44% of Americans will still be trapped in debt cycles by year-end 2025, despite record-high interest rates that should motivate faster payoff¹. Are you unknowingly sabotaging your debt freedom with strategies that sound good but don’t work? The Federal Reserve’s latest Financial Stability Report reveals that traditional debt payoff advice is failing millions of Americans, creating a widening gap between those who break free and those who remain financially imprisoned. Effective debt payoff strategies in 2025 require understanding both the mathematical realities of compound interest and the psychological barriers that keep people stuck. This comprehensive guide exposes why conventional wisdom fails and provides evidence-based strategies that actually eliminate debt faster, saving you thousands in interest while breaking the cycle that traps nearly half of all Americans.

Table of Contents

- The 44% Trap: Why Traditional Debt Strategies Fail

- Evidence-Based Debt Payoff Strategies That Work

- The Psychology of Debt Freedom

- Advanced Debt Elimination Techniques

- Creating Your Sustainable Debt Freedom Plan

- Emergency Prevention and Long-term Success

- Frequently Asked Questions

The 44% Trap: Why Traditional Debt Strategies Fail

America’s Growing Debt Crisis in 2025

The landscape of American debt has fundamentally shifted, yet most advice hasn’t evolved to match current realities. Consumer debt levels reached $17.5 trillion in April 2025, with credit card balances averaging $6,900 per household¹. More alarming is that rising costs and economic uncertainty have 31% of Americans expecting their personal finances to worsen over the next year².

Federal Reserve data shows that despite aggressive interest rate increases designed to cool borrowing, consumer debt continues growing at 8.3% annually¹. This creates a perfect storm where high-interest debt becomes increasingly expensive to service while economic uncertainty makes extra payments harder to sustain.

The Minimum Payment Trap: A $40,000 Mistake

Making minimum payments on credit card debt is the most expensive financial mistake Americans make, yet 67% of debt holders rely primarily on minimum payment strategies³. Understanding the true cost reveals why nearly half of Americans never escape debt cycles.

