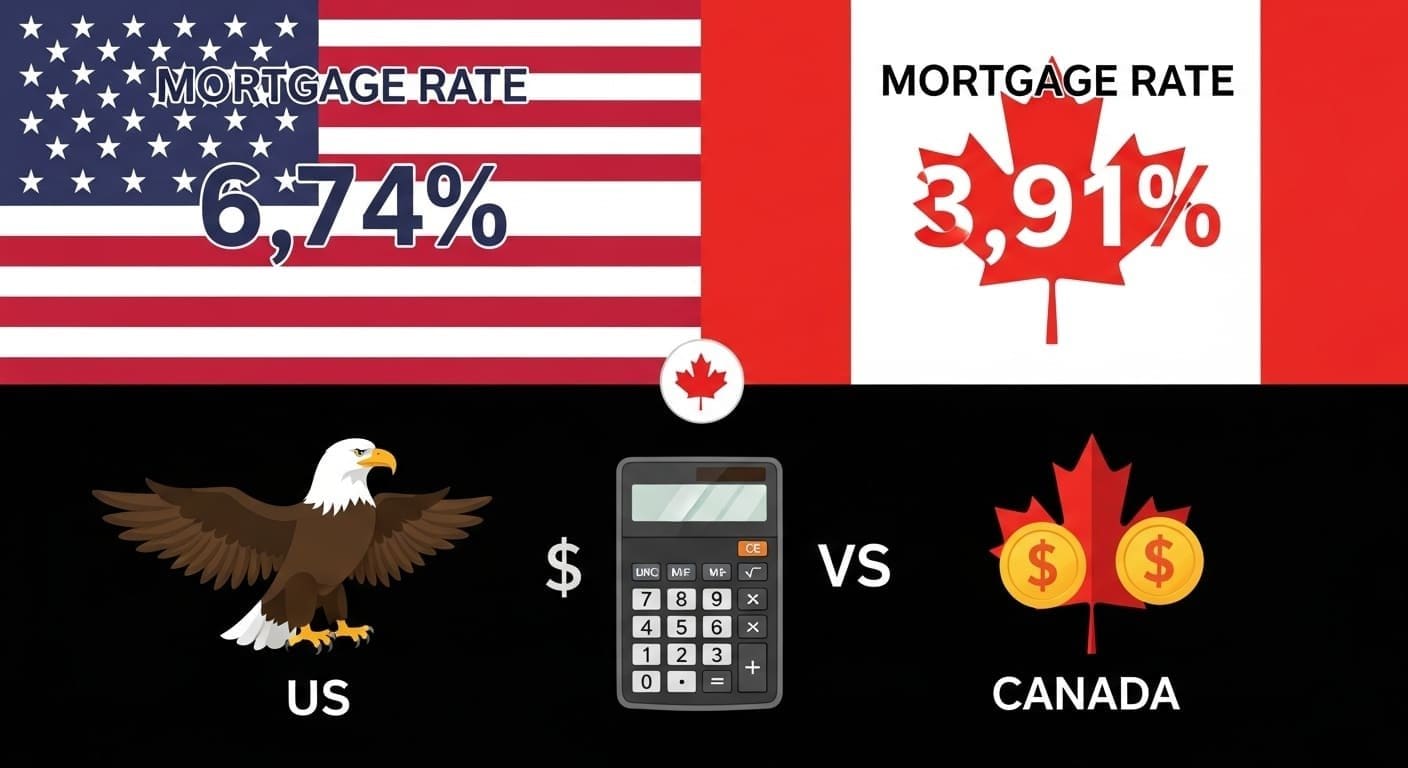

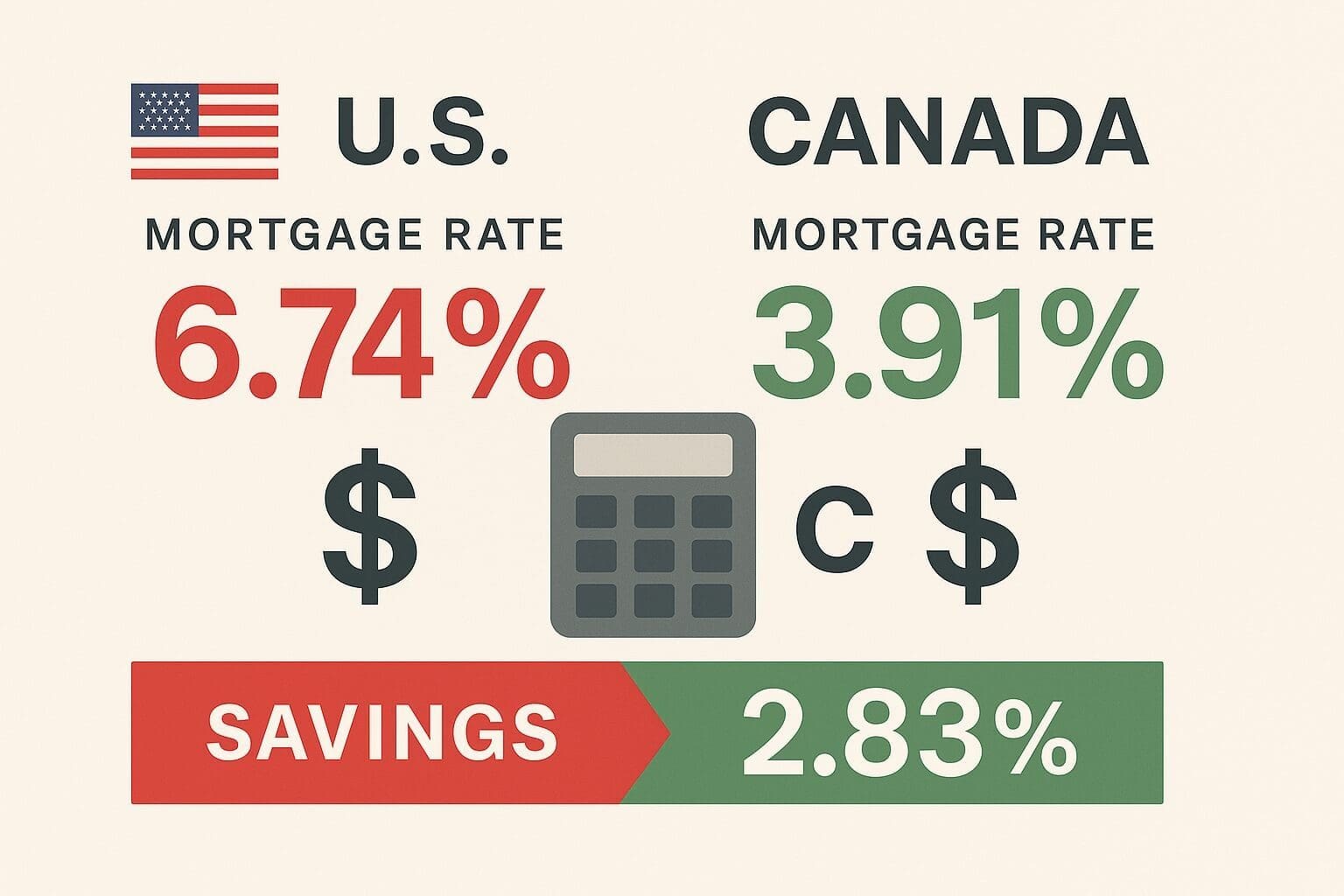

Don’t let a 2.8% mortgage rate differential cost you a fortune. While US borrowers face rates hovering around 6.74% in July 2025, Canadian markets offer competitive 5-year fixed rates starting at 3.91%. That’s not just a number on paper—it’s the difference between paying $150,000 to $200,000 more in interest over your mortgage term. Americans living abroad or considering cross-border property investments are missing out on one of the most significant arbitrage opportunities in decades. The Federal Reserve’s aggressive stance, with the federal funds rate holding at 4.33%[1], contrasts sharply with Canada’s Bank of Canada rate at 2.75%[2]. This guide reveals how savvy cross-border borrowers can navigate both markets to secure the best possible financing for their North American property investments.

