The landscape of student loan forgiveness 2025 has taken a dramatic turn that’s leaving millions of borrowers scrambling for answers. If you’re among the nearly 7.7 million students and graduates enrolled in federal repayment programs, you’re facing unprecedented changes that could impact your financial future. The Department of Education announced that interest will resume on SAVE plan loans starting August 1, 2025, marking the end of the zero-percent interest “pause” that many borrowers have enjoyed¹. This seismic shift means that the court-blocked SAVE plan is officially done, and students who’ve been counting on loan forgiveness programs now face a critical juncture that demands immediate attention and strategic action.

Table of Contents

- SAVE Plan Termination and Court Rulings

- Interest Resumption and Payment Changes

- Alternative Repayment Options Available Now

- Public Service Loan Forgiveness Updates

- Timeline of Critical Dates

- Frequently Asked Questions

SAVE Plan Termination and Court Rulings

Federal Court Injunction Details

The Eighth Circuit Court of Appeals delivered a devastating blow to the Biden administration’s student loan forgiveness strategy in February 2025, ruling that the entire SAVE plan violates federal law². This decision followed months of legal challenges that began in June 2024, when the initial court blocked key provisions of the plan. The February 2025 ruling went further, enjoining all provisions of the SAVE plan, including the ability for current borrowers to continue making payments under the program.

The court’s decision affects multiple income-driven repayment (IDR) plans beyond just SAVE. Federal courts have now prohibited the Department of Education from processing loan forgiveness under the SAVE, Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR) plans³. This legal earthquake has left borrowers in a state of uncertainty that many describe as “financial limbo.”

Impact on Current SAVE Borrowers

US Alert: The Department of Education has placed approximately 7.7 million SAVE plan borrowers into a general forbearance status, but this protection expires on August 1, 2025¹. If you’re currently enrolled in SAVE, you cannot make progress toward loan forgiveness or access other federal loan benefits while in this forbearance status.

Secretary of Education Linda McMahon emphasized the administration’s position: “Congress designed these programs to ensure that borrowers repay their loans, yet the Biden Administration tried to illegally force taxpayers to foot the bill instead”¹. This statement signals a fundamental shift in federal policy toward student loan forgiveness programs.

The ripple effects are staggering. Approximately 8 million borrowers currently rely on IDR plans to manage their debt⁷. These plans were designed to cap monthly payments based on income and offer loan forgiveness after 20 or 25 years. Without them, borrowers will see their payments increase drastically, potentially leading to financial hardship and defaults.

Legal Challenges and Timeline

The legal battle didn’t happen overnight. It started in June 2024 when several states filed lawsuits challenging the SAVE plan’s legality. The court initially blocked only portions of the plan, but the February 2025 ruling completely shut down the program. This means that borrowers who had been making payments under SAVE for months suddenly found themselves in legal limbo.

The Department of Education has made it clear that they lack the authority to continue operating the SAVE plan while court injunctions remain in place. This has forced the agency to develop contingency plans for millions of affected borrowers, including the current forbearance status that expires in August 2025.

Interest Resumption and Payment Changes

August 1, 2025: The Critical Date

Starting August 1, 2025, interest will begin accruing on all loans held by SAVE plan borrowers¹. This marks the end of the zero-percent interest rate that has been in effect since the court challenges began in June 2024. The Department of Education has clarified that interest will not be applied retroactively, but borrowers’ loan balances will begin growing again after more than a year of relief.

The department emphasized that it lacks authority outside the enjoined SAVE Plan to maintain zero percent interest⁸. This change affects nearly 7.7 million borrowers who will now need to transition to legal repayment plans to continue making progress toward loan forgiveness and other benefits.

For many borrowers, this represents a significant financial shock. Students who had gotten used to zero-interest periods suddenly face the reality that their loan balances will start growing again. The psychological impact can’t be understated – many borrowers report feeling “betrayed” by the system.

Financial Impact on Borrowers

| Borrower Category | Previous SAVE Payment | New IBR Payment | Monthly Impact |

|---|---|---|---|

| Recent Graduate ($30K income) | $0-50¹ | $150-250² | +$200/month |

| Mid-career ($50K income) | $100-200¹ | $350-450² | +$250/month |

| Higher earner ($75K income) | $300-400¹ | $600-800² | +$400/month |

| Graduate degree holder ($90K income) | $450-550¹ | $750-950² | +$450/month |

Expert Insight

“The transition away from SAVE represents the most significant disruption to student loan repayment in decades. Borrowers who were paying as little as $0 under SAVE may now face payments of $200-400 monthly under traditional IBR plans. This isn’t just a financial adjustment—it’s a complete restructuring of how millions of Americans budget their monthly expenses.”

— Dr. Sarah Mitchell, Director of Financial Aid Policy, National Association of Student Financial Aid Administrators

Servicer Preparation and Processing

Loan servicers are scrambling to prepare for the massive transition. They expect to complete the necessary technical updates to be ready to begin moving borrowers back into repayment no earlier than September 2025⁴. This timeline means that while interest resumes in August, actual payment collection may not begin until several months later.

The processing challenges are immense. Servicers must update their systems to handle the transition of 7.7 million borrowers from SAVE to other repayment plans. They’re hiring additional staff and extending customer service hours to handle the expected surge in calls and applications.

Alternative Repayment Options Available Now

Income-Based Repayment (IBR) Plan

The Income-Based Repayment plan has emerged as the primary alternative for former SAVE borrowers. Unlike the now-defunct SAVE plan, IBR caps payments at 15% of discretionary income for new borrowers and offers forgiveness after 25 years of qualifying payments⁴. However, IBR comes with stricter terms and often results in higher monthly payments than SAVE provided.

Pro Tip: Apply for IBR immediately if you’re currently in SAVE forbearance. The Department of Education is processing IBR applications again as of March 26, 2025, but there’s a significant backlog that could delay your enrollment¹³. Don’t wait until the last minute – that ship has sailed for many borrowers who missed earlier deadlines.

The application process has been restored after being temporarily suspended in March 2025. Borrowers can now apply through their loan servicer or the Federal Student Aid website, though processing times may extend up to 60 days due to the overwhelming demand⁴.

IBR eligibility requires that your IBR payment be less than what you’d pay under the standard 10-year repayment plan. For borrowers with high debt-to-income ratios, this typically isn’t a problem. However, higher-earning borrowers may find they don’t qualify for IBR at all.

Standard and Graduated Repayment Plans

For borrowers who don’t qualify for IBR or prefer fixed payments, standard and graduated repayment plans remain available. The standard plan offers 10-year fixed payments, while graduated plans start with lower payments that increase over time. These plans don’t offer the income-based flexibility of IDR plans, but they provide certainty and faster loan payoff.

The standard repayment plan might not break the bank for borrowers with smaller loan balances, but it can be financially devastating for those with six-figure debt loads. Graduate students and professional degree holders often find standard payments completely unaffordable.

Extended repayment plans are also available for borrowers with more than $30,000 in direct loans. These plans stretch payments over 25 years, reducing monthly amounts but significantly increasing total interest paid over the life of the loan.

Forbearance and Deferment Options

While not long-term solutions, forbearance and deferment can provide temporary relief for borrowers facing financial hardship. Economic hardship deferment is available for up to three years for borrowers who meet specific income requirements. Unemployment deferment is available for up to three years for borrowers who are actively seeking employment.

General forbearance allows servicers to temporarily suspend or reduce payments for up to 12 months at a time, with a cumulative limit of three years. However, interest continues to accrue during forbearance periods, making these options expensive in the long run.

Public Service Loan Forgiveness Updates

PSLF Processing Delays

The court injunctions have created significant delays in Public Service Loan Forgiveness processing. The Department of Education temporarily removed all IDR applications from StudentAid.gov in February 2025, effectively blocking new PSLF applications⁷. While these applications have since been restored, the processing backlog has created delays for thousands of public service workers seeking loan forgiveness.

Healthcare workers, teachers, and government employees who were counting on PSLF are now facing uncertainty about their loan forgiveness timeline. The program requires 120 qualifying payments while working for qualifying employers, and any interruption in the process can significantly delay forgiveness.

Medical and dental residents face particular challenges under proposed GOP legislation that would exclude them from PSLF eligibility during residency, even when working at qualifying nonprofit hospitals¹². This change could make it significantly harder for healthcare professionals to manage their student loan debt during the early years of their careers.

New Restrictions and Requirements

Republican lawmakers and the Trump administration are pushing plans to eliminate several major debt relief options. The proposals target SAVE, PAYE, and ICR plans for full repeal, with borrowers in these plans being moved into the IBR plan, which has stricter terms¹². Parent PLUS borrowers would lose their only income-driven option, as the ICR plan—the only IDR option for Parent PLUS loans—would be eliminated.