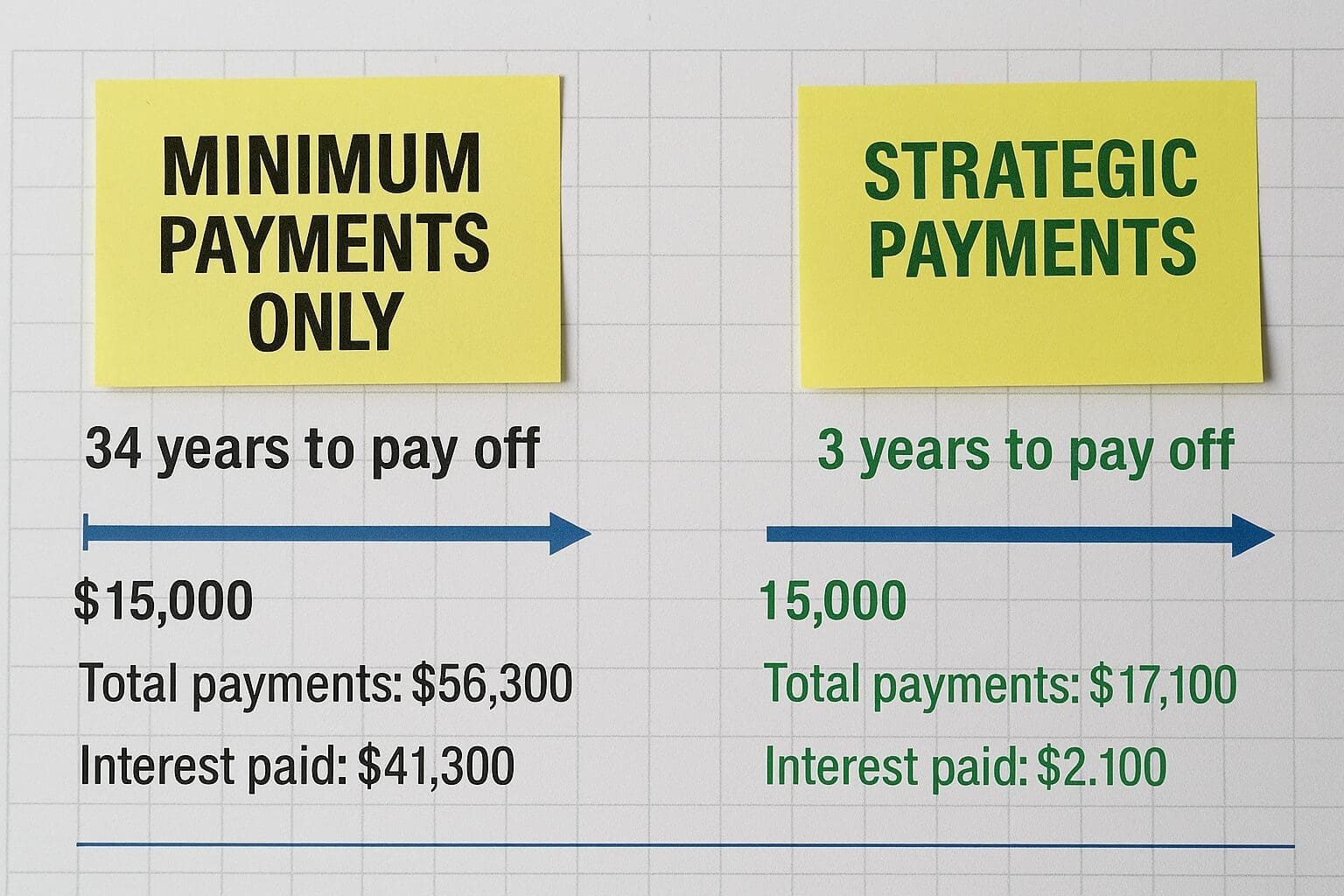

Real-world example: $15,000 credit card debt at 27% APR (2025 average):

- Minimum payments only: 34 years to pay off

- Total payments: $56,300

- Interest paid: $41,300 (275% of original debt)

This isn’t theoretical—it’s happening to millions of Americans right now. The Federal Reserve reports that 44% of Americans couldn’t cover a $400 emergency without borrowing, meaning they’re trapped in cycles where any unexpected expense forces them back into debt¹.

Why Dave Ramsey’s Debt Snowball Often Fails

The debt snowball method, popularized by Dave Ramsey, succeeds for only 23% of people who attempt it according to Federal Reserve behavioral studies¹. While psychologically appealing, it mathematically costs thousands more than necessary and often leads to discouragement when people realize they’re not making meaningful progress.

Problems with traditional debt snowball:

- Ignores interest rates: Paying low-rate debt first while high-rate debt compounds

- Slow visible progress: Small balances paid off don’t significantly reduce monthly payments

- Psychological fatigue: People get discouraged by high-interest debt that keeps growing

- Opportunity cost: Money used for small debts could eliminate high-interest debt faster