Table of Contents

Current Rate Landscape Analysis

US Mortgage Market Reality Check

The American mortgage landscape in July 2025 presents a challenging environment for borrowers. 30-year fixed mortgage rates have climbed to 6.74% for purchases and 6.77% for refinancing[1], representing a significant increase from previous months. This upward pressure stems from the Federal Reserve’s monetary policy stance, with the bank prime loan rate maintaining at 7.50%[1] throughout July 2025.

Recent data from Freddie Mac shows that mortgage rates ticked up to 6.72% following a stronger-than-expected jobs report[1], breaking a five-week decline streak. The economic uncertainty persists as tariff timelines continue to shift, making the interest rate path rather unclear. For American borrowers, this translates to monthly payments that can strain household budgets significantly.

US Alert: The Federal Reserve’s June 2025 projections indicate PCE inflation expected to reach 3.0% by year-end[3], up from March’s 2.6% forecast. This suggests rates may remain elevated longer than previously anticipated.

Canadian Market Opportunities

Canada’s mortgage environment tells a dramatically different story. The Bank of Canada has maintained its overnight rate at 2.75% since June 4, 2025[2], creating a favorable borrowing environment. Current 5-year fixed rates for insured borrowers start at 3.91%, while uninsured borrowers can secure rates at similar levels.

The Canadian prime rate sits at 4.95%, substantially lower than US equivalents. This rate differential creates compelling opportunities for cross-border borrowers who can access Canadian financing. Variable mortgage rates for insured borrowers are available at 3.95%, offering flexibility for those comfortable with rate fluctuations.

Economic Fundamentals Driving the Spread

Several macroeconomic factors contribute to this substantial rate differential. Canada’s inflation rate has declined to 1.7%, well below the Bank of Canada’s target range, providing room for accommodative monetary policy. Meanwhile, US inflation concerns persist, with the Federal Reserve projecting core PCE inflation at 3.1% for 2025[3].

Canadian unemployment stands at 7.0%, while the US labor market remains relatively tight. This divergence in economic conditions justifies the different monetary policy approaches between the two countries.

US Canada Mortgage Rates Comparison Data

Current Rate Breakdown by Product Type

The rate differential varies significantly across different mortgage products, creating strategic opportunities for informed borrowers:

| Mortgage Product | US Rates (July 2025) | Canadian Rates (July 2025) | Spread |

|---|---|---|---|

| 30-Year Fixed | 6.74%[1] | N/A | N/A |

| 5-Year Fixed | N/A | 3.91% | N/A |

| 15-Year Fixed | 5.94%[1] | N/A | N/A |

| 3-Year Fixed | N/A | 3.87% | N/A |

| Variable Rate | 7.87%[1] | 3.95% | 3.92% |

| Jumbo Loans | 6.84%[1] | N/A | N/A |

HUD Housing Market Indicators Impact

The HUD Housing Market Indicators for March 2025 reveal critical market dynamics[2]. New single-family home sales increased 1.8% to 676,000 units[2], while existing home sales rose 4.2% to 4.26 million units[2]. These figures indicate continued demand despite elevated rates.

Median home prices reached $414,500[2] according to HUD data, representing the ongoing affordability challenge for American buyers. The homeownership affordability index stands at 100.7[2], indicating that median-income families have just enough income to qualify for median-priced homes.

Federal Reserve Projections Analysis

The Fed’s June 2025 projections paint a complex picture for mortgage rates[3]. With the federal funds rate projected at 3.9% for 2025[3], mortgage rates are likely to remain elevated. The Fed’s unemployment rate forecast of 4.5% for 2025[3] suggests a cooling labor market, which could eventually provide downward pressure on rates.

GDP growth projections of 1.4% for 2025[3] indicate economic moderation, down from previous forecasts of 1.7%. This slower growth trajectory may influence the Federal Reserve’s future rate decisions.

Canadian Corner: Bank of Canada Governor Tiff Macklem’s recent statements suggest the central bank remains data-dependent, with potential for further rate cuts if economic conditions warrant. This contrasts with the Fed’s more hawkish stance.

Cross-Border Qualification Strategies

Dual Citizenship Advantages

Americans with Canadian citizenship or permanent residency enjoy significant advantages in accessing Canadian mortgage markets. Dual citizens can qualify for insured mortgage rates, which offer the most competitive pricing. This status eliminates many of the barriers that foreign nationals face when seeking Canadian financing.

