A 401k loan calculator helps Americans understand the true cost of borrowing from their retirement savings. According to the Internal Revenue Service, you can typically borrow up to 50% of your vested account balance or $50,000, whichever is less. Recent data from the Employee Benefit Research Institute shows that 15% of eligible participants have outstanding 401k loans, making loan calculators essential tools for informed decision-making.

📊 Financial Analysis by

Anderson Silva, The Evolving Post

7 years of dedicated financial research and policy analysis. Data sourced from IRS, Department of Labor, and Federal Reserve official documentation.

Table of Contents

- How 401k Loan Calculators Work

- 401k Loan Limits and Federal Rules

- Calculating Monthly Payments and Interest

- True Cost Analysis: What Calculators Don’t Show

- Alternatives to 401k Loans

- When 401k Loans Make Financial Sense

- try-our-401k-loan-calculator

- Frequently Asked Questions

How 401k Loan Calculators Work

What makes a 401k loan calculator different from traditional loan calculators? These specialized tools factor in unique retirement plan regulations and opportunity costs that standard calculators miss. The IRS guidance on 401k loans emphasizes that borrowing from retirement accounts involves complex calculations beyond simple interest rates.

Most 401k loan calculators require these key inputs:

- Current 401k Balance: Your total vested account value

- Desired Loan Amount: Amount you want to borrow (up to federal limits)

- Interest Rate: Typically prime rate plus 1-2%

- Repayment Term: Usually 5 years for general purposes

- Payment Frequency: Monthly, quarterly, or other schedule

According to the Department of Labor, more than half of employer plans allow 401k loans, but each calculator must account for specific plan provisions that may differ from federal maximums.

The calculation methodology involves standard loan formulas adjusted for retirement plan specifics. Most calculators use the present value formula: PV = PMT × [(1 – (1 + r)^-n) / r], where PV is the loan amount, PMT is the payment, r is the interest rate per period, and n is the number of payments.

Understanding Calculator Limitations

Standard 401k loan calculators typically don’t account for opportunity costs, tax implications of loan defaults, or the impact of reduced retirement contributions during repayment periods. These factors can significantly affect the true cost of borrowing from your retirement savings.

Advanced Calculator Features

Sophisticated calculators include features like loan comparison tools, opportunity cost analysis, and scenarios for early repayment or job changes that could trigger immediate repayment requirements. These tools help users understand the full financial impact of their borrowing decision.

401k Loan Limits and Federal Rules

How do federal regulations determine your maximum 401k loan amount? The calculation involves multiple IRS rules that affect how much you can actually borrow from your retirement savings, with specific limits based on your account balance and borrowing history.