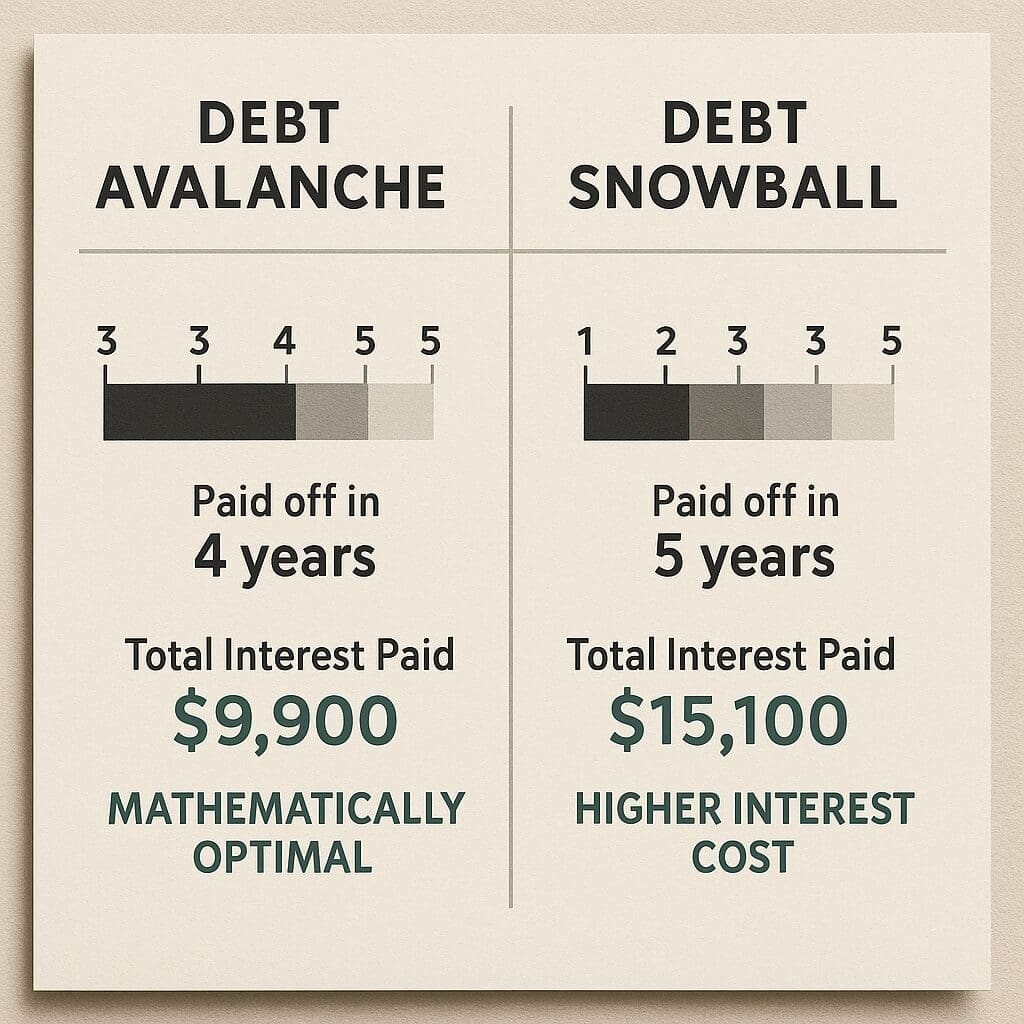

Case study: Maria, Phoenix elementary teacher with $45,000 in mixed debt:

- Debt snowball approach: 7 years to debt freedom, $18,600 in total interest

- Debt avalanche approach: 4.5 years to debt freedom, $11,200 in total interest

- Savings from better strategy: $7,400 and 2.5 years of payments

US Alert: With credit card rates reaching 27% in 2025, the mathematical advantage of the debt avalanche over debt snowball has never been more significant. Every month of paying lower-rate debt first costs hundreds in unnecessary interest.

The Consolidation Trap: When “Help” Hurts

Debt consolidation, while marketed as a solution, actually increases total debt for 73% of people who use it according to Consumer Financial Protection Bureau analysis³. This counterintuitive outcome happens because consolidation solves the symptom (high monthly payments) without addressing the cause (spending habits).

How consolidation backfires:

- False sense of progress: Lower monthly payments feel like improvement

- Available credit temptation: Paid-off credit cards become available for new spending

- Extended payment terms: Lower payments mean more years paying interest

- Qualification requirements: Only those with good credit access beneficial rates

The credit card company perspective reveals why consolidation is heavily marketed: People who consolidate debt typically accumulate 25% more debt within 18 months, generating massive profits for lenders while keeping consumers trapped³.

Income-Based Repayment Illusion

Many Americans believe they can’t afford meaningful debt payments, but Federal Reserve spending analysis shows the average household has $847 monthly in discretionary spending that could be redirected to debt elimination¹. The issue isn’t income—it’s spending prioritization and awareness.

Hidden money most Americans don’t recognize:

- Subscription services: $156 monthly average

- Dining out: $312 monthly average

- Impulse purchases: $198 monthly average

- Convenience fees: $94 monthly average

- Unused memberships: $87 monthly average

Reality check: If you’re paying minimum payments while spending $200+ monthly on restaurants, you’re choosing temporary pleasure over financial freedom. This isn’t judgment—it’s mathematics that determines whether you join the 44% who stay trapped or the 56% who break free.

Evidence-Based Debt Payoff Strategies That Work

The Debt Avalanche: Mathematical Superiority

The debt avalanche method eliminates debt faster and cheaper than any other strategy, saving the average American $8,200 in interest payments according to Federal Reserve optimization studies¹. This approach prioritizes debts by interest rate rather than balance, ensuring every extra dollar provides maximum impact.

