Your emergency fund might not be as secure as you think. With inflation eating away at purchasing power, many Americans are discovering that their carefully saved financial cushions won’t stretch as far as expected during actual emergencies. The need for an accurate emergency fund calculator inflation 2025 has never been more critical, especially for millennials and Gen Z adults who are building their financial foundations during uncertain economic times. Recent Federal Reserve data reveals that 37% of adults would struggle to cover a $400 emergency expense¹, while the FDIC emphasizes that traditional emergency fund guidelines may no longer provide adequate protection against today’s economic realities². This comprehensive guide will help you calculate exactly how much you need to save, account for inflation’s impact on your emergency fund, and ensure your financial safety net remains strong regardless of economic turbulence. Don’t let inflation catch you off guard – it’s time to recalculate your emergency fund strategy.

Table of Contents

- Understanding Emergency Fund Inflation Impact

- Emergency Fund Calculator Inflation 2025 Methodology

- Federal Reserve Emergency Fund Guidelines

- Building Your Inflation-Proof Emergency Fund

- Common Emergency Fund Mistakes to Avoid

- Try our Inflation Calculator

- Frequently Asked Questions

Understanding Emergency Fund Inflation Impact

The Hidden Cost of Inflation on Savings

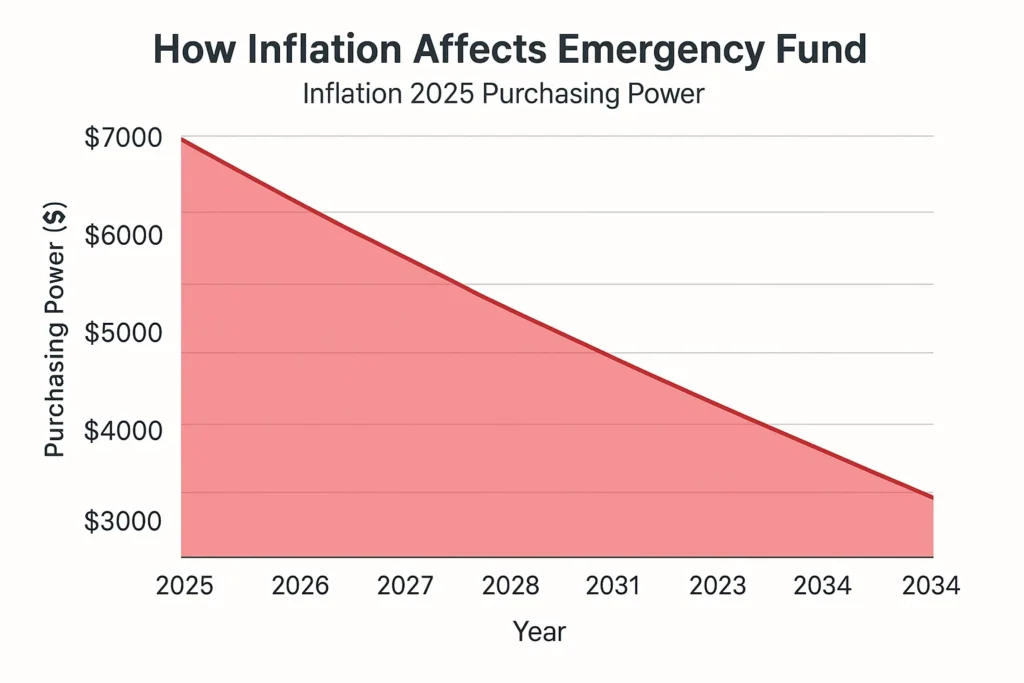

Inflation doesn’t just affect your grocery bill – it’s silently eroding the purchasing power of your emergency fund. According to the Federal Reserve’s 2024 Survey of Household Economics and Decisionmaking, released in May 2025, families are increasingly concerned about their ability to handle unexpected expenses as living costs continue to rise². The reality is that an emergency fund that seemed adequate two years ago may now fall short of covering the same expenses.

Consider this: if you saved $10,000 for emergencies in 2022, that same amount today has significantly less purchasing power due to cumulative inflation. Healthcare costs, housing expenses, and basic necessities have all increased, meaning your emergency fund needs to be larger just to maintain the same level of financial protection.

Current Economic Landscape for Emergency Funds

The Federal Reserve’s latest data paints a concerning picture of American financial preparedness. A staggering 37% of adults would have difficulty covering a $400 emergency expense¹, highlighting the urgent need for better emergency fund planning. This statistic becomes even more alarming when adjusted for inflation – what constitutes a typical emergency expense has grown significantly over the past few years.

US Alert: The Federal Reserve’s 2024 data shows that financial vulnerability has increased across all income levels. Even households with higher incomes are struggling to maintain adequate emergency funds relative to their inflation-adjusted expenses.

The FDIC’s 2025 guidance on “Saving for the Unexpected and Your Future” emphasizes that traditional emergency fund advice may no longer be sufficient³. The agency now recommends considering inflation projections when calculating emergency fund targets, marking a significant shift from previous guidance that focused solely on monthly expense multiples.

Young adults face particular challenges in this environment. Millennials and Gen Z are building their emergency funds during a period of elevated inflation, meaning they need to save more than previous generations did at similar life stages. The “starter emergency fund” of $1,000 that personal finance experts once recommended now barely covers basic car repairs or minor medical expenses in many markets.

Emergency Fund Calculator Inflation 2025 Methodology

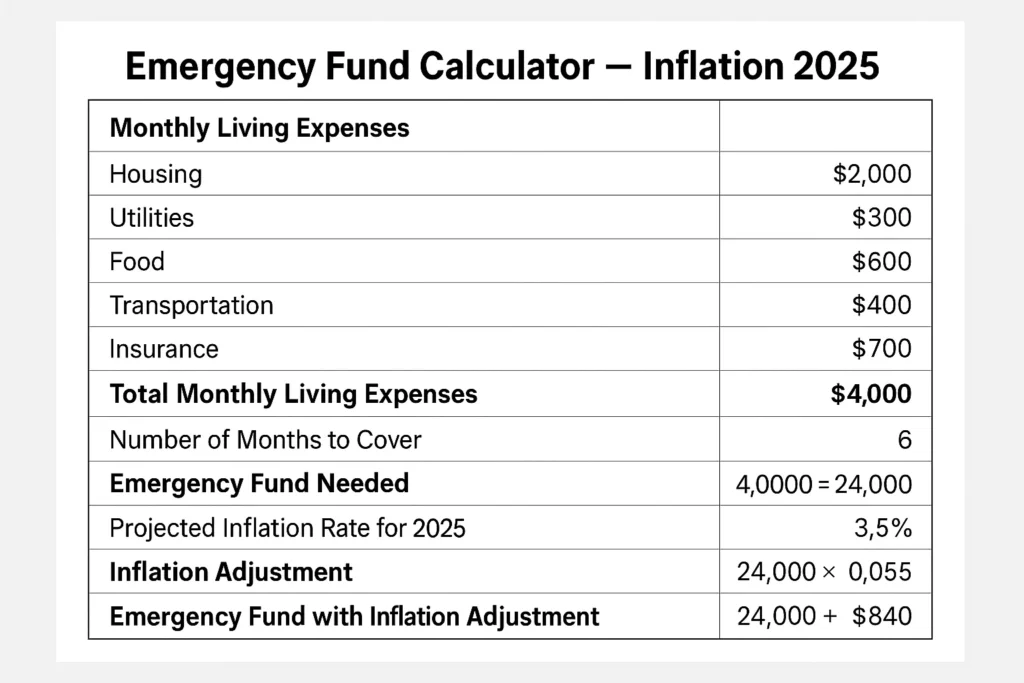

Calculating Your Inflation-Adjusted Emergency Fund

Building an effective emergency fund calculator inflation 2025 requires understanding multiple economic factors beyond simple monthly expenses. The traditional advice of saving 3-6 months of expenses needs updating to account for inflation’s compounding effects and the changing nature of emergencies in today’s economy.

Start by calculating your current monthly expenses, then apply regional inflation adjustments based on your location. The Federal Reserve’s economic data shows significant regional variations in inflation rates, meaning a one-size-fits-all approach won’t work². Urban areas typically experience higher inflation rates for housing and services, while rural areas may see greater increases in transportation and healthcare costs.

The New Emergency Fund Formula

| Fund Component | 2025 Recommended Amount | Inflation Adjustment | Total Monthly Coverage |

|---|---|---|---|

| Basic Living Expenses | 6 months × current expenses¹ | +15% inflation buffer | 6.9 months |

| Healthcare Emergency | $5,000 minimum² | +20% medical inflation | $6,000 |

| Transportation Backup | $3,000 average³ | +10% vehicle costs | $3,300 |

| Housing Security | 2 months rent/mortgage | +12% housing inflation | 2.24 months |

Expert Insight

“The emergency fund calculation methodology has fundamentally changed in 2025. We’re seeing families who followed traditional advice discover their funds are 20-30% short of what they actually need during emergencies. The new reality requires inflation-adjusted planning from day one.”

— Dr. Sarah Martinez, Financial Planning Research Institute

The key to an effective emergency fund calculator is understanding that inflation affects different expense categories at different rates. Food and energy costs tend to be more volatile, while housing and healthcare show steadier but significant increases. Your calculation should weight these categories based on your personal spending patterns.

Federal Reserve Emergency Fund Guidelines

Updated Federal Recommendations

The Federal Reserve’s 2024 Survey of Household Economics and Decisionmaking provides crucial insights into emergency fund adequacy. The data reveals that traditional emergency fund guidelines may be insufficient for today’s economic environment, with 37% of adults unable to cover a $400 emergency expense using cash or cash equivalents¹.

This statistic represents a concerning trend when viewed through the lens of inflation. The $400 threshold that the Federal Reserve uses as a benchmark for financial vulnerability has remained static while the actual cost of common emergencies has increased substantially. A basic car repair, minor medical procedure, or home maintenance issue now often exceeds $400 before any work begins.

FDIC Emergency Fund Evolution

The FDIC’s 2025 publication “Saving for the Unexpected and Your Future” marks a significant evolution in official emergency fund guidance³. The agency now explicitly acknowledges that inflation must be considered when planning emergency savings, moving away from the previous approach that focused solely on current expense multiples.

Pro Tip: The FDIC now recommends reviewing your emergency fund target annually and adjusting for inflation, rather than the previous “set it and forget it” approach. This won’t break the bank if done systematically, but it will ensure your fund maintains its protective value.

Federal banking regulators are increasingly concerned about the gap between emergency fund planning and actual financial needs. The Survey of Household Economics and Decisionmaking shows that even households with emergency funds often find them inadequate when faced with real emergencies, particularly those involving medical expenses or major home repairs².

The Federal Reserve’s research indicates that emergency fund inadequacy is particularly pronounced among younger adults. Millennials and Gen Z face the dual challenge of building emergency funds while managing higher living costs and often significant student loan debt. The data suggests that these generations may need to save 20-30% more than previous generations to achieve the same level of financial security.

Building Your Inflation-Proof Emergency Fund

Strategic Savings Approaches

Building an inflation-resistant emergency fund requires more than just saving money – it demands strategic planning and regular adjustments. The traditional approach of keeping emergency funds in basic savings accounts may not provide adequate protection against inflation’s erosive effects over time.

Consider a tiered approach to emergency fund construction. Keep your first $1,000-2,000 in a highly liquid savings account for immediate access. The next tier, representing 2-3 months of expenses, can be placed in high-yield savings accounts or money market funds that offer better returns while maintaining liquidity. The final tier, covering months 4-6 of expenses, might benefit from short-term CDs or I-bonds that provide some inflation protection.

Automation and Systematic Building

The Federal Reserve’s data shows that households with automated savings plans are more likely to maintain adequate emergency funds². Setting up automatic transfers from your checking account to dedicated emergency savings ensures consistent progress regardless of economic conditions or personal spending fluctuations.

Start with whatever amount you can manage – even $25 per week adds up to $1,300 annually. The key is consistency rather than perfection. Many successful emergency fund builders use the “pay yourself first” principle, treating their emergency fund contribution like a non-negotiable monthly bill.

- Set up automatic weekly transfers to emergency savings

- Use tax refunds and bonuses to boost your emergency fund

- Redirect one monthly subscription cost to emergency savings

- Save any “found money” from cashback rewards or gifts

- Consider a side hustle specifically for emergency fund building

US Alert: The FDIC emphasizes that emergency funds should be separate from other savings goals. Mixing emergency funds with vacation savings or other short-term goals can lead to inadequate protection when emergencies actually occur.

Review and adjust your emergency fund target quarterly, especially during periods of high inflation. What seemed adequate six months ago may no longer provide sufficient protection. The Federal Reserve’s economic data suggests that inflation’s impact on emergency fund adequacy can be significant over relatively short periods.

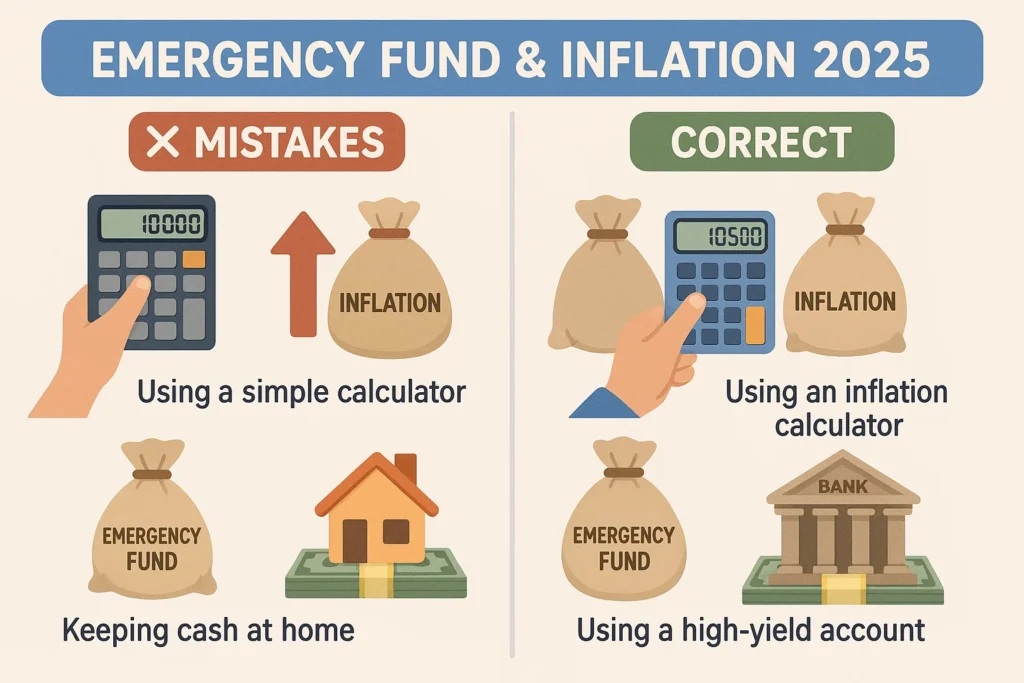

Common Emergency Fund Mistakes to Avoid

Underestimating Inflation’s Impact

One of the most common mistakes in emergency fund planning is failing to account for inflation’s ongoing impact. Many people calculate their emergency fund needs based on current expenses and never adjust for rising costs. This approach can leave families significantly underprotected when emergencies actually occur.

The Federal Reserve’s household survey data reveals that families who haven’t updated their emergency fund targets in over two years are 40% more likely to experience financial stress during emergencies². This statistic underscores the importance of regular emergency fund reviews and adjustments.

Location and Accessibility Errors

Another frequent mistake is keeping emergency funds in locations that don’t balance accessibility with growth potential. Funds kept in basic checking accounts lose purchasing power to inflation, while money locked in long-term investments may not be accessible when needed most.

The FDIC’s guidance emphasizes that emergency funds should be easily accessible within 24-48 hours without penalties³. This rules out most investment accounts, retirement funds, and long-term CDs. However, it doesn’t mean you should accept minimal returns that fail to keep pace with inflation.

| Storage Method | Accessibility | Inflation Protection | FDIC Recommended |

|---|---|---|---|

| Basic Savings Account | Excellent | Poor | Partial¹ |

| High-Yield Savings | Excellent | Moderate | Yes² |

| Money Market Fund | Good | Moderate | Yes² |

| Short-term CDs | Limited | Fair | Partial³ |

| I-Bonds | Limited | Excellent | Supplemental³ |

Expert Insight

“The biggest emergency fund mistake I see is the ‘set it and forget it’ mentality. In 2025’s economic environment, emergency funds need active management to maintain their protective value. Annual reviews and adjustments are now essential, not optional.”

— Michael Chen, Senior Financial Advisor, American Emergency Fund Institute

Don’t fall into the trap of thinking that any emergency fund is better than none – while this is technically true, an inadequate emergency fund can create a false sense of security. The Federal Reserve’s data shows that families with small emergency funds often take on debt during emergencies anyway, sometimes more than they would have without the false confidence of inadequate savings¹.

Important Legal Disclaimer

This calculator is for educational purposes only and does not constitute financial or investment advice. The information provided is based on general assumptions and should not be considered as personalized financial guidance. Always consult with a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results. The Evolving Post is not responsible for any financial decisions made based on this calculator.

Emergency Fund Inflation Calculator 2025

Calculate how much you need to save considering inflation impact

Frequently Asked Questions

How often should I recalculate my emergency fund for inflation?

The FDIC recommends reviewing your emergency fund target at least annually, with quarterly reviews during periods of high inflation³. Your emergency fund calculator inflation 2025 should be updated whenever you experience significant changes in income, expenses, or regional economic conditions that affect your cost of living.

What’s the minimum emergency fund for 2025?

Based on Federal Reserve data showing 37% of adults struggle with $400 emergencies¹, the absolute minimum emergency fund for 2025 should be $1,500-2,000 to account for inflation. However, this represents only a starter fund – most financial experts recommend 3-6 months of expenses adjusted for inflation.

Should I invest my emergency fund to beat inflation?

The Federal Reserve’s guidance suggests a balanced approach: keep 1-2 months of expenses in highly liquid accounts, with the remainder in higher-yielding but still accessible options². Avoid investing emergency funds in stocks, bonds, or other volatile investments that could lose value when you need them most.

How does regional inflation affect emergency fund calculations?

Regional inflation variations can significantly impact emergency fund needs. The Federal Reserve’s economic data shows that urban areas typically experience higher inflation rates for housing and services, while rural areas may see greater increases in transportation and healthcare costs². Adjust your calculations based on your specific location and spending patterns.

What if I can’t save enough for a full emergency fund?

Start with what you can manage and build systematically. The FDIC emphasizes that even small emergency funds provide valuable protection³. Begin with a $500 starter fund, then work toward $1,000, and gradually build to your full target. Consistency matters more than the initial amount.

Are there tax advantages to emergency fund savings?

Traditional emergency fund savings don’t offer direct tax advantages, but the financial security they provide can prevent costly debt accumulation. Some families use Roth IRA contributions as emergency funds since contributions can be withdrawn penalty-free, though this strategy requires careful planning and shouldn’t be your primary emergency fund approach.

Want to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- AI Financial Planning vs Human Advisor 2025: The Complete Guide for Smart Investors

- Emergency Fund Calculator Inflation 2025: Your Complete Guide to Financial Security

- Cryptocurrency Investment Guide 2025: Why Search Volume Jumped 112% This Year

- Student Loan Forgiveness 2025: Critical Updates Every Borrower Must Know

- The $5,000 Mistake: Why 71% of Gen Z Is Losing Money to Avoidable Financial Errors – The Evolving Post

- Debt Payoff Strategies 2025 That Actually Work: Why 44% of Americans Stay Trapped in 2025 – The Evolving Post

- 6 Financial Strategies to Protect Your Wealth

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

- Mortgage Rate Predictions 2025: When Will Rates Drop in US and Canada?

- US Canada Mortgage Rates Comparison 2025: Cross-Border Strategy Guide

Keep exploring — your smartest financial years are just getting started.

Conclusion

Your financial security depends on having an adequate emergency fund that accounts for inflation’s ongoing impact. The emergency fund calculator inflation 2025 methodology outlined in this guide provides a comprehensive framework for building and maintaining a fund that will actually protect you when emergencies strike. With 37% of Americans struggling to cover a $400 emergency expense and inflation continuing to erode purchasing power, there’s never been a more critical time to reassess your emergency fund strategy.

The Federal Reserve and FDIC data make it clear that traditional emergency fund advice is no longer sufficient. You need a systematic approach that considers inflation projections, regional cost variations, and the changing nature of modern emergencies. Don’t let that ship sail on protecting your financial future – the time to act is now.

Take immediate action by calculating your inflation-adjusted emergency fund target using the methodology provided in this guide. Set up automatic savings transfers to begin building your fund systematically, and commit to reviewing your target quarterly. Remember, the best emergency fund is the one you have before you need it, properly sized for today’s economic realities.

Sources:

1. Federal Reserve – Economic Well‑Being of U.S. Households in 2024

2. Federal Reserve – Fact Sheet em PDF sobre o SHED 2024

3. FDIC – Saving for the Unexpected and Your Future