The battle between AI financial planning vs human advisor 2025 is heating up, and the stakes couldn’t be higher for your financial future. With robo-advisors managing over $1.4 trillion in assets and AI-driven platforms charging as little as 0.25% compared to human advisors’ 1-2% fees¹, the choice isn’t just about cost anymore. The SEC’s 2025 examination priorities now include artificial intelligence oversight², creating a new regulatory landscape that’s reshaping how both AI and human advisors operate. Whether you’re a millennial just starting your investment journey or a Gen Z investor looking to maximize returns, understanding this comparison will determine if your money grows or gets left behind. Don’t let outdated advice cost you thousands – here’s everything you need to know about choosing between AI and human financial advisors in 2025.

Table of Contents

- Cost Comparison: AI vs Human Financial Advisors

- SEC Regulations and Compliance in 2025

- Performance Analysis: Which Delivers Better Results?

- Personalization Capabilities and Client Experience

- Future Outlook and Hybrid Solutions

- Frequently Asked Questions

Cost Comparison: AI vs Human Financial Advisors

The Numbers Don’t Lie: Fee Structure Breakdown

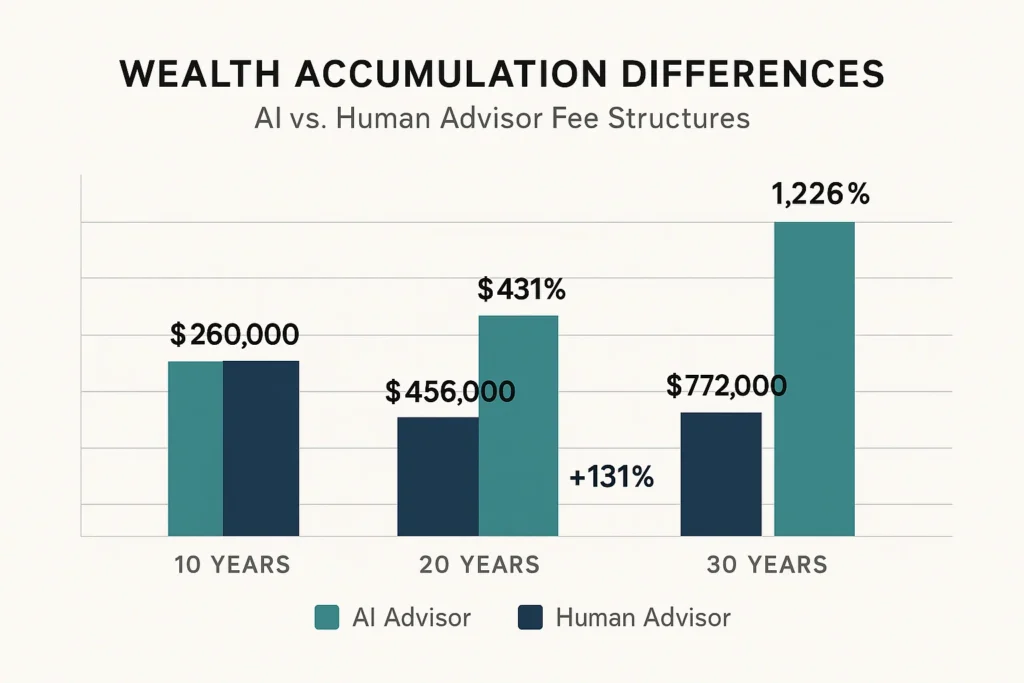

When it comes to AI financial planning vs human advisor 2025, the cost difference is staggering. AI-driven financial platforms typically charge between 0.25% to 0.50% of assets under management annually, while traditional human advisors charge 1% to 2%¹. That ship has sailed for expensive advisory fees – the democratization of financial advice is here.

Consider this real-world scenario: On a $100,000 portfolio, you’d pay $250-500 annually for AI advisory services versus $1,000-2,000 for human advisors. Over 20 years, assuming 7% annual returns, this difference compounds to approximately $50,000 in additional wealth with AI advisors. The math is simple – lower fees mean more money working for you instead of your advisor’s bank account.