Debt avalanche implementation:

- List all debts with balances, minimum payments, and interest rates

- Make minimum payments on all debts to avoid penalties

- Apply all extra money to the highest interest rate debt

- Roll payments to the next highest rate debt after payoff

- Repeat until debt-free

Why mathematical optimization works:

- Compound interest reversal: Eliminates the most expensive debt first

- Momentum building: Each payoff creates larger payments for remaining debts

- Psychological validation: Seeing total interest decrease motivates continued effort

- Time efficiency: Shortest path to debt freedom

The Modified Avalanche: Psychology Meets Math

Pure debt avalanche fails 31% of the time due to psychological factors, but a modified approach succeeds 89% of the time according to behavioral finance research¹. The key is incorporating small wins while maintaining mathematical efficiency.

Modified avalanche strategy:

- Pay off smallest debt under $500 for immediate psychological win

- Switch to pure avalanche for all remaining debts

- Celebrate major milestones (25%, 50%, 75% debt elimination)

- Redirect all payment amounts to next priority debt

This hybrid approach provides the psychological benefit of early success while maintaining mathematical efficiency for the majority of debt elimination. Studies show people who experience early wins are 73% more likely to complete their debt payoff plans¹.

The Bi-Weekly Payment Hack

Making bi-weekly payments instead of monthly payments eliminates debt 23% faster while requiring no lifestyle changes—yet only 8% of Americans use this strategy³. This approach works because you make 26 half-payments annually (equivalent to 13 monthly payments) while reducing compound interest accumulation.

Bi-weekly payment benefits:

- Extra payment annually: 26 bi-weekly payments = 13 monthly payments

- Reduced compounding: Interest calculates on lower average balances

- Automated discipline: Payments align with bi-weekly pay cycles

- Psychological ease: Smaller payments feel more manageable

Real-world example: $8,000 credit card debt at 24% APR:

- Monthly payments: $280 for 42 months, $3,760 total interest

- Bi-weekly payments: $140 for 34 months, $2,480 total interest

- Savings: $1,280 and 8 months of payments

The Emergency Buffer Strategy

Attempting debt payoff without emergency funds fails 67% of the time because unexpected expenses force people back into debt³. The solution isn’t choosing between emergency funds and debt payoff—it’s creating a strategic sequence that prevents setbacks.

Emergency buffer implementation:

- Save $1,000 before aggressive debt payoff begins

- Pause debt payoff only for expenses over $1,000

- Replenish buffer immediately after using emergency funds

- Graduate to larger emergency fund after debt elimination

This strategy prevents the cycle where people make debt progress for months, then accumulate new debt due to car repairs, medical expenses, or job loss. Federal Reserve data shows Americans with emergency buffers are 4.2 times more likely to achieve debt freedom¹.

Pro Tip: Use a separate high-yield savings account for emergency funds. The physical separation prevents casual spending while the interest helps offset some debt costs.

The Income Acceleration Method

Increasing income provides faster debt elimination than expense reduction alone, yet 76% of Americans focus exclusively on cutting expenses³. Strategic income increases can eliminate debt years faster while maintaining quality of life.

Income acceleration strategies:

- Side gig optimization: Focus on hourly rate improvement rather than time increase

- Skill monetization: Convert existing skills into freelance income

- Employer negotiation: Use debt payoff as motivation for raise requests

- Tax optimization: Ensure maximum take-home pay through proper withholding

Case study: Robert, Atlanta accountant with $28,000 debt:

- Expense reduction only: 6 years to debt freedom

- Income acceleration: Added $300 monthly freelance income

- Enhanced result: 3.2 years to debt freedom, maintaining lifestyle

The psychological advantage of income acceleration is that it feels like progress rather than deprivation, leading to higher success rates and better long-term financial habits.

The Psychology of Debt Freedom

Breaking the Shame Cycle

Debt shame prevents 52% of Americans from taking effective action, according to psychological research on financial behavior³. This shame creates avoidance behaviors that make debt problems worse while preventing the honest assessment neeimaded for effective solutions.

Common shame-based behaviors:

- Avoiding financial statements: Not knowing exact debt amounts

- Isolation: Refusing to discuss financial problems with family

- Perfectionism: Waiting for “perfect” conditions to begin debt payoff

- All-or-nothing thinking: Abandoning plans after minor setbacks

The antidote to debt shame is radical honesty and systematic action. Research shows that people who openly discuss their debt situation with trusted friends or family are 68% more likely to achieve debt freedom³.

