The sobering reality hits hard: healthcare cost financial planning 2025 has become more critical than ever for American retirees. With the Centers for Medicare & Medicaid Services projecting healthcare spending to surge by 7.1% in 2025¹, pre-retirees and current retirees face an unprecedented financial challenge. Unlike other expenses that fluctuate, healthcare costs historically only move in one direction—upward. For the average 65-year-old couple, lifetime retirement healthcare costs could now exceed $673,000², and that’s before factoring in the additional $85,917 increase driven by recent inflation pressures³. The days of relying solely on Medicare to cover your golden years are long gone. Smart financial planning today isn’t just about having enough money—it’s about having a bulletproof strategy that can weather the storm of rising medical expenses, prescription drug costs, and insurance premium hikes that won’t break the bank.

Table of Contents

- Understanding the 2025 Healthcare Cost Landscape

- How Inflation Is Reshaping Retirement Healthcare Budgets

- Medicare Cost Changes and What They Mean for You

- Strategic Financial Planning Approaches for Rising Healthcare Costs

- Employer Insurance Transition Strategies

- Advanced Planning Strategies for High Healthcare Costs

- Frequently Asked Questions

Understanding the 2025 Healthcare Cost Landscape

The Magnitude of Healthcare Cost Increases

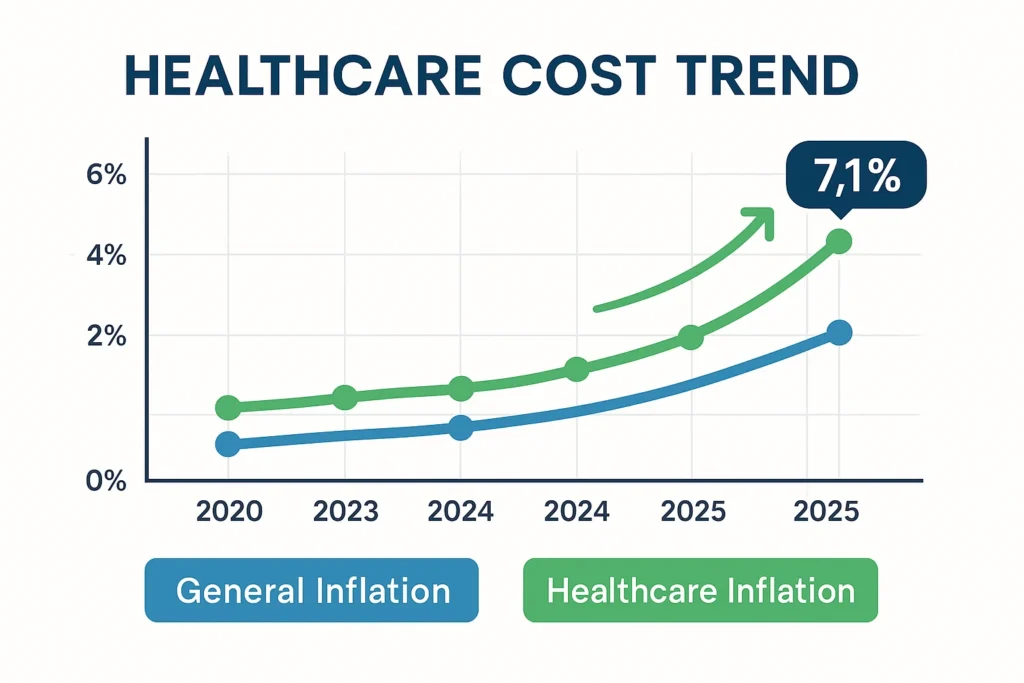

The numbers don’t lie, and they’re not pretty. Federal actuaries estimate that national health spending will increase by 7.1% in 2025, significantly outpacing GDP growth¹. This isn’t just a statistical blip—it represents the third consecutive year of healthcare cost increases above 5%, following a decade where costs averaged only around 3% annually. For American families approaching retirement, this translates into real dollars that must come from somewhere in your budget.

The ripple effects are already visible across multiple sectors. Employers surveyed by Mercer report that total health benefit costs per employee are expected to rise 5.8% on average in 2025, even after implementing cost-reduction measures⁴. Without these measures, costs would jump by approximately 7%—a figure that would make your current employer-sponsored coverage significantly more expensive. This trend shows no signs of slowing down, and that ship has sailed when it comes to hoping for cost stability.