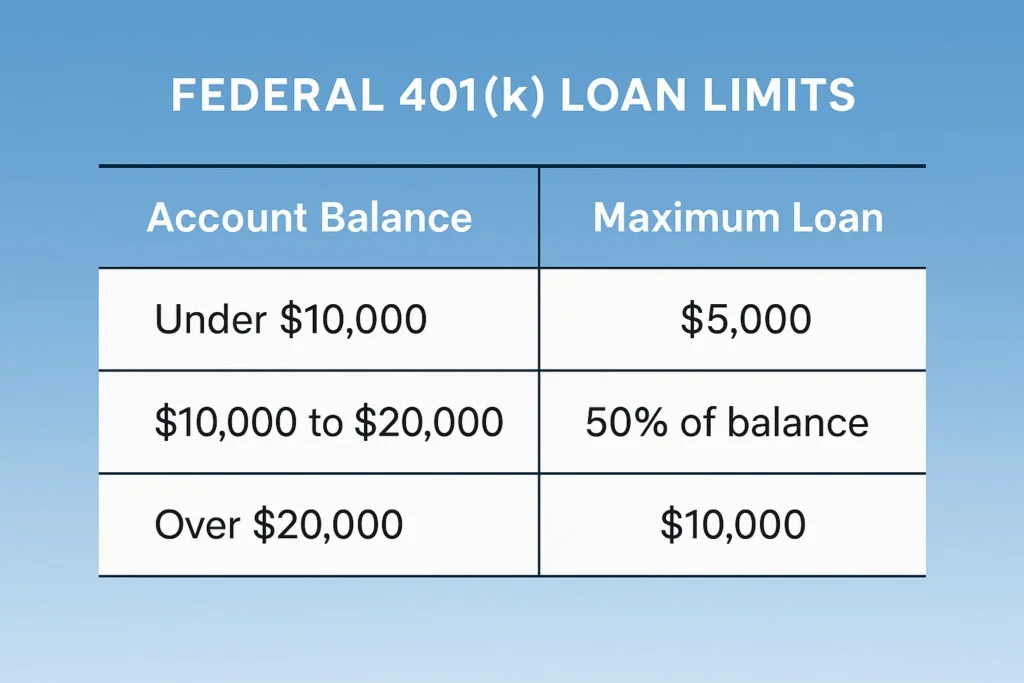

The IRS distribution rules establish that you may borrow up to 50% of your vested account balance up to a maximum of $50,000. However, additional restrictions apply if you’ve had outstanding loans in the past year.

Federal Borrowing Limits:

| Account Balance | Maximum Loan Amount | Minimum Loan (if available) |

|---|---|---|

| Under $10,000 | Up to $10,000 | Plan minimum |

| $10,000 – $20,000 | 50% of balance | $5,000 – $10,000 |

| $20,000 – $100,000 | 50% of balance | $10,000 – $50,000 |

| Over $100,000 | $50,000 maximum | Up to $50,000 |

The IRS borrowing limits documentation explains that if you had an outstanding loan balance in the past 12 months, your new loan limit must be reduced by the highest previous balance minus the current outstanding amount.

Recent statistics from the Plan Sponsor Council of America reveal that 23% of eligible participants have access to loan features, with average loan amounts increasing 4% year-over-year.

Mandatory Repayment Requirements

Federal law requires loan repayment within 5 years for general purposes, with substantially level payments made at least quarterly. Home purchase loans may extend beyond 5 years under specific circumstances defined by the IRS.

Employer Plan Variations

While the IRS sets maximum limits, individual employer plans may impose stricter requirements regarding minimum loan amounts, interest rates, or repayment schedules that affect calculator results. Some plans limit loans to specific purposes or require spouse consent.

Calculating Monthly Payments and Interest

What factors determine your actual monthly 401k loan payments? Beyond the principal amount, several variables affect your repayment calculations, including interest rates, payment frequency, and loan terms that directly impact your monthly budget.