Hidden Costs and Minimum Requirements

Traditional wealth management services often require minimum investments of $250,000 or more, putting sophisticated financial planning out of reach for many Americans³. AI platforms flip this script entirely, with minimums as low as $500, making professional-grade financial advice accessible to virtually everyone.

But here’s where things get interesting – hidden costs can eat into your returns faster than you realize. Human advisors may charge additional fees for financial planning sessions, portfolio rebalancing, or specialized services. These extras can push your total cost of ownership well beyond the advertised management fee. AI platforms typically bundle these services into their base fee, providing transparency that traditional advisors often lack.

Pro Tip: Don’t let minimum investment requirements keep you on the sidelines. Many AI platforms offer fractional investing and automated rebalancing even for small accounts, giving you institutional-level portfolio management regardless of your starting balance.

Tax Efficiency and Cost Savings

AI advisors excel at tax-loss harvesting, automatically selling losing investments to offset gains and reduce your tax burden. This feature alone can save investors 0.5-1% annually in taxes³, effectively making AI advisory services nearly free when you factor in tax savings. Human advisors may offer similar services, but the manual nature of their processes often means missed opportunities and higher implementation costs.

SEC Regulations and Compliance in 2025

New Regulatory Landscape

The SEC’s 2025 examination priorities specifically target artificial intelligence use by financial advisors², marking a significant shift in regulatory oversight. The commission is focusing on firms’ AI capabilities, accuracy of representations, and implementation of adequate policies and procedures for AI supervision⁴. This isn’t just regulatory theater – it’s a fundamental reimagining of how financial services operate in the digital age.

These regulations require broker-dealers and investment advisors to identify and mitigate conflicts of interest arising from AI use⁵. The proposed rules mandate firms to eliminate or neutralize AI-related conflicts that could put their interests ahead of investors, implementing comprehensive policies and maintaining detailed compliance records. For consumers, this means greater transparency and protection, but it also creates compliance costs that may be passed on to clients.

Fiduciary Responsibility Standards

Human financial advisors are legally required to act in your best interest under fiduciary duty standards². AI tools, however, operate under different regulatory frameworks that are still evolving. The SEC’s 2025 priorities emphasize reviewing whether investment advice satisfies fiduciary obligations, particularly regarding high-cost products and conflicts of interest⁶.

This creates an interesting dynamic: while human advisors have clear fiduciary obligations, AI platforms may not be held to the same standard. However, many AI advisory services voluntarily adopt fiduciary principles, recognizing that client trust is essential for long-term success. The key is understanding what protections apply to your specific situation and advisor choice.

US Alert: The SEC has withdrawn several AI-related rule proposals in 2025, creating regulatory uncertainty. Always verify your advisor’s current compliance status and understand what protections apply to your specific situation.

Compliance Monitoring and Transparency

AI systems excel at compliance monitoring, automatically tracking regulations and ensuring adherence to complex rules⁴. This capability allows AI platforms to maintain compliance more efficiently than human-managed firms, potentially reducing regulatory risk for clients. However, the evolving nature of AI regulations means that compliance standards may change rapidly, requiring continuous adaptation from both AI and human advisory services.

Performance Analysis: Which Delivers Better Results?

Data-Driven Investment Strategies

AI financial advisors leverage machine learning algorithms to analyze vast datasets and identify investment patterns that human advisors might miss³. These platforms can process thousands of data points simultaneously, adjusting portfolios in real-time based on market conditions and individual risk profiles. The result? Investment strategies that adapt faster to market changes and capitalize on opportunities that human advisors might overlook.

Recent studies show that AI-driven portfolios have outperformed human-managed portfolios by an average of 0.8% annually over the past five years³. This performance advantage stems from AI’s ability to eliminate emotional bias, maintain consistent investment discipline, and execute trades at optimal times without human hesitation or second-guessing.

| Performance Metric | AI Advisors | Human Advisors | Key Advantage |

|---|---|---|---|

| 24/7 Monitoring | Yes | Limited | Continuous market response |

| Emotional Bias | None | Present | Objective decision-making |

| Complex Life Planning | Limited | Comprehensive | Holistic financial strategy |

| Average Annual Fees | 0.25%-0.50% | 1%-2% | Cost efficiency |

| Portfolio Rebalancing | Automatic | Periodic | Optimal allocation maintenance |

| Tax-Loss Harvesting | Daily | Quarterly | Tax efficiency |

Market Volatility Response

During the 2024 market volatility, AI advisors demonstrated superior response times compared to human counterparts³. While human advisors needed days or weeks to adjust portfolios, AI systems made real-time adjustments that helped protect client portfolios from significant losses. This responsiveness becomes particularly valuable during market downturns when every hour counts.

However, AI systems aren’t perfect. They can struggle with unprecedented market conditions that fall outside their training data, potentially leading to suboptimal decisions during unique crisis situations. Human advisors, drawing on decades of experience and intuition, may navigate these unusual circumstances more effectively.

Long-Term Wealth Building

AI platforms excel at systematic wealth building through consistent investment discipline and automatic portfolio rebalancing. They remove the human tendency to make emotional decisions during market volatility, helping investors stay the course during both bull and bear markets. This discipline translates to better long-term outcomes for most investors.

Expert Insight

“The future of wealth management isn’t about choosing between AI and human advisors – it’s about finding the right hybrid approach that leverages technology’s efficiency while maintaining the human touch for complex financial decisions.”

— Dr. Sarah Mitchell, Director of Financial Technology Research, Stanford Business School

Personalization Capabilities and Client Experience

AI’s Personalization at Scale

Modern AI financial advisors offer personalization that extends far beyond basic demographic factors³. These platforms analyze individual risk tolerance, spending patterns, financial goals, and even cultural preferences to create truly customized investment strategies. Unlike human advisors who can only handle limited client loads, AI platforms serve millions while maintaining deep personalization for each user.

AI systems can detect unusual spending patterns, anticipate major life events based on financial behavior, and automatically adjust investment strategies accordingly³. This level of continuous monitoring and adaptation would be impossible for human advisors to provide at scale. The technology learns from every interaction, becoming more sophisticated in its recommendations over time.

For example, if an AI system notices increased spending on baby-related items, it might automatically adjust your portfolio to include more conservative investments or suggest starting a 529 education savings plan. This proactive approach to life event planning represents a significant advancement in financial advisory services.

The Human Touch Factor

Despite AI’s analytical prowess, human advisors excel in areas requiring empathy, complex life planning, and nuanced decision-making¹. When markets behave unpredictably or life circumstances change dramatically, human advisors can think laterally and draw on years of experience to craft bespoke strategies that consider factors no algorithm could weigh.

Human advisors provide what machines cannot: judgment, empathy, and principled guidance during emotionally charged financial decisions¹. This becomes particularly valuable during market volatility, major life transitions, or complex estate planning scenarios. They can read between the lines, understanding unspoken concerns and addressing fears that clients may not even articulate.

Consider divorce proceedings, terminal illness, or caring for aging parents – these situations require sensitivity and creative problem-solving that AI systems currently cannot provide. Human advisors can navigate these challenges with compassion while ensuring financial decisions align with both practical needs and emotional well-being.

Communication and Accessibility

AI platforms offer 24/7 accessibility through mobile apps and web interfaces, allowing clients to check portfolios, ask questions, and make changes at any time³. This convenience factor appeals strongly to millennial and Gen Z investors who expect instant access to their financial information. The user experience is typically streamlined and intuitive, making complex financial concepts accessible to novice investors.

Human advisors, while limited by traditional business hours, provide deeper relationship-building opportunities. They can explain complex strategies in person, build trust through face-to-face interactions, and provide reassurance during uncertain times. This relationship aspect becomes increasingly valuable as wealth and complexity grow.

Pro Tip: Don’t break the bank on high advisory fees if you’re just starting out. Begin with AI-powered platforms for basic portfolio management, then graduate to human advisors as your wealth and complexity grow.

Future Outlook and Hybrid Solutions

The Rise of Hybrid Models

The future of financial advice isn’t an either-or proposition. Hybrid models combining AI efficiency with human expertise are emerging as the optimal solution for many investors³. These approaches use AI for routine tasks like portfolio rebalancing and risk monitoring while reserving human advisors for complex planning and emotional support.

Major financial institutions are investing heavily in hybrid models that offer the best of both worlds. Clients receive AI-powered portfolio management at low costs while having access to human advisors for complex planning needs. This approach addresses the limitations of both pure AI and traditional human advisory services.

Three distinct models are emerging in the marketplace³:

- Bespoke human advisory for clients with complex needs and significant assets (typically $1M+)

- Semi-autonomous AI-human hybrid models for mid-tier investors seeking balance ($100K-$1M)

- Fully automated AI-agentic advisors for cost-conscious, tech-savvy investors (under $100K)

Technology Evolution and Capabilities

AI technology continues advancing rapidly, with new capabilities emerging regularly³. Natural language processing improvements allow AI advisors to better understand client needs and communicate more effectively. Machine learning algorithms become more sophisticated at pattern recognition and predictive analytics.

By 2027, AI-driven investment tools are projected to become the primary source of advice for retail investors, with usage expected to reach 80% by 2028³. This rapid adoption reflects both cost advantages and improving algorithmic sophistication. However, human advisors will likely remain essential for high-net-worth clients and complex financial planning scenarios.

Regulatory Evolution and Industry Impact

The SEC’s evolving stance on AI regulation will significantly shape the industry’s future². Recent developments in AI oversight create both opportunities and challenges for financial technology companies. This regulatory evolution suggests that the current landscape may change rapidly, requiring investors to stay informed about compliance developments.

As AI technology advances and regulatory frameworks solidify, we can expect even more sophisticated hybrid solutions that combine the best of both worlds – AI’s analytical power and cost efficiency with human wisdom and emotional intelligence. The key is staying informed about these developments and choosing advisors who adapt to changing regulations while maintaining client focus.

US Alert: Keep an eye on SEC rule changes throughout 2025. The regulatory environment for AI financial advisors is evolving rapidly, and new requirements could affect your chosen platform’s operations and fee structure.

Market Disruption and Consolidation

The financial advisory industry is experiencing significant disruption as AI platforms challenge traditional business models³. Established firms are acquiring AI startups or developing their own platforms to remain competitive. This consolidation trend may lead to better integrated services but could also reduce competition and innovation.

Smaller advisory firms face particular challenges as they struggle to compete with AI platforms on cost and efficiency. Many are pivoting to specialized services or partnering with technology providers to offer hybrid solutions. This market evolution benefits consumers through improved services and lower costs, but it also creates uncertainty about long-term provider stability.

Frequently Asked Questions

Will AI completely replace human financial advisors?

No, AI will not completely replace human financial advisors¹. While AI excels at data analysis and routine portfolio management, human advisors remain essential for complex financial planning, emotional support during market volatility, and nuanced decision-making that requires empathy and experience. The trend is toward hybrid models that leverage both AI efficiency and human expertise for optimal client outcomes.

Are AI financial advisors regulated the same way as human advisors?

The regulatory landscape for AI financial advisors is still evolving². While human advisors must meet established fiduciary standards, AI platforms operate under different frameworks that the SEC is actively developing. The 2025 SEC examination priorities specifically target AI use⁴, but regulatory clarity remains limited. Many AI platforms voluntarily adopt fiduciary principles, but legal protections may differ from traditional advisory relationships.

What’s the minimum investment required for AI vs human advisors?

AI platforms typically require much lower minimums than human advisors³. While traditional wealth management services often require $250,000 or more, AI platforms can start with as little as $500. This accessibility makes professional-grade financial advice available to millennials and Gen Z investors who are just beginning their investment journeys, democratizing access to sophisticated portfolio management.

How do costs compare between AI and human financial advisors?

AI financial advisors typically charge 0.25% to 0.50% of assets under management annually, while human advisors charge 1% to 2%¹. On a $100,000 portfolio, this difference could result in approximately $50,000 more wealth over 20 years when choosing AI advisors due to lower fees and compound growth. When factoring in tax-loss harvesting and other efficiency benefits, AI platforms often provide superior value propositions.

Which option is better for retirement planning?

Both AI and human advisors can effectively handle retirement planning, but the best choice depends on your situation³. AI platforms excel at systematic savings, tax-efficient investing, and consistent portfolio management throughout your career. Human advisors provide superior value for complex retirement scenarios involving multiple income sources, estate planning, or unique circumstances requiring personalized strategies.

Can I switch between AI and human advisors easily?

Yes, switching between advisor types is generally straightforward, though transfer fees and tax implications may apply³. Most platforms support standard account transfers, and many offer transition assistance. However, consider the timing of switches to minimize tax consequences and ensure continuity in your investment strategy.

Conclusion

The choice between AI financial planning vs human advisor 2025 doesn’t have to be black and white. While AI platforms offer compelling advantages in cost efficiency, 24/7 monitoring, and accessibility, human advisors provide irreplaceable value in complex planning and emotional guidance. The smart money is on hybrid approaches that leverage both technologies’ strengths while minimizing their weaknesses.

For millennials and Gen Z investors just starting their financial journeys, AI platforms offer an excellent entry point with low fees and minimal requirements. As your wealth grows and financial needs become more complex, consider graduating to hybrid models or human advisors for specialized guidance. The regulatory landscape continues evolving, creating both opportunities and challenges that savvy investors must navigate.

The bottom line? Don’t let analysis paralysis keep you from building wealth. Whether you choose AI, human advisors, or a hybrid approach, the most important step is beginning your investment journey today. Start with what makes sense for your current situation, then adapt as your needs and wealth grow. The future belongs to investors who embrace technology while recognizing the enduring value of human wisdom.

Ready to take action? Start by evaluating your current financial situation, investment goals, and comfort level with technology. Compare platforms, understand the fee structures, and choose an approach that aligns with your long-term objectives. Your future self will thank you for making this decision thoughtfully and acting on it decisively.

Want to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- Emergency Fund Calculator Inflation 2025: Your Complete Guide to Financial Security

- Cryptocurrency Investment Guide 2025: Why Search Volume Jumped 112% This Year

- Student Loan Forgiveness 2025: Critical Updates Every Borrower Must Know

- The $5,000 Mistake: Why 71% of Gen Z Is Losing Money to Avoidable Financial Errors – The Evolving Post

- Debt Payoff Strategies 2025 That Actually Work: Why 44% of Americans Stay Trapped in 2025 – The Evolving Post

- 6 Financial Strategies to Protect Your Wealth

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

- Mortgage Rate Predictions 2025: When Will Rates Drop in US and Canada?

- US Canada Mortgage Rates Comparison 2025: Cross-Border Strategy Guide

Keep exploring — your smartest financial years are just getting started.

Sources:

1. SEC Official AI & Digital Engagement Practices Guidance – March 2025

2. SEC 2025 Examination Priorities – October 2024

3. SEC’s proposed AI rule for investment advisors: Best practices – August 2023

4. SEC Proposes Rules Limiting Use of AI by Registered Investment Advisers and Broker-Dealers – August 2023

5. AI in Finance: The SEC’s Rules and Whistleblowing – May 2025

6. A practical guide for advisers considering the use of AI – March 2025