The 2024–2025 FAFSA overhaul marks the most significant transformation in federal student aid in decades. For students and families across America, understanding these changes is crucial for maximizing college affordability and minimizing stress. This comprehensive guide will walk you through the new FAFSA, explain its impact, and provide actionable steps to help you secure the financial aid you deserve.

Table of Contents

- What Is FAFSA and Why the Changes Now?

- A Brief History of FAFSA and Its Challenges

- Key FAFSA Changes for 2024–2025

- Student Aid Index (SAI) vs. Expected Family Contribution (EFC)

- Impact on Pell Grants

- Real-World Examples and Case Studies

- Who Stands to Gain—and Who Might Lose

- Action Steps for Students and Parents

- FAQs

- Final Thoughts

What Is FAFSA and Why the Changes Now?

The Free Application for Federal Student Aid (FAFSA) is the primary gateway to federal grants, low-interest loans, and work-study programs. Each year, over 17 million students fill out the FAFSA, but for many, the process has been daunting. The old form had over 100 questions, confusing language, and a formula (the Expected Family Contribution, or EFC) that few understood.

Recognizing these barriers, Congress passed the FAFSA Simplification Act in 2020, aiming to make the process more accessible, transparent, and fair. The changes, fully implemented for the 2024–2025 academic year, are designed to help more students—especially those from low- and middle-income families—get the aid they need.

A Brief History of FAFSA and Its Challenges

Since its introduction in 1992, the FAFSA has been a critical tool for opening doors to higher education. However, the complexity of the form has long been criticized. According to a 2022 NASFAA report, nearly 2 million eligible students failed to complete the FAFSA each year, leaving billions in aid unclaimed. Many families, especially those with limited English proficiency or first-generation college students, found the process overwhelming.

In my experience as a college counselor, I’ve seen students abandon the application halfway through, not because they weren’t eligible, but because the process felt insurmountable. This overhaul is a direct response to those stories.

Key FAFSA Changes for 2024–2025

The new FAFSA brings several major updates:

- Fewer Questions: The number of questions is reduced from 108 to as few as 36 for many applicants, focusing only on what truly matters.

- Student Aid Index (SAI): The EFC is replaced by the SAI, a more transparent and equitable measure of a family’s ability to pay.

- IRS Direct Data Exchange (DDX): Families now authorize the IRS to transfer tax data directly, reducing errors and paperwork.

- Revised Family Size and Sibling Rules: The new formula no longer provides extra aid for families with multiple children in college.

- Expanded Pell Grant Access: More students with lower incomes will automatically qualify for the maximum Pell Grant.

- Mobile-Friendly Design: The form is now easier to complete on smartphones and tablets, closing the digital divide.

For a detailed breakdown of every change, visit the official Federal Student Aid update page.

Student Aid Index (SAI) vs. Expected Family Contribution (EFC)

The EFC was a black box for most families. The new SAI is designed to be clearer and more accurate. Here’s how they compare:

| Feature | EFC (Old) | SAI (New) |

|---|---|---|

| Range | 0 to 99,999+ | -1,500 to 9,999+ |

| Negative Values | No | Yes (increases aid eligibility) |

| Sibling Discount | Yes | No |

| Tax Data | Manual entry | IRS DDX import |

| Pell Grant Trigger | Partial (low EFC) | Automatic if SAI ≤ 0 |

This new index means that the neediest students (those with negative SAI) will automatically qualify for the highest possible aid, while middle-income families may see less benefit if they have multiple children in college.

Impact on Pell Grants

The Pell Grant is the backbone of federal need-based aid. For 2024–2025, the maximum Pell Grant is $7,395 (source). Under the new rules:

- Students with an SAI ≤ 0 automatically receive the maximum grant.

- Eligibility is now based on SAI and household size, not the number of siblings in college.

- More than 610,000 additional students are expected to qualify for Pell Grants under the new rules (Department of Education).