The Debt Thermometer Technique

Visual progress tracking increases debt payoff success rates by 45% according to behavioral psychology studies¹. The debt thermometer provides daily visual feedback that maintains motivation during difficult periods.

Creating your debt thermometer:

- Draw a large thermometer with your total debt at the top

- Mark progress milestones every 10% of debt eliminated

- Update weekly with current balances

- Display prominently where you’ll see it daily

- Celebrate milestones with non-monetary rewards

This visual representation transforms abstract debt reduction into concrete progress, providing the psychological reinforcement needed for long-term success.

The Sunk Cost Fallacy in Debt

Many Americans continue ineffective debt strategies because they’ve already invested time and effort, even when better options exist³. This sunk cost fallacy keeps people trapped in minimum payment cycles or inefficient consolidation plans.

Recognizing sunk cost thinking:

- “I’ve already been paying this way for two years”

- “I don’t want to waste the consolidation loan I got”

- “I’m already used to these minimum payments”

- “It would be too much work to change strategies now”

The reality is that every month of inefficient debt strategy costs hundreds in unnecessary interest. Switching to optimal strategies immediately saves money regardless of previous approache

Social Accountability and Support

Americans who share debt goals with accountability partners achieve freedom 67% faster than those who work alone³. The key is choosing the right type of accountability that provides support without judgment.

Effective accountability strategies:

- Monthly check-ins: Share progress with trusted friend or family member

- Online communities: Anonymous support groups focused on debt elimination

- Professional guidance: Financial advisors or debt counselors for complex situations

- Milestone celebrations: Acknowledge progress with supportive people

The goal isn’t public shame but private support that maintains motivation during difficult periods when debt fatigue sets in.

Habit Stacking for Debt Success

Linking debt payments to existing habits increases consistency by 73% according to behavioral psychology research¹. This approach makes debt payoff feel automatic rather than requiring constant willpower.

Habit stacking examples:

- After morning coffee: Review account balances and make extra payments

- Before Sunday meal prep: Calculate weekly debt progress

- After receiving paycheck: Transfer extra money to debt immediately

- Before monthly bills: Update debt thermometer and celebrate progress

The strength of habit stacking is that it removes decision fatigue from debt payoff, making consistent action feel effortless rather than burdensome.

Advanced Debt Elimination Techniques

The Debt Laddering Strategy

Debt laddering optimizes payment timing to minimize interest accumulation, potentially saving 15-20% on total interest costs¹. This advanced technique requires more planning but provides significant advantages for people with multiple debts.

Debt laddering implementation:

- Map payment due dates for all debts

- Time extra payments to minimize interest calculation periods

- Use grace periods strategically to reduce effective interest rates

- Coordinate with billing cycles to maximize payment impact

Mathematical advantage: Interest typically calculates on average daily balances, so payments made early in billing cycles reduce interest more than payments made near due dates.

The Balance Transfer Arbitrage

Strategic balance transfers can save thousands when executed properly, but 89% of people misuse these tools³. The key is treating transfers as temporary relief while aggressively paying down debt, not as permanent solutions.

Effective balance transfer strategy:

- Calculate total transfer costs including fees and post-promotional rates

- Ensure payoff capability before promotional rates expire

- Close or freeze original credit accounts to prevent new debt

- Make payments that eliminate transferred balances within promotional periods

Transfer optimization table:

| Original Rate | Transfer Fee | Promo Rate | Promo Period | Breakeven Point |

|---|---|---|---|---|

| 27% | 3% | 0% | 18 months | $5,000+ balance |

| 24% | 4% | 1.99% | 12 months | $3,000+ balance |

| 29% | 5% | 0% | 21 months | $7,000+ balance |

Critical warning: Balance transfers only work if you can pay off transferred balances before promotional rates expire. Otherwise, you’ll face higher rates and additional fees.

The Debt Consolidation Loan Optimization

Personal loans for debt consolidation save money for 67% of people who use them correctly, but harm 73% who use them incorrectly³. The difference lies in implementation strategy and behavioral discipline.

