: 5.1% (guaranteed)

- Best High-Yield Savings: 4.4% (variable)

- Average Savings Account: 0.6% (variable)

- Traditional Bank Savings: 0.01% (variable)

Key Advantages of T-Bills:

- Rate Lock: Your rate is guaranteed for the full term

- No Bank Risk: Government backing vs. FDIC insurance limits

- Tax Benefits: State tax-free in most states

- No Fees: No monthly maintenance or transaction fees

When Savings Accounts Win:

- Daily liquidity needs

- Amounts under $1,000

- Frequent access requirements

Real-World Scenario:

Mark from Toronto had $25,000 in a “high-yield” savings account earning 3.8%. He moved to a T-Bill ladder earning 5.1%, increasing his annual income by $325 with the same safety level.

Myth #7: “T-Bills Only Make Sense When Inflation Is High”

Reality: T-Bills provide value in any environment where they beat inflation and alternative safe investments.

Current Environment Analysis (July 2025):

- Inflation Rate: 2.4% (CPI)

- T-Bill Rate: 5.1%

- Real Return: 2.7% above inflation

Historical Context:

Even during low inflation periods (2010-2020), T-Bills consistently outperformed savings accounts and provided positive real returns during most years.

Future Rate Considerations:

If the Federal Reserve cuts rates in late 2025 as expected, T-Bills purchased now lock in current high rates, while savings account rates will drop immediately.

Age and Demographic Misconceptions

Myth #8: “T-Bills Are Only for Retirees”

Reality: Younger investors are increasingly using T-Bills for strategic cash management and goal-based saving.

Millennial and Gen Z Use Cases:

Emergency Fund Optimization

Traditional Approach: $15,000 in 0.6% savings account = $90 annual interest

T-Bill Approach: $15,000 in rolling 13-week T-Bills = $765 annual interest

Difference: $675 extra per year with same liquidity

Home Down Payment Strategy

Case Study: Jessica and Ryan, both 29, saving for a $100,000 down payment

- Timeline: 18 months

- Strategy: 6-month T-Bill ladder with $5,000 monthly purchases

- Result: Extra $2,400 in interest compared to savings account

Investment Bridge Strategy

Scenario: Waiting for stock market opportunities

- Problem: Keeping cash in low-yield savings while researching investments

- Solution: 4-week T-Bills for maximum flexibility with 5%+ returns

- Benefit: Earn substantial interest while maintaining quick access

Modern T-Bill Strategies by Age Group

Ages 20-30: Building Foundation

- Emergency fund optimization

- Short-term goal funding (car, wedding, travel)

- Investment opportunity cash

Ages 30-40: Wealth Building

- Home down payment accumulation

- Business opportunity funds

- Portfolio diversification

Ages 40-50: Risk Management

- College savings (short-term component)

- Career transition funds

- Market volatility protection

Ages 50+: Capital Preservation

- Retirement income ladders

- Estate planning liquidity

- Healthcare expense reserves

Liquidity and Flexibility Myths

Understanding T-Bill Liquidity

Myth: “T-Bills Lock Up Your Money Like CDs”

Reality: T-Bills offer predictable, short-term commitments with no early withdrawal penalties.

Liquidity Comparison:

| Investment | Early Access | Penalty | Typical Terms |

|---|---|---|---|

| T-Bills | At maturity only | None | 4-52 weeks |

| CDs | Early withdrawal allowed | 3-12 months interest | 6 months – 5 years |

| Savings Bonds | After 12 months | 3 months interest | Up to 30 years |

| Savings Account | Anytime | None | Ongoing |

The T-Bill Ladder Strategy

How It Works:

Instead of investing all money in one T-Bill, create a “ladder” with staggered maturity dates.

Example 12-Week Ladder with $12,000:

- Week 1: Buy $3,000 in 4-week T-Bills

- Week 2: Buy $3,000 in 4-week T-Bills

- Week 3: Buy $3,000 in 4-week T-Bills

- Week 4: Buy $3,000 in 4-week T-Bills

Result: Starting in week 5, $3,000 matures every week, providing regular liquidity while maintaining 5%+ returns.

Emergency Access Strategies

For True Emergencies:

- Keep 1-2 months expenses in instant-access savings

- Use T-Bill ladders for remaining emergency fund

- Consider money market funds for intermediate liquidity

Secondary Market Option:

While not recommended for beginners, T-Bills can be sold before maturity through brokers, though this may result in gains or losses based on interest rate changes.