The qualification process for dual citizens mirrors that of Canadian residents, requiring standard documentation including employment verification, credit history, and down payment confirmation. Stress testing requirements apply at rates approximately 2% higher than contract rates, but this remains manageable given the lower base rates.

Foreign National Pathways

Non-resident Americans can still access Canadian mortgages, though with additional requirements. Uninsured mortgage rates for foreign nationals typically start around 3.91%, still significantly below US equivalents. Lenders may require larger down payments, typically 35% or more, and proof of global income.

Documentation requirements include international credit reports, employment letters, and sometimes Canadian co-signers. The process takes longer than domestic applications but remains viable for motivated borrowers.

Income and Credit Considerations

Canadian lenders evaluate global income differently than US counterparts. Americans working for US companies can often use their US income to qualify for Canadian mortgages, provided they can demonstrate stability and continuity. Currency conversion calculations use conservative exchange rates, typically favoring the lender.

Credit history evaluation varies by lender. Some Canadian institutions accept US credit reports, while others require establishment of Canadian credit history. The minimum credit score requirements are generally similar to US standards, around 620 for insured mortgages and higher for uninsured products.

Legal and Tax Implications

Cross-border mortgage arrangements create complex tax implications. US citizens remain subject to US tax obligations regardless of property location. Canadian property ownership may trigger Canadian tax obligations, particularly for rental income or capital gains upon sale.

Professional tax advice becomes essential for cross-border property owners. Proper structuring can minimize double taxation while maximizing available deductions. Some borrowers establish Canadian corporations to hold properties, though this adds complexity and ongoing compliance requirements.

Market Timing and Economic Factors

Federal Reserve vs Bank of Canada Divergence

The monetary policy divergence between the Federal Reserve and Bank of Canada creates the current opportunity. The Fed’s June 2025 projections suggest only two rate cuts totaling 50 basis points for 2025[3], while Canadian markets price in more aggressive easing.

Market consensus expects the Bank of Canada to hold rates at 2.75% through July 2025[2], with potential cuts later in the year. This divergence is expected to persist through 2025, maintaining the rate differential that benefits cross-border borrowers.

Tariff and Trade Policy Impact

US tariffs of 25% on Canadian imports, though delayed, continue creating market volatility. This uncertainty has pushed Canadian five-year government bonds to 2.57% by April 2025, supporting lower mortgage rates. The trade relationship uncertainty paradoxically benefits Canadian borrowers through lower bond yields.

Economic disruption often creates the best opportunities for contrarian investors. The current environment rewards those willing to navigate cross-border complexity for substantial savings.

Seasonal Rate Patterns

Historical analysis reveals Canadian mortgage rates typically offer better pricing in Q1 and Q4. This seasonal pattern reflects funding costs and competitive dynamics within the Canadian banking system. Strategic borrowers can time their applications to coincide with these favorable periods.

US mortgage rates show less pronounced seasonal variation, though spring homebuying season can create upward pressure. The current July 2025 environment represents a reasonable entry point for those unable to wait for optimal timing.

Currency Considerations

USD/CAD exchange rates fluctuating between 1.25-1.40 throughout 2025 create additional strategic considerations. A stronger US dollar increases purchasing power for American buyers in Canadian markets, while a weaker dollar reduces this advantage.

Currency hedging strategies can protect against adverse movements, though they add cost and complexity. Some borrowers accept currency risk as part of their overall cross-border strategy, particularly for properties generating Canadian dollar income.

Real-World Case Studies

Case Study 1: The Seattle Tech Executive

Sarah, a software engineer from Seattle, leveraged her dual US-Canadian citizenship to purchase a $750,000 Vancouver condo. By securing a 3.91% five-year fixed rate instead of a comparable 6.74% US rate[1], she saves approximately $1,680 monthly in interest costs.

Over a 25-year amortization, Sarah’s total interest savings exceed $420,000. The cross-border complexity required professional tax advice costing $5,000 annually, but the net benefit remains substantial. Her Canadian property also provides portfolio diversification and potential immigration flexibility.