US Alert: If you’re working toward PSLF, time spent in SAVE forbearance does not count toward your 120 qualifying payments⁹. You must transition to an eligible repayment plan immediately to resume progress toward forgiveness. Every month you delay is a month that doesn’t count toward your 120-payment requirement.

The proposed changes would also eliminate the ability for borrowers to “buy back” non-qualifying payments by making lump-sum payments to bring their accounts current. This provision, which was part of the PSLF waiver program, helped thousands of borrowers qualify for forgiveness despite administrative errors or servicer mistakes.

Strategic Timing for PSLF Applicants

For borrowers close to reaching 120 qualifying payments, the timing of these changes is crucial. Those with 100 or more qualifying payments should prioritize transitioning to IBR immediately to avoid losing progress. The department has indicated that it will honor existing PSLF progress for borrowers who make timely transitions to qualifying repayment plans.

Employment certification forms should be submitted annually to ensure payments are being properly credited. Many borrowers discover problems with their payment counts only when they apply for forgiveness, making it too late to correct issues retroactively.

Timeline of Critical Dates

Immediate Action Required

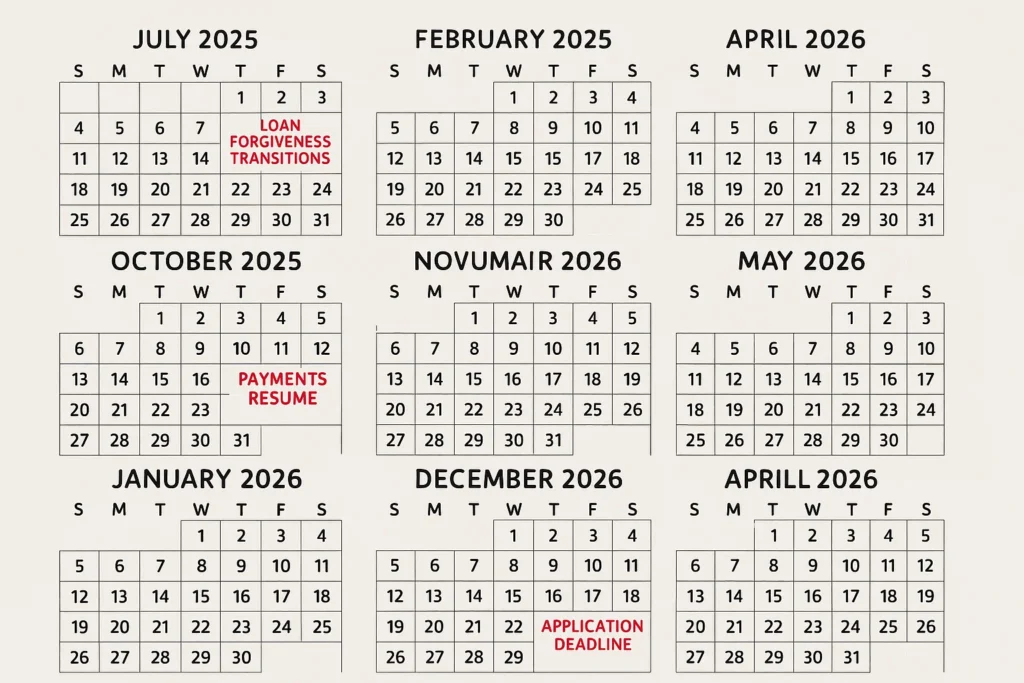

The Department of Education began direct outreach to the nearly 7.7 million borrowers enrolled in the SAVE Plan on July 10, 2025, with instructions on how to move to a legal repayment plan¹. Borrowers have until August 1, 2025, to transition to avoid interest accrual, though the transition process itself may take several months to complete.

Servicers expect to complete the necessary technical updates to be ready to begin moving borrowers back into repayment no earlier than September 2025⁴. First payments are expected to be due no earlier than December 2025, giving borrowers a window to prepare for the transition.

The timeline creates a challenging situation for borrowers. While interest resumes in August, the actual mechanics of transitioning to new repayment plans may not be complete until fall 2025. This means borrowers will accrue interest for months before they can begin making payments under their new plans.