Key Cost Drivers You Need to Know

Several interconnected factors are pushing healthcare costs skyward. The ongoing shortage of healthcare workers continues to drive up service prices as providers compete for qualified staff. Meanwhile, the introduction of expensive gene and cellular therapies—some costing over $1 million per treatment—is creating unprecedented cost pressures⁵. Additionally, the surge in demand for behavioral health services and popular GLP-1 weight loss medications is contributing to overall cost increases.

Prescription drug spending remains particularly concerning, with employer drug benefit costs per employee rising 7.2% in 2024 alone⁶. This acceleration in pharmaceutical costs is driven by specialty drugs, biosimilars entering the market at higher-than-expected prices, and increased utilization of mental health medications post-pandemic.

US Alert: The FDA approved 55 new drugs in 2024, with an average launch price of $180,000 per year. Many of these medications target chronic conditions common in older adults, directly impacting retirement healthcare budgets.

How Inflation Is Reshaping Retirement Healthcare Budgets

The Compound Effect of Healthcare Inflation

Healthcare inflation operates differently from general inflation, and the impact on retirement budgets is profound. Research from HealthView Services reveals that even short periods of high inflation create long-term consequences for healthcare costs⁷. For a healthy 55-year-old couple retiring in 10 years, assuming just two years of healthcare cost inflation at 1.5 times the Consumer Price Index, lifetime retirement healthcare costs will increase by $160,712 to over $1 million total³.

The mathematics are unforgiving. Unlike gasoline or food prices that can decrease during economic downturns, healthcare costs historically only increase. This one-way escalator means that every dollar of healthcare inflation compounds over your entire retirement period, potentially lasting 20-30 years or more. Current projections suggest that healthcare costs will consume 18.7% of GDP by 2032¹, up from approximately 17.8% in 2025.

Real-World Budget Impact

Current retirees are already feeling the squeeze. According to the Schroders 2025 U.S. Retirement Survey, 45% of retirees report that their expenses are higher than expected, with 62% admitting they have no idea how long their savings will last⁸. More concerning, retirees are now spending an average of 15% of their total monthly income on healthcare costs, including insurance premiums, prescriptions, and out-of-pocket expenses.

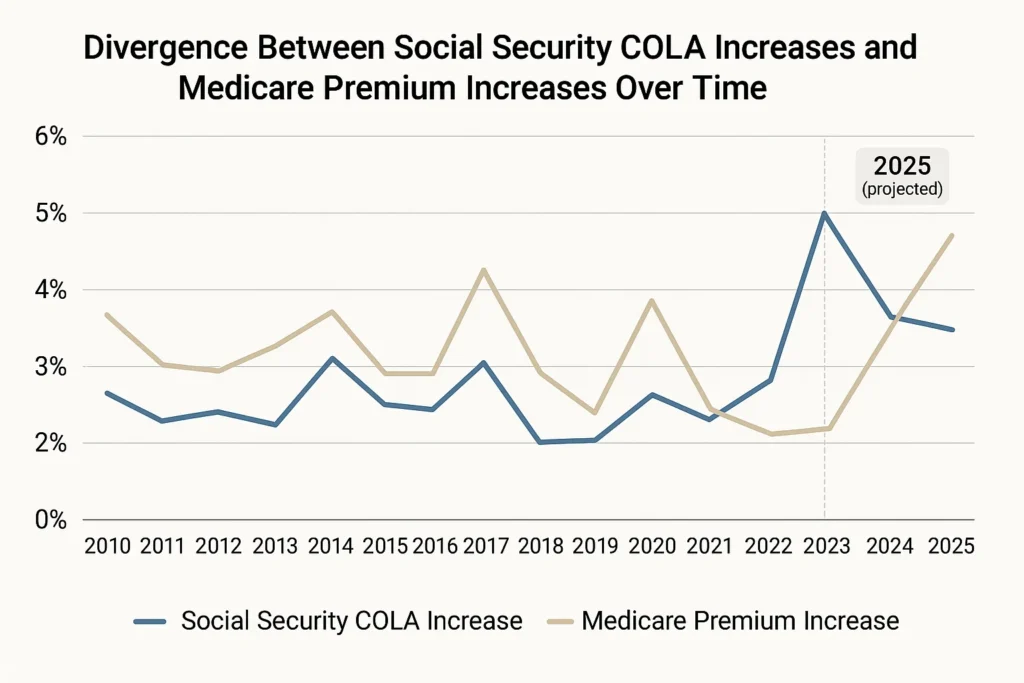

The situation becomes even more challenging when you consider that Social Security cost-of-living adjustments rarely keep pace with healthcare inflation. While the 2025 COLA increased benefits by 2.5%, Medicare Part B premiums rose by 5.9%, creating a net reduction in purchasing power for many retirees⁹.

| Age Group | Additional Lifetime Healthcare Costs Due to Inflation | Total Projected Costs | Monthly Impact |

|---|---|---|---|

| 45-year-old couple | $259,808³ | $1,770,276³ | $7,380 |

| 55-year-old couple | $160,712³ | $1,073,717³ | $4,474 |

| 65-year-old couple | $85,917³ | $673,587³ | $2,807 |

Expert Insight

“Even when adjusted for higher Social Security COLAs, the portion of retirement budgets required to cover healthcare will be significantly higher than most expect. Unlike other consumer goods and services, healthcare costs historically do not increase and decrease—they only go up.”

— Ron Mastrogiovanni, Founder and CEO, HealthView Services

Medicare Cost Changes and What They Mean for You

Medicare Premium and Deductible Increases

Medicare beneficiaries face significant cost increases in 2025 that will directly impact monthly budgets. Medicare Part B monthly premiums rose to $185.00, marking a $10.30 increase from 2024’s $174.70⁹. The annual deductible also jumped to $257, up $17 from the previous year. For many retirees living on fixed incomes, these increases represent a meaningful percentage of their monthly Social Security payments.

The timing couldn’t be worse. While retirees received a Social Security cost-of-living adjustment of 2.5%, Medicare premiums rose by 5.9%—more than double the COLA increase. This scissors effect, where Medicare costs rise faster than Social Security benefits, is becoming a persistent challenge for retirement financial planning. Over the past decade, Medicare Part B premiums have increased at an average annual rate of 5.9%, compared to Social Security COLAs averaging just 2.6%.

Out-of-Pocket Cost Projections

The Medicare cost increases extend beyond premiums. CMS projects that per capita out-of-pocket spending will continue rising across all services through 2032¹⁰. Out-of-pocket hospital services spending per capita is projected to increase at an average rate of 2.9% per year, reaching $152 per capita by 2032. Similarly, physician and clinical services out-of-pocket spending is expected to increase at 3.5% annually, rising from $226 per capita in 2024 to $298 by 2032.

Medicare Advantage plans, while potentially offering additional benefits, are also experiencing premium increases. The average Medicare Advantage premium is expected to rise 13% in 2025, though this varies significantly by region and plan type¹¹. These increases come despite Medicare Advantage plans receiving higher government payments per beneficiary.