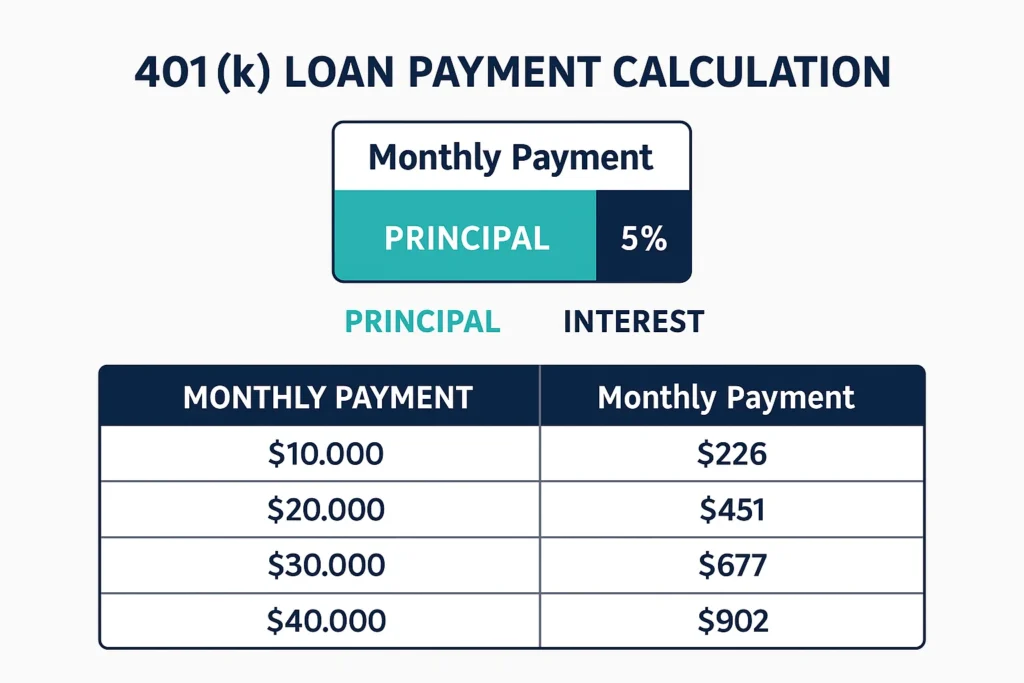

Interest rates on 401k loans typically range from prime rate plus 1-2%, according to IRS commercial reasonableness requirements. Current rates generally fall between 7-9% annually, significantly lower than credit cards but higher than some secured loans.

Sample Payment Calculations (8% annual rate, monthly payments):

- $10,000 loan over 5 years: $202.76 monthly payment, $2,165.84 total interest

- $20,000 loan over 5 years: $405.53 monthly payment, $4,331.68 total interest

- $30,000 loan over 5 years: $608.29 monthly payment, $6,497.52 total interest

- $50,000 loan over 5 years: $1,013.82 monthly payment, $10,829.20 total interest

The payment calculation uses the standard amortization formula where each payment includes both principal and interest, with early payments consisting primarily of interest and later payments focusing on principal reduction.

Interest Payment Benefits

Unlike traditional loans, 401k loan interest payments go back into your own retirement account rather than to a bank or credit card company. This unique feature means you’re essentially paying interest to yourself, though you still lose potential investment growth on the borrowed funds.

Payment Frequency Options

Most plans offer flexible payment schedules including monthly, biweekly, or quarterly payments. Biweekly payments can reduce total interest costs and shorten the repayment period by making 26 payments per year instead of 12 monthly payments.

True Cost Analysis: What Calculators Don’t Show

Why do basic 401k loan calculators often underestimate the real cost of borrowing from your retirement? The hidden costs extend far beyond monthly payments, including opportunity costs, reduced employer matching, and potential tax consequences that significantly impact your financial future.

The most significant hidden cost is opportunity cost – the investment returns you lose by removing money from your retirement account. According to Federal Reserve data, the average 401k account earned approximately 8.3% annually over the past decade, meaning a $30,000 loan could cost you $12,000 in lost growth over five years.

Hidden Costs Analysis:

- Opportunity Cost: Lost investment growth on borrowed funds

- Reduced Contributions: Many borrowers reduce or stop contributions during repayment

- Lost Employer Match: Missing out on free employer matching funds

- Tax Consequences: Potential taxes and penalties if loan defaults

- Administrative Fees: Setup and maintenance fees charged by plan administrators

Research from the Center for Retirement Research at Boston College indicates that 401k loan default rates remain relatively low at 10-15%, but defaults can trigger immediate tax liabilities and 10% early withdrawal penalties.

Compound Interest Impact

The long-term impact of removing funds from a tax-advantaged account compounds over time. A $20,000 loan taken at age 35 could reduce retirement savings by over $160,000 by age 65, assuming an 8% annual return on the borrowed funds.

Job Change Risks

If you leave your employer, most plans require full loan repayment within 60-90 days. Failure to repay triggers a taxable distribution plus 10% penalty if you’re under age 59½, potentially creating significant tax consequences that calculators don’t account for.

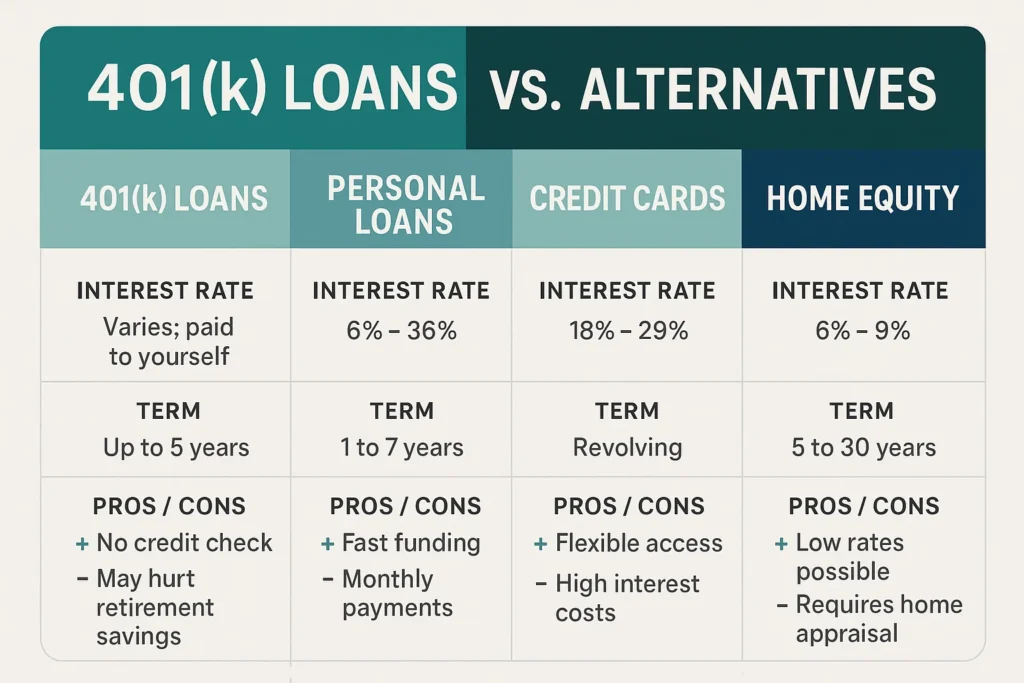

Alternatives to 401k Loans

What other financing options should you consider before borrowing from your 401k? Several alternatives may offer better terms or preserve your retirement savings while still providing access to needed funds.

The Consumer Financial Protection Bureau recommends exploring all borrowing alternatives before tapping retirement funds, as preserving long-term savings typically provides greater financial benefits.

Primary Alternatives to Consider:

- Personal Loans: Unsecured loans with fixed rates, typically 6-15% APR

- Home Equity Loans/HELOC: Lower rates but your home serves as collateral

- Credit Cards: Higher rates but more flexible for short-term needs

- Family Loans: Potentially lower or no interest from relatives

- Emergency Fund: Using existing savings avoids all borrowing costs

- Roth IRA Withdrawals: Contributions can be withdrawn tax-free anytime

According to Senate Banking Committee data, personal loan rates have become increasingly competitive, with many borrowers qualifying for rates lower than typical 401k loan rates.

Emergency Fund Building

Building an emergency fund prevents the need for 401k loans in most situations. Financial experts recommend saving 3-6 months of expenses, which can handle most unexpected costs without touching retirement savings.

Credit Optimization Strategies

Improving your credit score can unlock better borrowing terms through traditional channels, making alternatives to 401k loans more attractive and cost-effective for most borrowing needs.

When 401k Loans Make Financial Sense

Under what specific circumstances might a 401k loan calculator show that borrowing from your retirement makes financial sense? While generally discouraged, certain situations may justify this borrowing strategy when used carefully and strategically.

Financial advisors generally agree that 401k loans work best for short-term needs when you have stable employment and can repay quickly. The Government Accountability Office research shows that participants with stable employment and higher account balances have better loan outcomes.

Scenarios Where 401k Loans May Be Appropriate:

- Home Down Payment: When avoiding PMI saves more than opportunity costs

- High-Interest Debt Consolidation: Paying off credit cards with 20%+ rates

- Emergency Medical Expenses: When no other funding sources exist

- Education Costs: For immediate family education needs

- Major Home Repairs: Essential repairs that protect property value

- Business Investment: High-return opportunities with guaranteed income

Recent analysis from the Urban Institute suggests that 401k loans can be appropriate when borrowers maintain their contribution rates and have clear repayment strategies.

Best Practices for 401k Borrowing

If you decide to proceed with a 401k loan, maintain your regular contributions, borrow only what you need, and have a backup repayment plan in case of job loss or other financial emergencies.

Strategic Timing Considerations

Market timing can affect 401k loan decisions. Borrowing during market downturns may reduce opportunity costs, while borrowing during strong market periods increases the cost of missing potential gains.

Frequently Asked Questions

How does a 401k loan calculator determine my maximum borrowing amount?

A 401k loan calculator uses IRS rules to determine you can borrow up to 50% of your vested account balance or $50,000, whichever is less. The calculator also factors in any outstanding loan balances from the past 12 months.

What interest rate should I expect on a 401k loan?

401k loan interest rates typically equal prime rate plus 1-2%, currently ranging from 7-9% annually according to IRS commercial reasonableness requirements. Your plan administrator sets the specific rate within these guidelines.

What happens if I can’t repay my 401k loan?

If you default on a 401k loan, the outstanding balance becomes a taxable distribution. According to the IRS, you’ll owe income taxes plus a 10% early withdrawal penalty if you’re under age 59½.

Can I use a 401k loan calculator for any employer plan?

Generic calculators use federal limits, but your specific plan may have different rules. The Department of Labor notes that only about half of plans offer loan features, and terms vary by employer.

Should I use a 401k loan to pay off credit card debt?

This depends on your specific situation. While 401k loan rates are typically lower than credit card rates, you lose potential investment growth. The Consumer Financial Protection Bureau recommends exploring all alternatives before borrowing from retirement savings.

Understanding how to use a 401k loan calculator effectively helps you make informed decisions about borrowing from your retirement savings. While these tools provide valuable payment estimates and help you understand federal borrowing limits, remember that the true cost extends beyond monthly payments to include opportunity costs and potential risks. Before using any 401k loan calculator results to make borrowing decisions, consider alternatives and consult with a financial advisor to ensure this strategy aligns with your long-term financial goals and retirement planning objectives.

Try Our 401k Loan Calculator

Want to see exactly what a 401k loan will cost?

Use our 401k loan calculator to instantly estimate your monthly payment, total interest, and the true impact on your retirement savings. Simply click the button below to access the calculator, enter your numbers, and make smarter, data-driven decisions before borrowing from your 401k. Empower your financial future

Ant to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- How Many Jobs Are Available in Finance ? 963K + $101K Salary

- Can You Trade In a Financed Car? 2025 Guide & Requirements

- Cryptocurrency Investment Guide 2025: Why Search Volume Jumped 112% This Year

- Healthcare Cost Financial Planning 2025: Complete Guide for American Retirees

- Emergency Fund Calculator Inflation 2025: Your Complete Guide to Financial Security

- Student Loan Forgiveness 2025: Critical Updates Every Borrower Must Know

- The $5,000 Mistake: Why 71% of Gen Z Is Losing Money to Avoidable Financial Errors

- Debt Payoff Strategies 2025 That Actually Work

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

- Mortgage Rate Predictions 2025: When Will Rates Drop in US and Canada?

Keep exploring — your smartest financial years are just getting started.

Government & Educational Resources

- IRS – Retirement Topics: Loans

- Department of Labor – 401k Plans for Participants

- IRS – Considering a Loan from Your 401k Plan

- Consumer Financial Protection Bureau – Getting Credit

- Federal Reserve – Survey of Consumer Finances

- Government Accountability Office – 401k Plan Fees

- Center for Retirement Research – 401k Loan Default Rates

- Employee Benefit Research Institute – 401k Activity Report