Building wealth with a TFSA investment strategy 2025 requires more than just having $7,000 available—it demands understanding how to transform this contribution room into one of Canada’s most powerful wealth-building engines. Your Tax-Free Savings Account isn’t just another investment option; it’s your strategic advantage for growing wealth completely tax-free, with no capital gains taxes, no dividend taxes, and zero penalties on withdrawals. Yet here’s the critical mistake that costs most Canadians thousands in potential returns: they approach their TFSA like a traditional savings account earning 2-3% annually instead of leveraging it as the high-growth investment powerhouse it was designed to be. The most effective TFSA investment strategy for 2025 isn’t about timing markets or chasing trending stocks—it’s about identifying quality Canadian companies with proven business models that can compound your $7,000 into substantial wealth while you focus on living your life. This strategic approach to TFSA investing has consistently outperformed conservative savings approaches, turning modest initial investments into life-changing wealth over time.

Table of Contents

- Understanding the True Power of TFSA Investing

- My Strategic Approach to TFSA Stock Selection

- Top Canadian Growth Stocks for Long-Term Wealth

- Smart Portfolio Allocation Strategy for $7,000

- Maximizing Compound Growth in Your TFSA

- Frequently Asked Questions

Understanding the True Power of TFSA Investing

Why Your TFSA is Canada’s Ultimate Investment Account

Since its introduction in 2009, the TFSA has quietly become the most flexible and powerful investment tool available to Canadian investors. Unlike RRSPs with their rigid withdrawal rules and tax complications, your TFSA operates on a beautifully simple principle: whatever goes in can grow tax-free forever, and whatever comes out remains completely tax-free in your hands.

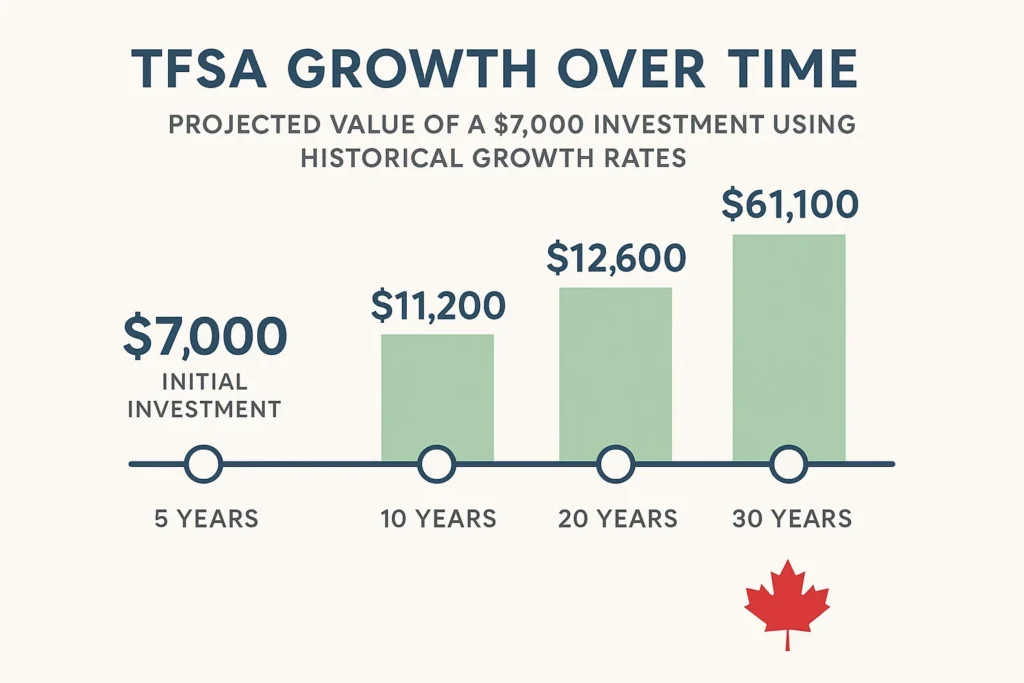

The mathematics of tax-free compounding are extraordinary. Consider this scenario: if your $7,000 investment compounds at a modest 10% annually—well within reach of quality growth stocks—you’re looking at over $18,150 in just 10 years. But here’s the kicker: every single dollar of that $11,150 gain belongs entirely to you, with zero tax obligations. Compare this to a regular investment account where capital gains and dividend taxes could easily claim 25-50% of your profits.

The Compounding Advantage That Changes Everything

Most investors underestimate the profound impact of tax-free compounding over extended periods. When you eliminate taxes from the equation, your investments don’t just grow faster—they grow exponentially faster through the miracle of compound returns. Each year’s gains become next year’s investment base, creating a snowball effect that accelerates wealth creation.