Case Study 2: The Snowbird Investor

Robert and Linda, Florida retirees, purchased a $500,000 Alberta vacation home using Canadian financing. Despite being non-residents, they secured an uninsured rate of 4.05% with a 35% down payment. Their US alternative would have been approximately 6.84% for a jumbo loan[1].

The monthly payment difference of $950 funds their extended Canadian stays. Over 20 years, they’ll save approximately $228,000 in interest costs. The couple established a Canadian corporation to hold the property, optimizing tax treatment for both countries.

Case Study 3: The Cross-Border Business Owner

Michael operates businesses in both Detroit and Windsor, qualifying him for Canadian resident rates despite US primary residence. His $1.2 million commercial property purchase used a 3.95% variable rate, compared to US commercial rates exceeding 7%.

The rate differential saves Michael $3,600 monthly, reinvested into business expansion. His cross-border business operations provide natural currency hedging, as Canadian property costs are offset by Canadian business income.

Implementation Roadmap

Phase 1: Eligibility Assessment (Weeks 1-2)

Determine your cross-border qualification status through citizenship, residency, or business connections. Dual citizens have the clearest path to Canadian resident rates, while others must evaluate foreign national requirements.

Obtain credit reports from both countries to understand your borrowing profile. Canadian credit history, even limited, significantly improves qualification odds. Consider establishing Canadian banking relationships before formal mortgage applications.

Calculate total cost of ownership including currency conversion, legal fees, and ongoing tax compliance. Professional advice costs typically range from $5,000-$15,000 annually but provide essential guidance for complex cross-border structures.

Phase 2: Market Research and Lender Selection (Weeks 3-4)

Research Canadian lenders with cross-border expertise. Major banks like RBC, TD, and BMO offer specialized programs, while credit unions may provide competitive rates for specific regions. Mortgage brokers with cross-border experience can streamline the process.

Monitor rate movements in both markets using tools like rate comparison websites and economic calendars. Bank of Canada announcements occur eight times yearly, providing predictable timing for rate changes.

Prepare documentation packages for multiple lenders to ensure competitive pricing. Pre-approval letters from Canadian lenders strengthen negotiating positions and demonstrate serious intent to sellers.

Phase 3: Application and Execution (Weeks 5-8)

Submit applications to multiple Canadian lenders to ensure competitive rates and terms. Processing times for cross-border applications typically extend 45-60 days, longer than domestic mortgages.

Coordinate legal representation in both countries to handle closing procedures. Canadian real estate lawyers typically charge $1,500-$3,000 for residential transactions, while US tax attorneys may charge similar amounts for structure setup.

Establish Canadian banking relationships before closing to facilitate ongoing payments and property management. Many lenders require Canadian bank accounts for mortgage payments, making this step essential.

Phase 4: Ongoing Management (Ongoing)

Monitor rate environments for refinancing opportunities. Canadian mortgages typically renew every 5 years, providing regular opportunities to reassess rates and terms.

Maintain compliance with both countries’ tax obligations through professional assistance. Annual compliance costs are offset by substantial interest savings for most cross-border borrowers.

Consider exit strategies including sale procedures and tax implications. Proper planning minimizes tax consequences while maximizing investment returns.

Key Takeaways

- Rate differential of 2.8% between US and Canadian markets creates unprecedented savings opportunities for qualified cross-border borrowers

- Dual citizens enjoy the clearest path to Canadian resident rates starting at 3.91% compared to US rates of 6.74%[1]

- Federal Reserve projections suggest US rates will remain elevated through 2025[3] while Canadian rates may decline further

- Cross-border mortgage strategies require professional guidance but can save $150,000-$200,000 over typical mortgage terms

- Currency fluctuations and trade policy create additional complexity but don’t eliminate the fundamental rate advantage

- Proper documentation and lender selection are critical for successful cross-border mortgage execution

“What’s your biggest cross-border mortgage challenge? Share your experience and questions below! 👇”

Want to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- 6 Financial Strategies to Protect Your Wealth

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- 8 Powerful Financial Strategies Every Single Person Should Know

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

- Mortgage Rate Predictions 2025: When Will Rates Drop in US and Canada?

Keep exploring — your smartest financial years are just getting started.

References: