About This Guide: This comprehensive article is thoroughly researched using official government sources including the Consumer Financial Protection Bureau, Federal Trade Commission, and state DMV requirements to provide accurate, up-to-date information for American consumers.

Table of Contents

- Understanding Financed Car Trade-Ins

- Negative Equity: What It Means for Your Trade-In

- The Trade-In Process with Outstanding Loans

- Dealer Payoff Requirements and Timeframes

- Protecting Yourself from Trade-In Scams

- Alternatives to Trading in Your Financed Car

- Frequently Asked Questions

Yes, you can trade in a financed car, but the process requires careful consideration of your loan balance, vehicle value, and potential negative equity. According to the Consumer Financial Protection Bureau, approximately 44% of Americans trade in vehicles with outstanding loan balances, making this a common automotive financing scenario.

The key to a successful financed car trade-in lies in understanding your equity position and the dealer’s obligations. Whether you have positive or negative equity will significantly impact your options and the financial implications of your trade-in decision.

Understanding Financed Car Trade-Ins

When you trade in a financed car, you’re essentially transferring both the vehicle and its associated debt obligations. The Consumer Financial Protection Bureau emphasizes that understanding your payoff amount is crucial before initiating any trade-in negotiations.

Key Components of a Financed Trade-In

Your financed car trade-in involves three critical values:

- Payoff amount: The total remaining balance on your existing loan

- Trade-in value: What dealers are willing to pay for your vehicle

- Equity position: The difference between these two amounts

According to Federal Trade Commission guidelines, dealers must clearly disclose how they handle your existing loan balance in any new financing arrangement.

Positive vs. Negative Equity Scenarios

Positive equity occurs when your car’s trade-in value exceeds your loan payoff amount. This scenario provides you with credit toward your new vehicle purchase, reducing the amount you need to finance.

Negative equity, conversely, means you owe more than your car is worth. The FTC reports that negative equity situations affect approximately 33% of trade-in transactions, often resulting from rapid depreciation or extended loan terms.

Negative Equity: What It Means for Your Trade-In

Negative equity, also known as being “underwater” or “upside-down” on your loan, presents unique challenges when trading in a financed car. The Federal Trade Commission provides detailed guidance on how dealers typically handle these situations.

How Dealers Handle Negative Equity

When you have negative equity, dealers may offer to “pay off” your existing loan, but this arrangement often involves rolling the negative equity into your new loan. This practice increases both your total loan amount and monthly payments, as you’ll pay interest on the negative equity amount plus your new vehicle’s price.