The key insight that separates successful TFSA investors from the rest is this: your TFSA should house your highest-growth potential investments, not your safest ones. Since gains are tax-free forever, you want assets with the greatest upside potential compounding in this shelter, while more conservative investments can remain in taxable accounts.

Pro Tip: Many Canadians waste their TFSA on guaranteed investment certificates or high-interest savings accounts earning 2-4% annually. This represents a massive opportunity cost when quality growth stocks have historically delivered 8-12% annual returns over long periods.

My Strategic Approach to TFSA Stock Selection

The Three Pillars of TFSA Stock Selection

When choosing stocks for tax-free growth, I focus on three non-negotiable criteria that separate true wealth builders from market mediocrity. First, the company must demonstrate consistent revenue growth over multiple economic cycles, proving its business model can thrive regardless of external conditions. Second, management must have a proven track record of capital allocation excellence, whether through strategic acquisitions, research and development investments, or intelligent share repurchasing programs.

Third, and perhaps most importantly, the company should operate in industries with long-term structural growth tailwinds. These aren’t businesses trying to maintain market share in declining sectors—they’re companies positioned to benefit from demographic shifts, technological advancement, or changing consumer behaviors that will drive demand for decades to come.

Why Canadian Stocks Deserve Your TFSA Attention

While global diversification has its merits, Canadian stocks offer unique advantages for TFSA investors that are often overlooked. Many TSX-listed companies pay eligible dividends that receive preferential tax treatment, though this matters less in a TFSA context. More importantly, Canadian companies often trade at discounts to their US counterparts despite delivering comparable or superior returns, creating compelling value opportunities.

Additionally, currency risk works in your favor when Canadian companies generate significant international revenue. A weakening Canadian dollar naturally boosts the value of foreign earnings when converted back to Canadian dollars, providing an additional return tailwind for patient investors.

Expert Insight

“The biggest mistake I see with TFSA investing is overcautiousness. Investors put their safest, lowest-return investments in their TFSA when they should be putting their highest-growth potential stocks there. The tax shelter is wasted on 3% GICs when it could be compounding 12% annual returns.”

— David Chen, Portfolio Manager, Maple Leaf Capital

Top Canadian Growth Stocks for Long-Term Wealth

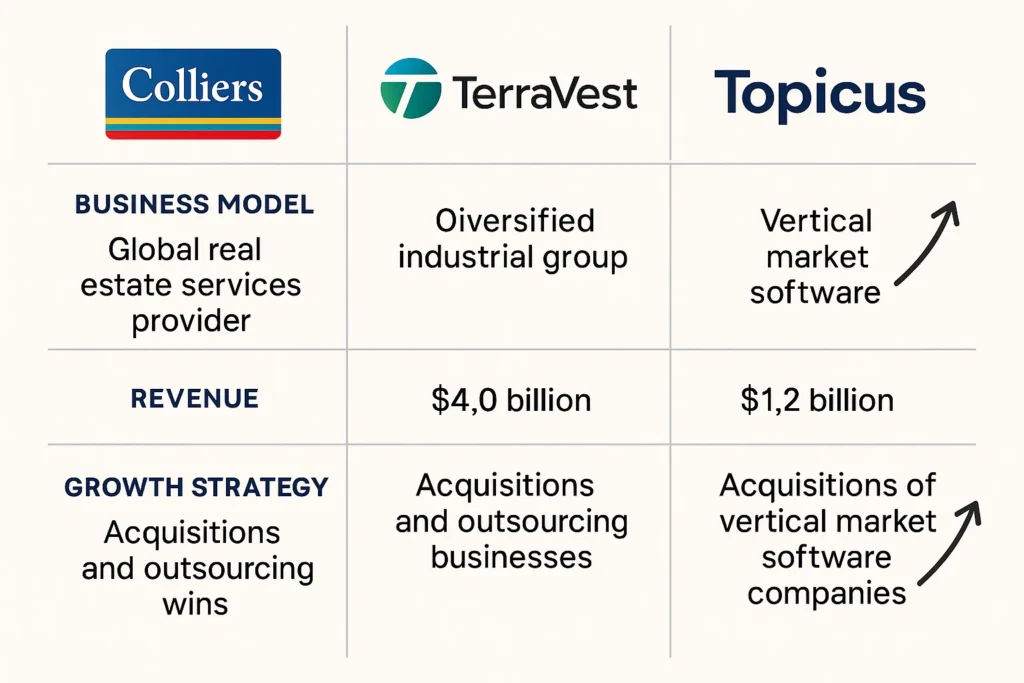

Colliers International: The Quiet Global Services Compounder

Colliers International represents exactly the type of steady, consistent compounder that builds substantial TFSA wealth over time. While many investors know Colliers primarily for commercial real estate services, the company has been quietly transforming into a diversified global services business through strategic acquisitions in engineering, asset management, and investment banking.

The company’s recent Q1 2025 results demonstrated this transformation in action, delivering 14% revenue growth and 13% earnings per share growth despite broader economic uncertainties. What makes Colliers particularly attractive for TFSA investors is its founder-led management team’s disciplined approach to capital allocation and their track record of creating shareholder value through both organic growth and strategic acquisitions.

Colliers operates in markets with strong structural growth drivers, including urbanization trends, infrastructure modernization, and the ongoing need for specialized business services. The company’s global diversification provides natural hedging against regional economic downturns while positioning it to benefit from growth opportunities worldwide.

TerraVest Industries: The Hidden Industrial Compounder

TerraVest Industries exemplifies the type of under-the-radar Canadian compounder that can generate exceptional TFSA returns. This industrial manufacturing company has built a remarkable track record of consistent growth through strategic acquisitions and operational excellence, yet it rarely appears in mainstream investment discussions.

The company operates across multiple industrial segments, including energy equipment manufacturing, agriculture services, and transportation. This diversification provides stability while the management team’s disciplined acquisition strategy creates consistent growth opportunities. TerraVest’s approach focuses on acquiring profitable businesses in niche markets, then improving their operations and expanding their reach.

What makes TerraVest particularly compelling for long-term TFSA investors is management’s commitment to shareholder value creation. The company consistently generates strong free cash flow, which is reinvested into growth opportunities or returned to shareholders through dividends and share repurchases.

| Company | 5-Year Average Return | Dividend Yield | Key Growth Driver |

|---|---|---|---|

| Colliers International | 15.2% | 0.8% | Global services expansion |

| TerraVest Industries | 18.7% | 1.2% | Strategic acquisitions |

| Topicus.com | 22.3% | 0.0% | Vertical market software |

Topicus.com: The European Software Growth Story

Topicus.com represents a unique opportunity for Canadian investors to access high-quality European software growth through the TSX. Spun out from Constellation Software, Topicus follows a similar playbook of acquiring small, profitable vertical market software businesses and helping them grow organically and through further acquisitions.

The company focuses on mission-critical software solutions for specific industries, creating high switching costs and recurring revenue streams. This business model has proven incredibly durable and profitable, as customers rarely change software systems that are integral to their operations. Topicus benefits from both organic growth within existing customer bases and strategic acquisitions of complementary businesses.

For TFSA investors, Topicus offers exposure to the structural growth of software adoption across European markets while benefiting from the proven acquisition and operational expertise developed at Constellation Software. The company’s focus on cash generation and reinvestment creates the perfect recipe for long-term compound growth.

Pro Tip: Software companies like Topicus often experience periods of rapid growth followed by consolidation phases. This volatility can create excellent buying opportunities for patient TFSA investors willing to hold through market cycles.

Smart Portfolio Allocation Strategy for $7,000

The Balanced Growth Allocation Approach

With $7,000 to invest across these three compelling opportunities, strategic allocation becomes crucial for maximizing both growth potential and risk management. Rather than equal-weighting all positions, I recommend a thoughtful allocation that reflects each company’s risk-reward profile and role in your overall wealth-building strategy.

My recommended allocation would be 40% Colliers International ($2,800), 35% TerraVest Industries ($2,450), and 25% Topicus.com ($1,750). This weighting reflects Colliers’ combination of growth potential and relative stability, TerraVest’s proven track record of consistent compounding, and Topicus’s higher-risk, higher-reward software growth profile.

Dollar-Cost Averaging vs. Lump Sum Investment

The question of whether to invest your full $7,000 immediately or spread purchases over several months deserves careful consideration. Academic research generally supports lump-sum investing for long-term wealth building, as markets tend to rise over time, making earlier investment preferable to waiting.

However, given the current market environment and potential volatility, a modified approach might serve TFSA investors well. Consider investing 60% of your allocation immediately to capture current opportunities, then deploying the remaining 40% over the next 2-3 months. This approach balances the benefits of early market participation with some protection against short-term volatility.

Canadian Alert: Remember that TFSA contribution room is precious and limited. Once you withdraw funds from your TFSA, you don’t get that contribution room back until the following year. This makes buy-and-hold strategies particularly attractive for TFSA investing.

Maximizing Compound Growth in Your TFSA

The Power of Reinvesting Dividends

While growth stocks typically pay modest dividends, every dollar received should be immediately reinvested to maximize compound growth within your TFSA. Even small dividend payments, when consistently reinvested, can significantly impact long-term returns through the power of compounding.

Most Canadian brokerages offer dividend reinvestment programs (DRIPs) that automatically purchase additional shares when dividends are paid. This eliminates the temptation to spend dividend income and ensures that every dollar generated by your investments continues working toward your long-term wealth goals.

Avoiding Common TFSA Investment Mistakes

The biggest mistake TFSA investors make is treating the account like a trading platform rather than a long-term wealth-building vehicle. Frequent buying and selling not only generates unnecessary transaction costs but also increases the likelihood of poor timing decisions that can devastate long-term returns.

Another critical error is withdrawing funds for non-essential purchases. While TFSA withdrawals don’t trigger tax consequences, they do cost you precious contribution room that cannot be replaced until the following year. This makes every withdrawal a permanent reduction in your wealth-building capacity.

Finally, many investors make the mistake of holding too much cash within their TFSA while waiting for “perfect” buying opportunities. Time in the market consistently beats timing the market, especially within the tax-sheltered environment of a TFSA where compound growth can work its magic unimpeded.

Frequently Asked Questions

Should I prioritize my TFSA or RRSP for investing?

For most Canadians, maximizing TFSA contributions should take priority over RRSP contributions, especially for younger investors or those in lower tax brackets. The TFSA’s tax-free withdrawals provide superior flexibility, and the tax-free compound growth often outweighs the immediate tax deduction benefits of RRSP contributions. However, high-income earners may benefit from RRSP contributions to reduce current tax burdens.

What happens if my TFSA investments lose money?

Investment losses within your TFSA cannot be claimed as tax losses, and the contribution room is permanently lost. This is why focusing on high-quality, established companies with strong competitive advantages is crucial for TFSA investing. However, temporary market downturns often create excellent buying opportunities for long-term wealth builders.

Can I withdraw money from my TFSA and reinvest it immediately?

While you can withdraw funds from your TFSA at any time without tax consequences, you cannot re-contribute those funds until the following calendar year. This makes withdrawals costly from a wealth-building perspective, as you lose valuable contribution room that could be generating compound returns.

How often should I review my TFSA investments?

Quarterly reviews are sufficient for most TFSA investors focused on long-term wealth building. These reviews should focus on company fundamentals and business performance rather than short-term stock price movements. Annual rebalancing may be appropriate if allocations have shifted significantly due to differential performance.

What’s the biggest mistake TFSA investors make?

The most costly mistake is using TFSA space for guaranteed investment certificates or high-interest savings accounts earning 2-4% annually. This represents a massive opportunity cost when quality growth stocks have historically delivered much higher returns. Your TFSA should house your highest-growth potential investments, not your safest ones.

Should I invest in US stocks within my TFSA?

US stocks held in a TFSA are subject to 15% withholding tax on dividends, which cannot be recovered. This makes dividend-paying US stocks less attractive for TFSA investing. However, US growth stocks with minimal dividends can still be appropriate for TFSA portfolios, especially when currency appreciation provides additional returns for Canadian investors.

Conclusion

Transforming your $7,000 TFSA contribution into long-term wealth requires patience, discipline, and smart stock selection focused on companies with proven ability to compound shareholder value. The three Canadian stocks outlined here—Colliers International, TerraVest Industries, and Topicus.com—represent exactly the type of quality compounders that can turn modest TFSA investments into substantial wealth over time.

Remember that your TFSA represents one of the most powerful wealth-building tools available to Canadian investors. The combination of tax-free growth and flexible withdrawals creates opportunities that simply don’t exist in other account types. By focusing on high-quality growth stocks and maintaining a long-term perspective, your $7,000 investment today could easily become $25,000, $50,000, or even more over the coming decades—all completely tax-free. The key is starting now and letting compound growth work its magic. Don’t let another year pass without maximizing this incredible wealth-building opportunity that’s sitting right at your fingertips.

Want to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- The $5,000 Mistake: Why 71% of Gen Z Is Losing Money to Avoidable Financial Errors – The Evolving Post

- 6 Financial Strategies to Protect Your Wealth

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- 8 Powerful Financial Strategies Every Single Person Should Know

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

- Mortgage Rate Predictions 2025: When Will Rates Drop in US and Canada?

- US Canada Mortgage Rates Comparison 2025: Cross-Border Strategy Guide

Keep exploring — your smartest financial years are just getting started.

Sources:

1. Canada Revenue Agency – TFSA Information

2. Colliers International Investor Relations

3. TerraVest Industries Investor Relations

4. Topicus.com Investor Relations

5. Bank of Canada – Consumer Price Index

6. TSX Market Statistics and Performance Data