How to Start Investing in T-Bills Today

Step-by-Step Getting Started Guide

Option 1: TreasuryDirect.gov (Recommended for Beginners)

Account Setup (5 minutes):

- Visit TreasuryDirect.gov

- Click “Open an Account”

- Provide SSN, driver’s license, and bank account details

- Verify identity through security questions

- Receive account confirmation email

Making Your First Purchase:

- Log into your account

- Select “BuyDirect” tab

- Choose “Bills” from security types

- Select term length (start with 13 weeks)

- Enter purchase amount ($100 minimum)

- Review and submit order

Important Dates:

- Auction Date: When your order is processed

- Issue Date: When payment is deducted (usually next business day)

- Maturity Date: When you receive full face value

Option 2: Brokerage Accounts

Best for: Investors with existing brokerage relationships

Top Options:

- Fidelity: $100 minimum, no fees, excellent research tools

- Charles Schwab: $1,000 minimum, comprehensive platform

- Vanguard: $1,000 minimum, low-cost focus

- TD Ameritrade: $1,000 minimum, advanced trading tools

Tax Considerations

U.S. Tax Treatment

- Federal Tax: T-Bill interest is taxable as ordinary income

- State Tax: Generally exempt from state and local taxes

- Reporting: Interest reported on Form 1099-INT

Canadian Tax Treatment

- Income Tax: T-Bill interest taxable as foreign income

- Currency Conversion: Must convert USD gains to CAD

- Reporting: Report on T1135 if total foreign assets exceed $100,000 CAD

Building Your T-Bill Strategy

Conservative Approach (Beginners)

- Start with $500-1,000

- Choose 13-week terms initially

- Reinvest at maturity to build familiarity

- Gradually increase amounts as comfort grows

Aggressive Approach (Experienced)

- Implement T-Bill ladders immediately

- Use multiple term lengths for optimization

- Consider tax-loss harvesting strategies

- Integrate with broader investment portfolio

Frequently Asked Questions

What happens if I need my money before the T-Bill matures?

T-Bills cannot be redeemed early through TreasuryDirect.gov. However, you can sell them in the secondary market through a broker, though this may result in gains or losses depending on interest rate changes since purchase. For emergency access, consider keeping some funds in high-yield savings accounts alongside your T-Bill investments.

How do T-Bill returns compare to inflation in 2025?

With current 3-month T-Bills yielding 5.1% and inflation at 2.4%, T-Bills provide a real return of approximately 2.7% above inflation. This is exceptional for a risk-free investment and significantly better than most savings accounts, which typically offer negative real returns after inflation.

Can Canadians invest in U.S. Treasury Bills?

Yes, but not directly through TreasuryDirect.gov. Canadians can purchase U.S. T-Bills through Canadian brokers like TD Direct Investing, RBC Direct Investing, or Interactive Brokers. Consider currency exchange costs and tax implications, as T-Bill interest is taxable in Canada as foreign income.

What’s the difference between T-Bills and T-Notes?

T-Bills mature in one year or less and are sold at a discount to face value. T-Notes mature in 2-10 years and pay semi-annual interest. For most individual investors seeking short-term, safe returns, T-Bills are more appropriate due to their shorter commitment and simpler structure.

How often are T-Bill auctions held?

The U.S. Treasury holds T-Bill auctions weekly:

- 4-week T-Bills: Every Tuesday

- 8-week T-Bills: Every Tuesday

- 13-week T-Bills: Every Monday

- 26-week T-Bills: Every Monday

- 52-week T-Bills: Every fourth Tuesday

This frequent schedule provides flexibility to invest regularly and take advantage of rate changes.

Are T-Bill gains guaranteed?

Yes, if held to maturity. The U.S. government guarantees you’ll receive the full face value at maturity. Your return is determined at purchase and cannot change. However, if you sell before maturity in the secondary market, gains or losses depend on current interest rates.

Should I choose T-Bills over high-yield savings accounts?

It depends on your needs:

Choose T-Bills if:

- You can commit funds for 4-52 weeks

- You want guaranteed, locked-in rates

- You prefer government backing over FDIC insurance

- You want to avoid bank fees

Choose high-yield savings if:

- You need daily access to funds

- You’re building an emergency fund under $5,000

- You prefer the simplicity of one account

- You want to avoid any commitment periods

How do rising or falling interest rates affect T-Bills?

If you hold to maturity: Interest rate changes don’t affect your return—you receive exactly what was promised at purchase.

If you sell early: Rising rates decrease T-Bill values (you might lose money), while falling rates increase values (you might gain money). This is why most investors hold T-Bills to maturity.

For future purchases: Rising rates mean higher returns on new T-Bills, while falling rates mean lower returns on new purchases.

Want to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- 6 Financial Strategies to Protect Your Wealth

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- 8 Powerful Financial Strategies Every Single Person Should Know

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

Keep exploring — your smartest financial years are just getting starte

Sources:

- TreasuryDirect.gov – Treasury Bills

- Federal Reserve Economic Data

- Bureau of Labor Statistics – Consumer Price Index

- Congressional Budget Office

- Federal Reserve Monetary Policy

- IRS Publication 550 – Investment Income and Expenses

- Canada Revenue Agency – Foreign Income

- FDIC Deposit Insurance Coverage

- Fidelity Treasury Bills Information

- Vanguard Treasury Securities

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Treasury Bill rates and terms are subject to change based on market conditions and government policy. Always verify current rates and terms directly with TreasuryDirect.gov or your chosen financial institution before making investment decisions. Consider consulting with a qualified financial advisor for personalized guidance.