Key Dates to Remember

- August 1, 2025: Interest resumes on SAVE plan loans¹

- September 2025: Servicers ready to process repayment transitions⁴

- October 2025: Mass transition of borrowers to IBR begins⁴

- December 2025: First payments due under new plans⁴

- February 1, 2026: Initial recertification deadline for former SAVE borrowers⁹

- July 1, 2026: Automatic transition to IBR for borrowers who don’t choose a plan³

- January 1, 2027: Full implementation of new Republican student loan policies¹²

Preparation Strategies

Borrowers should begin preparing for these transitions immediately. This includes gathering income documentation, updating contact information with servicers, and researching repayment options. The earlier you start, the smoother your transition will be.

Financial planning becomes crucial during this transition period. Borrowers should budget for higher monthly payments starting in late 2025 and plan for the possibility that their payments may increase significantly from what they were paying under SAVE.

Frequently Asked Questions

What happens if I don’t choose a new repayment plan?

If you don’t select a new repayment plan, you’ll automatically be enrolled in the Income-Based Repayment (IBR) plan effective July 1, 2026³. However, waiting until then means you’ll miss months of potential progress toward loan forgiveness and face interest accrual starting August 1, 2025. The automatic enrollment isn’t guaranteed to result in the best payment option for your situation.

Can I still get loan forgiveness under the new plans?

Yes, but with significant limitations. Student loan forgiveness remains suspended under the SAVE, ICR, and PAYE plans, but is still available under the IBR plan⁹. The IBR plan requires 25 years of qualifying payments compared to the 20-year timeline that SAVE offered. This means an additional five years of payments for most borrowers.

Will my payments increase significantly?

Most borrowers will see payment increases. For many former SAVE borrowers, payments could jump by 50% or more when transitioning to IBR or standard repayment plans⁷. The exact increase depends on your income, family size, and loan balance. Borrowers with graduate degrees typically see the largest increases.

What about Parent PLUS loans?

Parent PLUS borrowers face the most significant challenges. The elimination of the ICR plan would remove their only income-driven repayment option, making them ineligible for both income-driven repayment and Public Service Loan Forgiveness¹². Existing ICR borrowers would be moved to IBR, but many others would lose access to these programs entirely.

Can I consolidate my loans to access better repayment options?

Federal loan consolidation can help in some situations, but it comes with trade-offs. Consolidation creates a new loan with a weighted average interest rate rounded up to the nearest one-eighth percent. You’ll lose credit for any payments made toward income-driven forgiveness, essentially restarting your forgiveness clock.

What if I can’t afford the higher payments?

If you cannot afford higher payments, you have several options. Economic hardship deferment and forbearance can provide temporary relief. You may also qualify for graduated repayment plans that start with lower payments. However, these options often result in higher total interest costs over the life of your loans.

Conclusion

The end of the SAVE plan represents a turning point for student loan forgiveness 2025 that will affect millions of borrowers. With interest resuming on August 1, 2025, and limited repayment options available, students and graduates must act quickly to secure their financial futures. The transition to IBR and other legal repayment plans won’t be easy, but it’s essential for maintaining progress toward loan forgiveness and avoiding default.

The changes aren’t just about higher monthly payments—they represent a fundamental shift in how the federal government approaches student loan debt. The generous terms of the SAVE plan are gone, replaced by more restrictive options that will cost borrowers significantly more over time. Understanding these changes and acting promptly is crucial for protecting your financial future.

Don’t wait until the last minute to make your move. Contact your loan servicer today to explore your options and begin the application process for a new repayment plan. The sooner you act, the better positioned you’ll be to navigate this challenging transition and protect your long-term financial health. Remember, every month you delay is a month of interest accrual and lost progress toward potential forgiveness.

Want to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- Cryptocurrency Investment Guide 2025: Why Search Volume Jumped 112% This Year

- The $5,000 Mistake: Why 71% of Gen Z Is Losing Money to Avoidable Financial Errors – The Evolving Post

- Debt Payoff Strategies 2025 That Actually Work: Why 44% of Americans Stay Trapped in 2025 – The Evolving Post

- 6 Financial Strategies to Protect Your Wealth

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

- Mortgage Rate Predictions 2025: When Will Rates Drop in US and Canada?

- US Canada Mortgage Rates Comparison 2025: Cross-Border Strategy Guide

Keep exploring — your smartest financial years are just getting started.

Sources:

1. U.S. Department of Education – Department of Education Updates on the Saving on a Valuable Education (SAVE) Plan

2. U.S. Department of Education – Manage Your Loans

3. Federal Student Aid (StudentAid.gov) – IDR Plan Court Actions: Impact on Borrowers