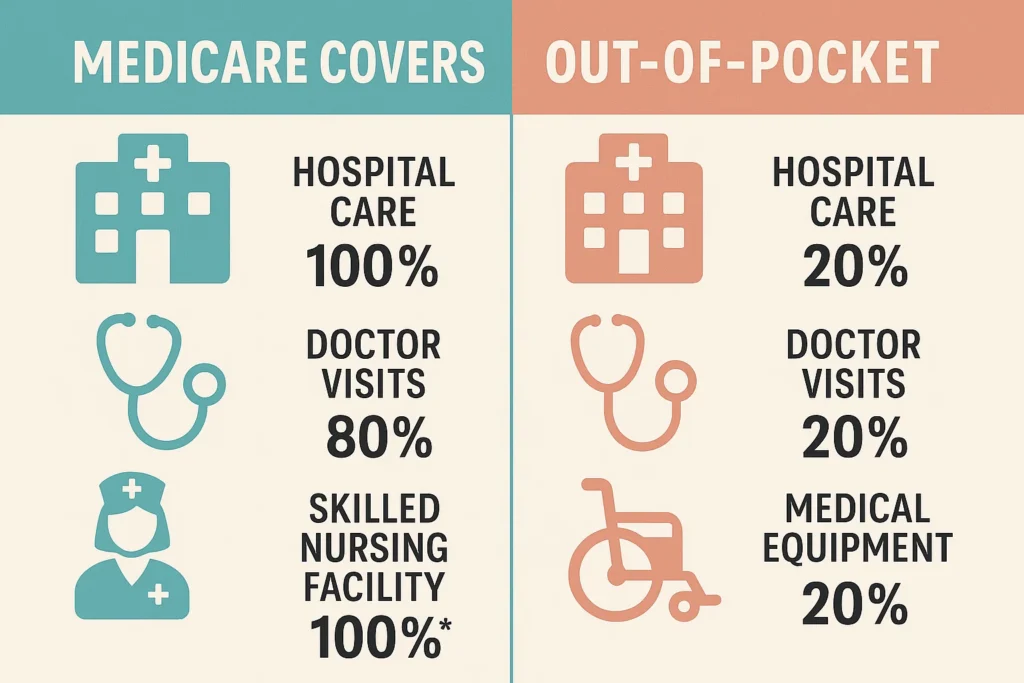

Pro Tip: Among surveyed retirees, 58% expected Medicare to cover more of their healthcare expenses than it actually does. Don’t make this costly assumption in your planning—Medicare typically covers only about 60% of total healthcare costs.

Strategic Financial Planning Approaches for Rising Healthcare Costs

The Health Savings Account Advantage

Health Savings Accounts (HSAs) remain one of the most powerful tools for healthcare cost financial planning 2025. These accounts offer triple tax advantages: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. For individuals 55 and older, catch-up contributions allow an additional $1,000 annually, bringing the total contribution limit to $4,550 for individual coverage in 2025.

The key strategy shift involves treating your HSA as a retirement account rather than a current expense account. By paying current medical expenses out-of-pocket and allowing HSA funds to grow invested, you create a substantial healthcare nest egg. After age 65, HSA funds can be withdrawn for any purpose (though non-medical withdrawals are subject to regular income tax), making it effectively a second IRA with superior tax treatment for medical expenses.

Consider the power of compound growth: a 45-year-old who contributes the maximum to an HSA for 20 years and earns a 7% annual return would accumulate approximately $247,000 by age 65, assuming no withdrawals. This amount alone could cover the majority of lifetime healthcare costs for many retirees.

Creating Healthcare-Specific Emergency Funds

Traditional financial advice suggests three to six months of expenses in an emergency fund, but healthcare costs require a specialized approach. Given the unpredictability of medical expenses and the fact that Medicare doesn’t cover everything, maintaining a separate healthcare emergency fund becomes crucial.

Financial planners now recommend maintaining at least $50,000-$75,000 specifically earmarked for healthcare emergencies. This fund should be in addition to your regular emergency savings and should be readily accessible through high-yield savings accounts or short-term CDs. The fund should cover potential scenarios like unexpected medical procedures not covered by insurance, prescription drugs during Medicare coverage gaps, or the need for immediate care while traveling.

Long-Term Care Insurance Considerations

The elephant in the room for many retirees is long-term care costs, which Medicare generally doesn’t cover. With the average cost of a private nursing home room exceeding $108,405 annually nationwide¹², and reaching over $150,000 in states like Alaska and Massachusetts, long-term care insurance becomes a critical component of comprehensive healthcare financial planning.

Traditional long-term care insurance has become more expensive and harder to obtain, leading many financial planners to recommend hybrid life insurance policies with long-term care benefits. These policies provide death benefits if long-term care isn’t needed, making them more attractive to many retirees who worry about “use it or lose it” scenarios.

US Alert: Approximately 70% of Americans over age 65 will need some form of long-term care services during their lifetime, yet most have no plan to pay for these costs beyond hoping Medicare will cover them—which it won’t for custodial care.

Employer Insurance Transition Strategies

COBRA vs. Medicare Timing Decisions

For Americans approaching 65 while still employed or recently retired, the timing of Medicare enrollment versus COBRA continuation presents critical financial decisions. COBRA allows you to continue your employer’s group health insurance for up to 18 months (or 36 months in certain circumstances), but you’ll pay the full premium plus a 2% administrative fee.

With employer healthcare costs rising 5.8% in 2025⁴, COBRA premiums will reflect these increases. The average COBRA premium for family coverage now exceeds $22,221 annually¹³, making it one of the most expensive health insurance options available. However, delaying Medicare enrollment can result in late enrollment penalties that last for life. The Medicare Part B penalty is 10% of the premium for each 12-month period you were eligible but didn’t enroll.

Retiree Health Plan Evaluation

Many large employers offer retiree health plans, but these benefits are becoming less generous and more expensive. Only 23% of large employers now offer retiree health benefits, down from 40% in the 1990s¹⁴. Employers are increasingly shifting costs to retirees or eliminating these benefits entirely due to rising costs and accounting requirements.

If your employer offers retiree health benefits, compare them carefully against Medicare Advantage or Medicare Supplement options. Consider factors beyond just premium costs: prescription drug coverage, provider networks, out-of-pocket maximums, and coverage for services like dental and vision. Many retiree plans coordinate with Medicare as the primary payer, which can create coverage gaps or complications.

Pro Tip: Don’t assume your employer’s retiree health plan is automatically your best option. Run side-by-side comparisons with Medicare options during your employer’s open enrollment period and Medicare’s Annual Open Enrollment (October 15 – December 7).

Advanced Planning Strategies for High Healthcare Costs

Geographic Arbitrage for Healthcare Costs

Healthcare costs vary dramatically across different regions of the United States, creating opportunities for strategic retirement location planning. According to the Medicare trustees’ report, Medicare Advantage premiums can vary by over 300% between different counties¹⁵. Similarly, Medigap supplement insurance costs can differ by $200+ monthly between states for identical coverage.

States like Wisconsin, Hawaii, and Iowa consistently rank among the most affordable for healthcare costs, while states like Alaska, Wyoming, and parts of California and New York rank among the most expensive. However, the calculation isn’t simply about finding the cheapest healthcare—you must also consider state income taxes, property taxes, overall cost of living, and proximity to quality healthcare facilities.

Self-Insurance Strategies for High-Income Retirees

For retirees with substantial assets, self-insuring certain healthcare risks can provide significant savings over traditional insurance approaches. This strategy involves maintaining larger cash reserves to cover potential medical expenses while purchasing only catastrophic coverage for major medical events.

The mathematics work particularly well for healthy retirees with over $2 million in retirement assets. By choosing high-deductible Medicare supplement plans and maintaining substantial healthcare emergency funds, these retirees can often save $5,000-$10,000 annually in premium costs while maintaining adequate protection against catastrophic expenses.

Tax-Efficient Healthcare Spending Strategies

The order in which you withdraw retirement funds to pay for healthcare expenses can significantly impact your overall tax burden. Healthcare expenses create unique opportunities for tax-efficient withdrawal strategies, particularly when combined with itemized deductions for medical expenses exceeding 7.5% of adjusted gross income.

For retirees in higher tax brackets, timing large medical procedures or expenses can create tax benefits through medical expense deductions. Additionally, using pre-tax retirement account withdrawals to pay for healthcare can sometimes result in lower overall taxes than using after-tax savings, particularly when medical expenses are substantial.

Frequently Asked Questions

How much should I budget for healthcare costs in retirement?

Financial planners recommend budgeting 15-20% of your retirement income for healthcare costs, but this percentage is rising due to inflation¹⁶. For a couple retiring in 2025, lifetime healthcare costs could exceed $675,000³, requiring monthly savings of approximately $2,800-$3,000 throughout retirement. However, these are averages—your actual costs may be higher or lower depending on your health status, location, and insurance choices.

What’s the biggest mistake people make in healthcare financial planning?

The most common error is underestimating Medicare’s coverage gaps. Many Americans assume Medicare will cover most healthcare costs, but it typically covers only about 60% of total expenses. Failing to plan for premiums, deductibles, copays, and uncovered services like long-term care can derail retirement finances. Additionally, many people don’t account for healthcare inflation, which historically runs 2-3 percentage points higher than general inflation.

Should I max out my HSA contributions if I’m approaching retirement?

Yes, if financially possible. HSAs offer unmatched tax advantages for healthcare expenses and function as excellent retirement accounts. For those 55 and older, catch-up contributions provide additional savings opportunities. The key is treating your HSA as a long-term investment vehicle rather than a current expense account. Every dollar you contribute reduces your current taxable income and can grow tax-free for decades.

How do I protect my healthcare budget from inflation?

Diversification is key. Consider investments that historically outpace healthcare inflation, maintain adequate emergency funds specifically for medical expenses, and review your insurance coverage annually. Healthcare REITs and pharmaceutical company stocks can provide some inflation protection, though they shouldn’t constitute your entire strategy. Additionally, maximizing HSA contributions and delaying Social Security to increase future benefits can help offset healthcare inflation.

Is long-term care insurance worth the cost?

For most middle-class retirees, some form of long-term care protection is essential. Traditional long-term care insurance works best for people in their 50s and early 60s who are still healthy. For older adults or those with health issues, hybrid life insurance policies with long-term care riders may be better options. The key is understanding that Medicare doesn’t cover custodial care, and the average cost of care can easily exceed $100,000 annually.

When should I switch from employer insurance to Medicare?

The timing depends on your specific situation. If you’re still working and have employer insurance that covers you adequately, you may delay Medicare Part B without penalty as long as you have qualifying employer coverage. However, once you retire or your employer coverage ends, you have an 8-month special enrollment period to sign up for Medicare without penalties. Delaying beyond this period results in permanent premium penalties.

Conclusion

Mastering healthcare cost financial planning 2025 isn’t optional—it’s essential for retirement security. With healthcare spending projected to grow 7.1% this year and Medicare premiums rising faster than Social Security benefits, the time for comprehensive planning is now. The strategies outlined here—from maximizing HSA contributions to creating healthcare-specific emergency funds—provide a roadmap for navigating these challenging financial waters.

The sobering reality is that healthcare will likely consume a larger portion of your retirement budget than you initially planned. However, with proper preparation, strategic use of tax-advantaged accounts, and careful insurance planning, you can maintain your financial security even as healthcare costs continue rising. Don’t let rising healthcare costs catch you off guard—start implementing these strategies today, and consider consulting with a fee-only financial planner who specializes in retirement healthcare planning. Your future self will thank you for taking action now rather than hoping things will somehow work out. The ship of hoping Medicare covers everything has already sailed, but the ship of smart planning is still in port, waiting for you to board.

ant to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- Emergency Fund Calculator Inflation 2025: Your Complete Guide to Financial Security

- Cryptocurrency Investment Guide 2025: Why Search Volume Jumped 112% This Year

- Student Loan Forgiveness 2025: Critical Updates Every Borrower Must Know

- The $5,000 Mistake: Why 71% of Gen Z Is Losing Money to Avoidable Financial Errors – The Evolving Post

- Debt Payoff Strategies 2025 That Actually Work: Why 44% of Americans Stay Trapped in 2025 – The Evolving Post

- 6 Financial Strategies to Protect Your Wealth

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

- Mortgage Rate Predictions 2025: When Will Rates Drop in US and Canada?

- US Canada Mortgage Rates Comparison 2025: Cross-Border Strategy Guide

Keep exploring — your smartest financial years are just getting started.

Sources:

1. CMS National Health Expenditure Projections

2. Health System Tracker – Healthcare Spending Growth

3. HealthView Services – Inflation Impact on Retiree Healthcare Costs

4. Mercer 2025 Healthcare Cost Survey

5. WTW Global Medical Trends Survey 2025

6. Brown & Brown 2025 Healthcare Cost Analysis

7. Plan Sponsor – Healthcare Inflation Impact

8. Investment News – Retiree Healthcare Cost Survey

9. Medicare.gov – 2025 Premium Changes

10. CMS Out-of-Pocket Spending Projections

11. Kaiser Family Foundation – Medicare Advantage 2025

12. Genworth Cost of Care Survey 2025

13. Health System Tracker – COBRA Premium Analysis

14. Aon Global Medical Trend Report 2025

15. CMS Medicare Geographic Cost Analysis

16. PwC Healthcare Cost Forecast 2025