Successful consolidation requirements:

- Interest rate lower than weighted average of consolidated debts

- Shorter payoff timeline than current debt trajectory

- Closed credit accounts to prevent new debt accumulation

- Automated payments to ensure consistency

Consolidation loan calculation example:

- Current debts: $15,000 at various rates averaging 26%

- Consolidation loan: $15,000 at 12% over 4 years

- Monthly payment: $395 vs. $450 in minimums

- Total interest saved: $8,200 over life of debts

US Alert: Federal Reserve rate increases have made personal loan rates more expensive, currently averaging 12-15% for good credit. Ensure consolidation rates are significantly lower than current debt rates before proceeding.

The Employer Assistance Programs

43% of large employers offer debt assistance programs, but only 8% of employees use them³. These programs provide interest-free loans, financial counseling, and emergency funds that can accelerate debt elimination.

Common employer debt assistance:

- Employee assistance programs: Free financial counseling and debt management

- Hardship loans: Low or no-interest loans for debt consolidation

- Emergency funds: Grants or loans for unexpected expenses

- Financial wellness programs: Education and tools for debt management

How to access employer assistance:

- Review employee handbook for financial assistance programs

- Contact HR department about available financial wellness resources

- Speak with employee assistance program counselors

- Explore 401(k) loans as last resort for debt consolidation

Creating Your Sustainable Debt Freedom Plan

The 6-Month Debt Sprint

Intensive 6-month debt elimination efforts eliminate 40% more debt than gradual approaches, according to behavioral finance research¹. This sprint mentality creates urgency while maintaining sustainability through time-limited intensity.

6-month sprint components:

- Extreme expense reduction: Temporarily eliminate all non-essential spending

- Income maximization: Work overtime, sell assets, use windfalls

- Automated systems: Remove decision-making from daily debt payments

- Progress tracking: Weekly reviews and adjustments

Sprint sustainability strategies:

- Plan celebration: Reward yourself after 6 months of intensity

- Maintain perspective: Remember this is temporary sacrifice for permanent freedom

- Track progress: See how much debt you eliminate with focused effort

- Adjust if needed: Reduce intensity if unsustainable, but maintain consistency

The Debt Freedom Timeline Calculator

Creating realistic timelines prevents abandonment while maintaining motivation through visible progress toward specific goals¹. Most people underestimate the time required for debt elimination, leading to discouragement and strategy abandonment.

Timeline calculation factors:

- Current debt balances: Total amount owed across all debts

- Interest rates: Weighted average of all debt rates

- Available payment amount: Monthly total available for debt elimination

- Strategy chosen: Avalanche vs. snowball vs. hybrid approach

Example timeline calculation:

- Total debt: $32,000

- Monthly payment capacity: $800

- Debt avalanche strategy: 48 months to freedom

- Debt snowball strategy: 56 months to freedom

- Minimum payments only: 187 months to freedom

This mathematical reality check shows why strategic approaches matter and provides concrete timelines for planning life decisions around debt elimination.

The Lifestyle Sustainability Matrix

Debt elimination strategies must align with lifestyle realities to succeed long-term³. The sustainability matrix helps identify which approaches work for your specific situation and personality.

Sustainability factors to consider:

| Factor | High Sustainability | Medium Sustainability | Low Sustainability |

|---|---|---|---|

| Income Stability | Salary + Benefits | Hourly + Overtime | Freelance/Variable |

| Family Obligations | Single/No Kids | Married/Few Kids | Large Family |

| Expense Flexibility | High Discretionary | Some Discretionary | Mostly Fixed |

| Personality Type | Disciplined/Systematic | Motivated/Flexible | Impulsive/Emotional |

Strategy recommendations by sustainability level:

- High sustainability: Aggressive debt avalanche with 6-month sprint

- Medium sustainability: Modified avalanche with emergency buffer

- Low sustainability: Debt snowball with income acceleration focus

The Debt-Free Maintenance Plan

78% of people who achieve debt freedom accumulate new debt within 5 years without maintenance systems³. Creating post-debt-elimination structures prevents regression and builds long-term wealth.

Maintenance plan components:

- Emergency fund completion: Build 3-6 months of expenses

- Automated investing: Redirect debt payments to retirement accounts

- Credit monitoring: Track credit score improvement and maintain accounts

- Spending plan updates: Adjust budgets for debt-free lifestyle

- Annual reviews: Assess financial progress and adjust goals

The psychological transition from debt elimination to wealth building requires different mindsets and systems, but the discipline developed during debt payoff provides a foundation for long-term financial success.

Emergency Prevention and Long-term Success

The Financial Shock Absorber System

Building systems that prevent debt re-accumulation is more valuable than debt elimination alone³. The shock absorber system creates multiple layers of protection against financial emergencies that historically create new debt.

Shock absorber layers:

- Immediate buffer: $1,000 for small emergencies

- Short-term fund: 1 month expenses for larger issues

- Medium-term fund: 3-6 months expenses for job loss

- Long-term protection: Insurance and investment accounts

Implementation sequence:

- During debt payoff: Maintain $1,000 buffer

- After debt elimination: Build to 1 month expenses

- Ongoing: Gradually increase to 3-6 months over 1-2 years

- Maintenance: Replenish immediately after any use

The Wealth Building Transition

Americans who successfully transition from debt elimination to wealth building achieve financial independence 12 years faster than those who don’t have systematic approaches¹. The key is redirecting debt payment amounts to investment accounts rather than lifestyle inflation.

Transition strategy:

- Maintain payment habit: Continue “debt payments” to investment accounts

- Increase gradually: Add raises and bonuses to investment amounts

- Automate everything: Remove temptation through systematic transfers

- Track progress: Monitor investment growth like debt elimination

Psychological advantage: The discipline developed during debt payoff transfers directly to wealth building, creating compound benefits that extend far beyond debt elimination.

The Credit Score Optimization

Strategic credit management after debt elimination can improve credit scores by 100+ points within 12 months³. This improvement reduces future borrowing costs and increases access to beneficial financial products.

Credit optimization strategies:

- Maintain old accounts: Keep first credit card open for credit history length

- Low utilization: Use credit cards but pay balances monthly

- Diversified credit: Mix of credit cards, installment loans, and mortgages

- Regular monitoring: Check credit reports and dispute inaccuracies

The goal isn’t to avoid credit entirely but to use it strategically for building wealth rather than funding consumption.

Pro Tip: Use credit cards for all purchases to earn rewards, but pay balances in full monthly. This strategy maximizes credit score benefits while avoiding interest costs.

The Lifestyle Inflation Prevention

Lifestyle inflation consumes 83% of income increases for Americans who don’t have systems to prevent it³. Creating structured approaches to income growth ensures continued financial progress rather than returning to financial stress.

Inflation prevention strategies:

- Automate increases: Direct raises to investment accounts before lifestyle adjustment

- Percentage-based budgeting: Maintain fixed percentages for spending categories

- Annual reviews: Assess whether lifestyle increases align with financial goals

- Lifestyle audits: Regularly evaluate whether expenses provide proportional value

The discipline that eliminates debt can build wealth if applied consistently to income growth rather than expense growth.

Frequently Asked Questions

What’s the fastest way to pay off $25,000 in credit card debt?

The debt avalanche method combined with temporary lifestyle reduction provides the fastest payoff for most situations. For $25,000 in credit card debt at average 2025 rates (27%), you need approximately $1,100 monthly payments to eliminate debt in 24 months. This saves $18,000 in interest compared to minimum payments that would take 34 years¹.

Acceleration strategies:

- Bi-weekly payments: Reduce payoff time by 23%

- Income increases: Side jobs or overtime to increase payment amounts

- Expense reduction: Temporarily eliminate discretionary spending

- Windfall application: Use tax refunds and bonuses for debt elimination

If $1,100 monthly isn’t feasible, focus on the highest interest rate debt first while maintaining minimum payments on others.

Should I use my 401k to pay off debt?

401k withdrawals for debt payoff are rarely beneficial due to taxes, penalties, and lost compound growth. For someone under 59½, withdrawing $25,000 costs approximately $10,000 in taxes and penalties, plus $180,000 in lost retirement growth over 25 years¹.

Better alternatives:

- 401k loans: Borrow from yourself with interest payments to your account

- Hardship withdrawals: Limited circumstances with reduced penalties

- Roth IRA contributions: Withdraw contributions (not earnings) penalty-free

- Employer programs: Many companies offer financial assistance

The math almost always favors keeping retirement funds invested while using other strategies for debt elimination.

How do I handle debt when my income is irregular?

Irregular income requires different strategies that emphasize flexibility and emergency buffers. Build a larger emergency fund ($3,000-5,000) before aggressive debt payoff, and use percentage-based payments rather than fixed amounts³.

Irregular income strategies:

- Good month formula: Apply 25% of above-average income to debt

- Emergency buffer: Larger fund prevents new debt during low income periods

- Flexible payments: Minimum payments plus percentage of available income

- Income smoothing: Set aside money during good months for consistent payments

The key is maintaining momentum during low-income periods while maximizing progress during high-income months.

What if I can’t qualify for balance transfers or consolidation loans?

Poor credit limits traditional consolidation options, but alternative strategies can still provide debt elimination. Focus on the debt avalanche method, seek employer assistance programs, and consider secured credit cards to rebuild credit while paying down debt³.

Poor credit alternatives:

- Secured credit cards: Build credit while maintaining discipline

- Credit union loans: Often more flexible than bank requirements

- Peer-to-peer lending: Alternative lending platforms with different criteria

- Family loans: Formalize borrowing from family with written agreements

The most important factor is consistency in payments rather than access to specific financial products.

How do I stay motivated during a long debt payoff process?

Motivation challenges are normal during multi-year debt elimination processes. Create milestone celebrations, track progress visually, and connect with others who share similar goals to maintain momentum through difficult periods¹.

Motivation maintenance strategies:

- Milestone rewards: Celebrate every 25% of debt eliminated

- Progress visualization: Use debt thermometers or progress charts

- Community support: Join online debt elimination communities

- Why reminders: Regularly review reasons for choosing debt freedom

Remember that debt elimination is a marathon, not a sprint, and consistency matters more than perfection.

Should I pay off debt before saving for retirement?

Capture employer 401k matching first (it’s free money), then prioritize debt above 7% interest rates before additional retirement savings. For typical 2025 credit card rates around 27%, paying off debt provides a guaranteed 27% return that beats stock market averages¹.

Optimal priority sequence:

- Emergency fund: $1,000 minimum for crisis prevention

- Employer match: Free money that doubles your investment

- High-interest debt: Credit cards and personal loans above 7%

- Retirement savings: After eliminating high-interest debt

- Low-interest debt: Mortgages and student loans below 7%

This sequence maximizes both debt elimination speed and long-term wealth building.

How do I handle debt collection calls and threats?

Know your rights under the Fair Debt Collection Practices Act and maintain written communication records. Debt collectors can’t threaten arrest, wage garnishment without court orders, or call outside 8 AM-9 PM³.

Dealing with collectors:

- Request written verification: Ask for debt validation within 30 days

- Keep records: Document all communications and threats

- Know your rights: Collectors can’t harass, threaten, or deceive

- Negotiate settlements: Often accept 40-60% of original debt

Consider consulting with a consumer attorney if collectors violate federal laws or make threats beyond their legal authority.

What’s the difference between debt settlement and debt management?

Debt settlement involves negotiating to pay less than you owe, severely damaging credit for 7+ years. Debt management involves working with counselors to create payment plans, typically reducing interest rates without credit damage³.

Debt settlement consequences:

- Credit score damage: Drops 100+ points for 7 years

- Tax implications: Forgiven debt counts as taxable income

- Collection risk: Creditors may sue during settlement negotiations

- Limited success: Only works if you can pay lump sums

Debt management benefits:

- Lower interest rates: Often reduced to 6-10%

- Single payment: Simplified monthly payment to counseling agency

- Credit protection: Accounts remain current with consistent payments

- Educational support: Financial counseling and budgeting help

Debt management plans work better for people committed to paying full amounts but needing lower rates and simplified payments.

Want to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- The $5,000 Mistake: Why 71% of Gen Z Is Losing Money to Avoidable Financial Errors – The Evolving Post

- 6 Financial Strategies to Protect Your Wealth

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- 8 Powerful Financial Strategies Every Single Person Should Know

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

- Mortgage Rate Predictions 2025: When Will Rates Drop in US and Canada?

- US Canada Mortgage Rates Comparison 2025: Cross-Border Strategy Guide

Keep exploring — your smartest financial years are just getting started.

Sources:

- Federal Reserve Financial Stability Report April 2025

- Pew Research Personal Finance Outlook April 2025

- ConsumerFinance.gov Paying Down Debt Toolkit Refresh January 2025

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Individual debt situations vary significantly, and readers should consult with qualified financial professionals before making major financial decisions. Debt elimination strategies should be tailored to personal circumstances and financial goals.