For many low-income and independent students, this change is a game-changer, making college more attainable than ever before.

Real-World Examples and Case Studies

Case Study 1: Single-Parent Family

Maria is a single mother in Texas with two children. Under the old FAFSA, she had to enter detailed tax information and hope that having two kids in college would boost her aid. With the new FAFSA, she authorizes IRS DDX, answers fewer questions, and her negative SAI qualifies both children for the maximum Pell Grant. The process takes less than 30 minutes, and she receives clear guidance from the new interface.

Case Study 2: Middle-Class Family with Multiple Children

The Johnsons, a family in Ohio with three kids in college, used to benefit from the sibling discount. Now, with the SAI formula, they see a higher expected contribution. While their oldest still qualifies for some aid, the total family award is lower than in previous years. They consult their financial aid office for additional institutional scholarships.

Case Study 3: Independent Student

Jamal, a 22-year-old foster youth, always struggled with dependency questions. The new FAFSA’s streamlined criteria make it clear he qualifies as independent. His negative SAI secures him the full Pell Grant and additional state aid, allowing him to focus on his studies rather than paperwork.

Who Stands to Gain—and Who Might Lose

Winners

- Low-Income Students: Negative SAI means maximum aid, less paperwork, and faster results.

- Independent Students: Foster youth, wards of the court, and those with special circumstances benefit from clearer rules.

- Mobile-First Users: The new design helps students who rely on smartphones or tablets.

Potentially at Risk

- Middle-Income Families with Multiple Children: Loss of sibling discount may reduce total aid.

- Parents Who Decline IRS DDX: Without tax data sharing, aid eligibility may be lost.

- Late Filers: State and institutional deadlines still matter—file early to maximize your options.