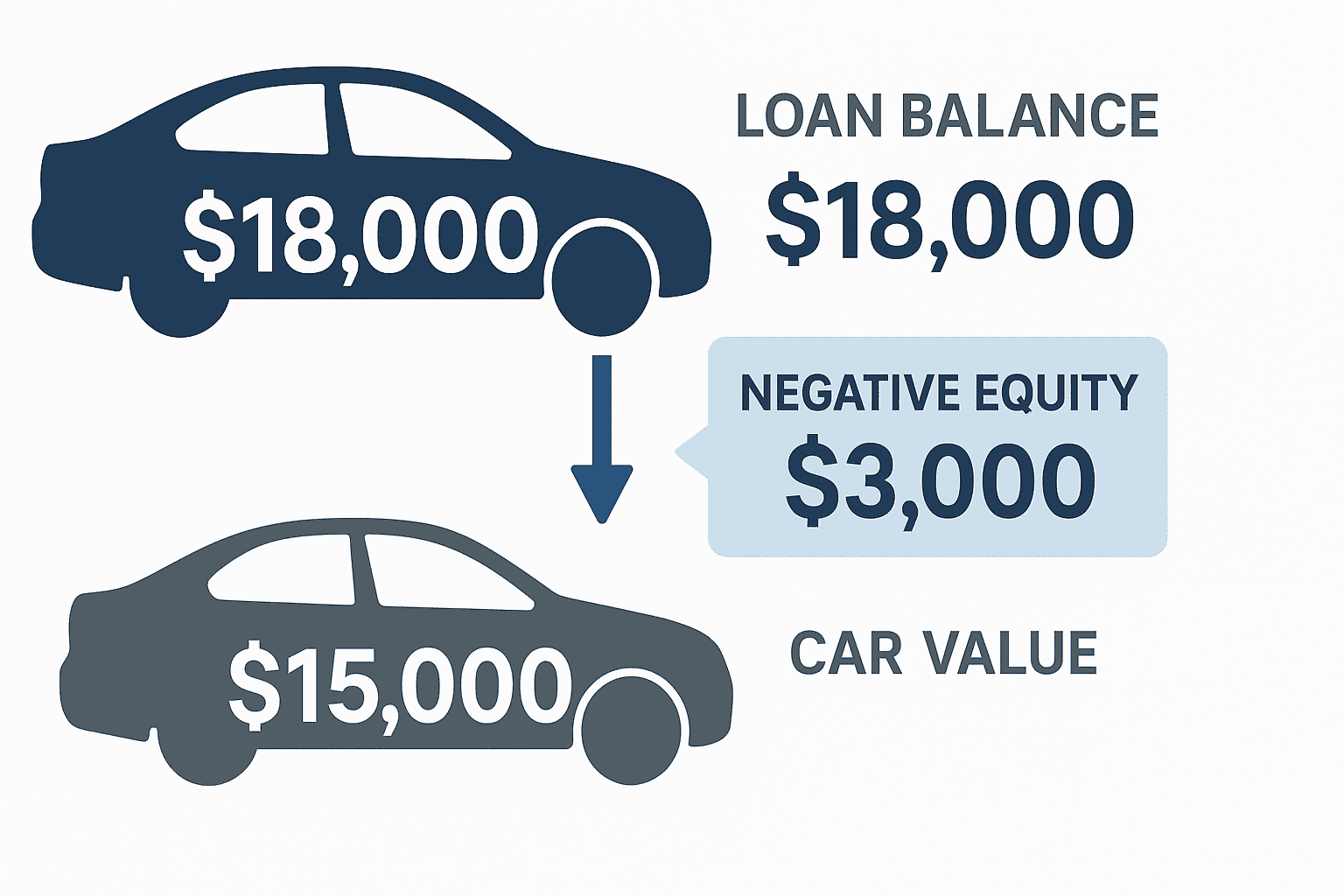

For example, if you owe $18,000 on your current car but it’s only worth $15,000, you have $3,000 in negative equity. The Consumer Financial Protection Bureau warns that dealers may add this $3,000 to your new car financing, significantly increasing your total debt burden.

Warning Signs of Predatory Practices

The FTC identifies several red flags in negative equity situations:

- Promises to “make your loan disappear” without clear documentation

- Failure to disclose how negative equity affects new financing terms

- Pressure to sign contracts without adequate time for review

The Trade-In Process with Outstanding Loans

Trading in a financed car requires careful coordination between you, the dealer, and your existing lender. Understanding this process helps ensure smooth transactions and protects your financial interests.

Step-by-Step Trade-In Process

- Obtain your payoff quote: Contact your current lender for an exact payoff amount, including any daily interest charges

- Research your vehicle’s value: Use resources like FTC-recommended valuation tools including NADA Guides, Edmunds, and Kelley Blue Book

- Calculate your equity position: Determine whether you have positive or negative equity

- Negotiate the trade-in value: Keep trade-in negotiations separate from new car pricing discussions

Documentation Requirements

Proper documentation is essential for financed car trade-ins. You’ll need:

- Current loan payoff statement

- Vehicle title (if available) or lienholder information

- Registration and insurance documents

- Maintenance records to support your vehicle’s value

The Utah Department of Motor Vehicles requires dealers to notify lienholders within 7 days of accepting a trade-in and pay off existing loans within 21 calendar days or 15 days of receiving payment, whichever comes first.

Dealer Payoff Requirements and Timeframes

When dealers accept financed vehicles as trade-ins, they assume legal obligations to handle existing loan payoffs properly. Understanding these requirements protects you from potential financial complications.

Legal Obligations and Timeframes

State regulations vary, but most jurisdictions impose strict deadlines on dealer payoff responsibilities. The Utah DMV serves as a model, requiring dealers to:

- Notify lienholders within 7 days of trade-in acceptance

- Complete loan payoffs within 21 calendar days of sale or 15 days of receiving payment

- Provide written notification if sales are rescinded within 5 calendar days

Consequences of Delayed Payoffs

When dealers fail to meet payoff deadlines, you remain legally responsible for the original loan payments. The Georgia Department of Consumer Affairs warns that delayed payoffs can result in:

- Continued loan payments on vehicles you no longer possess

- Credit score damage from missed payments

- Additional interest and late fees on the original loan

Protecting Your Interests

To safeguard against dealer negligence:

- Obtain written confirmation of payoff responsibilities

- Monitor your original loan account for timely payoff

- Maintain contact with your original lender during the transition period

- Document all communications with the dealership regarding payoff arrangements

Protecting Yourself from Trade-In Scams

The complexity of financed car trade-ins creates opportunities for unscrupulous dealers to exploit consumers. Recognizing common scams and understanding your rights provides essential protection.

Common Trade-In Scams

The Federal Trade Commission identifies several prevalent schemes:

Phantom Payoffs: Dealers promise to handle loan payoffs but fail to follow through, leaving consumers responsible for payments on vehicles they no longer possess.

Hidden Negative Equity: Dealers obscure how negative equity affects new financing terms, resulting in unexpectedly high monthly payments or extended loan terms.

Conditional Financing Manipulation: Dealers use “conditional” financing arrangements to pressure consumers into unfavorable terms after taking possession of trade-in vehicles.

Red Flags to Watch

University of Rhode Island finance professor Nilton Porto advises consumers to be wary of dealers who pressure you to disclose payment capabilities, trade-in values, or down payment amounts before negotiating vehicle prices. Additional warning signs include:

- Reluctance to provide written payoff guarantees

- Pressure to sign contracts immediately without review time

- Excessive add-on products that increase financing amounts

Your Legal Protections

Federal and state consumer protection laws provide recourse against fraudulent trade-in practices. The Georgia Consumer Affairs Department notes that under the Holder Rule, finance companies may be subject to claims against dealerships when financing is arranged through the dealer.

Alternatives to Trading in Your Financed Car

While trading in a financed car offers convenience, alternative approaches may provide better financial outcomes, particularly in negative equity situations.

Private Sale Considerations

Selling your financed car privately often yields higher returns than dealer trade-ins. Texas A&M financial expert Nick Kilmer notes that private sales “may earn you significantly more money” compared to wholesale trade-in values.

However, private sales of financed vehicles require coordination with your lender to handle title transfers and loan payoffs. You’ll need to:

- Obtain payoff quotes valid for specific timeframes

- Arrange for buyer financing verification

- Coordinate simultaneous payment and title transfer processes

Loan Acceleration Strategies

The Consumer Financial Protection Bureau suggests considering loan acceleration to reach positive equity before trading. This approach involves:

- Making additional principal-only payments

- Applying windfalls or bonuses to loan reduction

- Refinancing to lower interest rates and shorter terms

Lease-End Alternatives

For consumers currently leasing vehicles, the Federal Reserve outlines end-of-term options including purchase, return, or lease extension. Understanding these alternatives helps inform decisions about transitioning to ownership or continuing lease arrangements.

Frequently Asked Questions

Can you trade in a financed car with negative equity?

Yes, you can trade in a financed car with negative equity, but the remaining loan balance typically gets rolled into your new car financing. According to the Federal Trade Commission, this increases your total loan amount and monthly payments, as you’ll pay interest on both the negative equity and your new vehicle’s price.

How long does a dealer have to pay off my trade-in loan?

Dealer payoff timeframes vary by state, but most require completion within 21 calendar days of the sale or 15 days of receiving payment, whichever comes first. The Utah Department of Motor Vehicles also requires dealers to notify lienholders within 7 days of accepting the trade-in.

What happens if the dealer doesn’t pay off my trade-in loan?

If a dealer fails to pay off your trade-in loan, you remain legally responsible for the payments even though you no longer possess the vehicle. The Georgia Department of Consumer Affairs advises immediately contacting both your original lender and the finance company for your new vehicle to resolve the situation.

Should I get pre-approved financing before trading in my financed car?

Yes, obtaining pre-approved financing gives you negotiating power and ensures you understand your true financing costs. The Consumer.gov recommends contacting multiple lenders including banks and credit unions to compare rates before visiting dealers.

Can I negotiate the trade-in value of my financed car?

Absolutely. The Federal Trade Commission recommends researching your vehicle’s value using NADA Guides, Edmunds, and Kelley Blue Book, then negotiating trade-in value separately from new car pricing to ensure dealers don’t adjust sales prices to compensate for generous trade-in offers.

Is it better to pay off my car loan before trading in?

If you have positive equity (owe less than the car’s value), the Consumer Financial Protection Bureau recommends paying off your existing loan before getting new financing to avoid potential complications and ensure clear ownership transfer.

ant to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- Cryptocurrency Investment Guide 2025: Why Search Volume Jumped 112% This Year

- Healthcare Cost Financial Planning 2025: Complete Guide for American Retirees

- Emergency Fund Calculator Inflation 2025: Your Complete Guide to Financial Security

- Student Loan Forgiveness 2025: Critical Updates Every Borrower Must Know

- The $5,000 Mistake: Why 71% of Gen Z Is Losing Money to Avoidable Financial Errors – The Evolving Post

- Debt Payoff Strategies 2025 That Actually Work: Why 44% of Americans Stay Trapped in 2025 – The Evolving Post

- 6 Financial Strategies to Protect Your Wealth

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

- Mortgage Rate Predictions 2025: When Will Rates Drop in US and Canada?

- US Canada Mortgage Rates Comparison 2025: Cross-Border Strategy Guide

Keep exploring — your smartest financial years are just getting started.

Sources

- Consumer Financial Protection Bureau – Should I trade in my car if it’s not paid off?

- Federal Trade Commission – Auto Trade-Ins and Negative Equity

- Georgia Department of Consumer Affairs – Vehicle Trade-Ins

- Consumer Financial Protection Bureau – Car Buying Skills for Servicemembers

- Federal Trade Commission – Financing or Leasing a Car

- Utah Department of Motor Vehicles – Trade-in Payoff Requirements

- Texas A&M University – 5 Tips for Car-Buying

- Consumer.gov – Getting a Car Loan