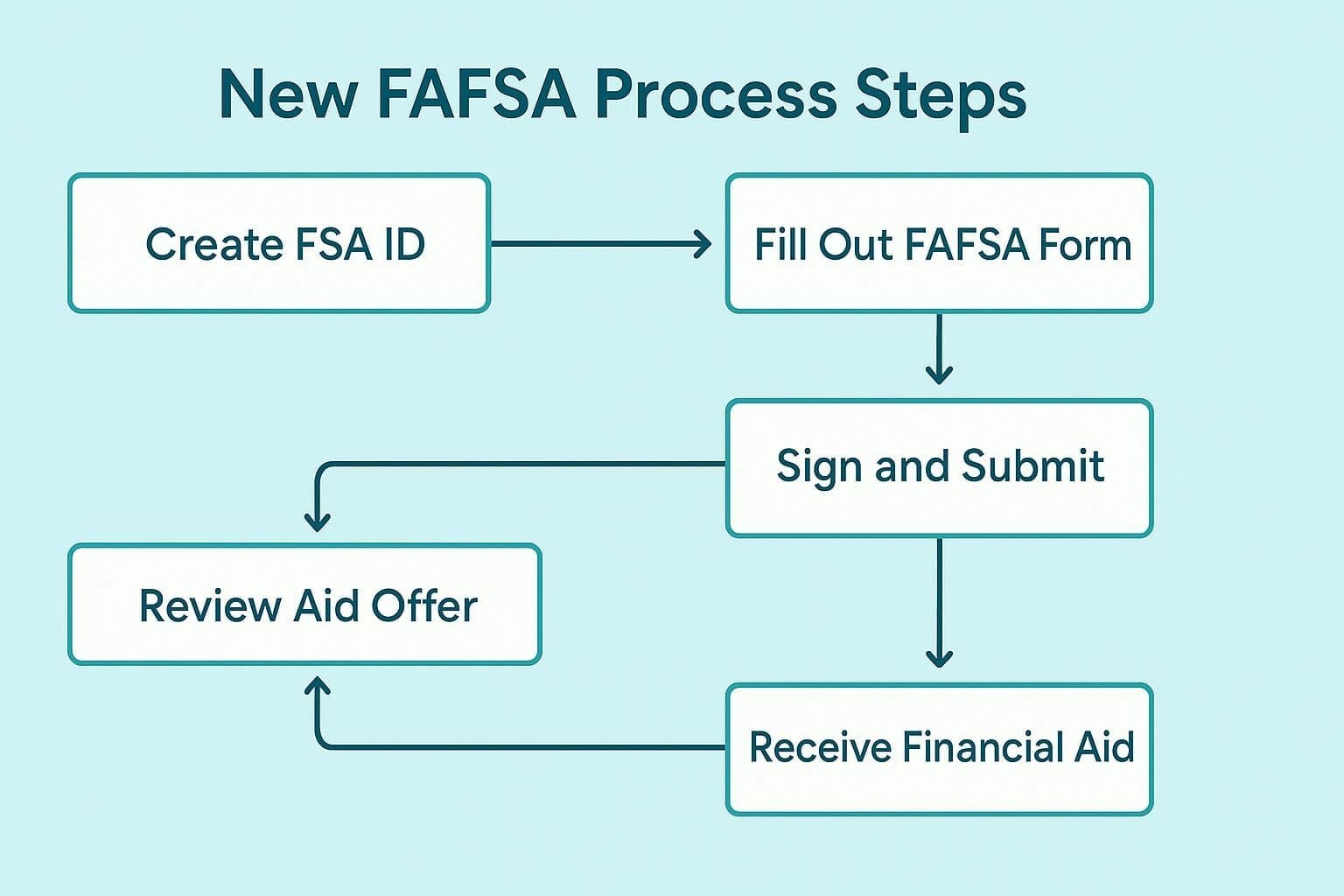

Action Steps for Students and Parents

- Create FSA IDs: Both student and parent must register at studentaid.gov.

- Gather 2023 Tax Returns: Have tax documents ready for IRS DDX.

- Review Household Size: Only dependents you support count under new rules.

- Use the FAFSA Estimator: Preview your SAI at the Federal Student Aid estimator.

- File Early: FAFSA opens October 1, 2024—apply as soon as possible to maximize state and college aid.

- Consult Financial Aid Offices: Every college may have unique deadlines and extra scholarship opportunities.

- Monitor SAI Updates: Check your FAFSA portal for real-time changes and updates.

FAQs

What if parents refuse IRS data sharing?

Most federal aid requires DDX. Without it, your FAFSA may be incomplete and you risk losing eligibility.

Do scholarships still use FAFSA?

Yes—most institutional and state scholarships reference FAFSA data, so a lower SAI often unlocks more aid.

How does FAFSA treat divorced parents?

Only the parent providing the majority of financial support reports income, regardless of custody.

Are 529 plans assessed?

Parent-owned 529s are assessed at up to 5.64% of their value in the SAI formula.

Can I appeal my award?

Yes. Document life changes (job loss, medical bills) and request a review from your school’s aid office.

Does household net worth matter?

Retirement accounts and home equity are excluded, minimizing impact for most families.

What about part-time students?

Part-time students qualify for Pell, prorated by credit load, and may access state aid separately.

Is there an application fee?

No—FAFSA is always free. Never pay third parties to file.

Will future changes occur?

Congress reviews FAFSA rules biennially; stay informed via studentaid.gov.

Final Thoughts

The 2024–2025 FAFSA redesign is a long-awaited step toward equity and simplicity in college funding. While some families may lose out on sibling discounts, the overall result is greater access for those who need it most. By understanding the new SAI, leveraging IRS DDX, and filing early, you’ll give yourself the best chance at the aid you deserve.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. For personalized guidance, consult a certified financial advisor or your school’s financial aid office.

Want to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- 6 Financial Strategies to Protect Your Wealth

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- 8 Powerful Financial Strategies Every Single Person Should Know

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

Keep exploring — your smartest financial years are just getting started.

Sources: