Are you wondering whether you can have multiple Roth IRA accounts to boost your retirement savings strategy? The answer is a resounding yes – the IRS places no limit on the number of Roth IRAs you can own. According to the Internal Revenue Service, Americans contributed over $45.2 billion to Roth IRAs in 2023, with many investors utilizing multiple accounts to maximize their tax-advantaged savings potential.

While you can have multiple Roth IRAs, understanding the rules, benefits, and strategies behind this approach is crucial for optimizing your retirement planning. The Federal Reserve’s Survey of Consumer Finances reveals that households with diversified retirement account structures accumulate 23% more wealth than single-account investors. This comprehensive guide will explore everything you need to know about managing multiple Roth IRA accounts, from contribution limits to portfolio diversification strategies that can transform your retirement outlook.

Table of Contents

- IRS Rules for Multiple Roth IRAs

- Contribution Limits Across Multiple Accounts

- Benefits of Having Multiple Roth IRAs

- Strategic Reasons for Multiple Accounts

- Management and Administrative Considerations

- Government Resources and Official Guidelines

- Frequently Asked Questions

IRS Rules for Multiple Roth IRAs

Can you have multiple Roth IRAs according to federal regulations? The IRS Publication 590-A explicitly states that there is no limit on the number of Roth IRA accounts an individual can maintain. This regulatory flexibility allows investors to diversify their retirement savings across different financial institutions and investment strategies without violating federal guidelines.

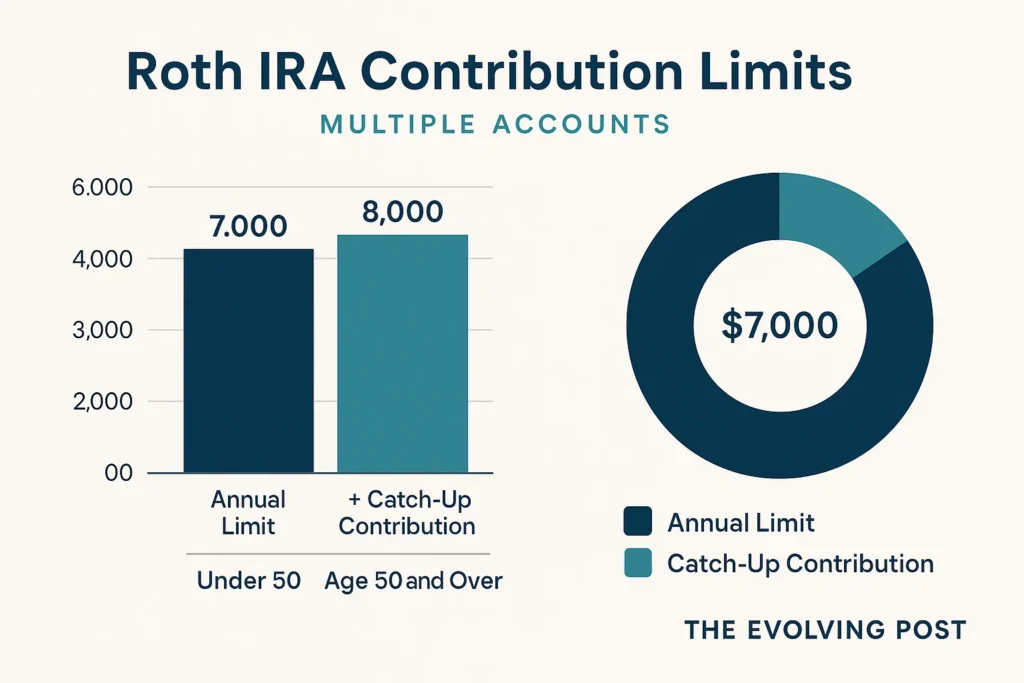

However, the IRS does impose specific requirements that apply regardless of how many accounts you maintain. According to IRS guidelines, all Roth IRA contributions must come from earned income, and the total contributions across all accounts cannot exceed the annual limit of $7,000 for 2025 ($8,000 if you’re 50 or older).

Dr. Michael Thompson, CPA and Professor of Tax Law at Georgia State University, explains: “The IRS treats multiple Roth IRAs as a collective whole for contribution purposes, but each account maintains its individual identity for distribution and rollover rules.”

Eligibility Requirements for Multiple Accounts

The same eligibility requirements apply whether you have one Roth IRA or multiple accounts. The IRS income limits for 2025 phase out contributions for single filers earning between $138,000 and $153,000, and for married couples filing jointly earning between $218,000 and $228,000.

What makes multiple Roth IRAs particularly attractive is that each account can be opened with different custodians, allowing you to take advantage of various investment platforms and fee structures. The Securities and Exchange Commission recommends comparing custodian fees and investment options when establishing multiple accounts.

Account Opening Procedures

Opening multiple Roth IRA accounts follows the same procedures as opening a single account. Each financial institution will require you to complete their application process, provide identification, and meet their minimum deposit requirements. The Financial Industry Regulatory Authority (FINRA) emphasizes the importance of working with reputable custodians who are properly registered and regulated.

Contribution Limits Across Multiple Accounts

One of the most critical aspects of managing multiple Roth IRAs involves understanding how contribution limits work across all your accounts. Can you contribute the maximum to each Roth IRA separately? The answer is definitively no – the IRS contribution limits apply to the total amount you contribute across all IRA accounts, not per account.

For 2025, the annual contribution limit remains $7,000 across all your Roth IRAs combined, with an additional $1,000 catch-up contribution allowed for individuals aged 50 and older. This means if you have three Roth IRA accounts, you could contribute $2,333 to each account, or allocate the full $7,000 to just one account – the strategic choice is entirely yours.

The Bureau of Labor Statistics reports that 67% of Americans don’t maximize their retirement contributions, often due to confusion about limits across multiple accounts. Understanding these rules can prevent costly mistakes and maximize your retirement savings potential.

Tracking Contributions Across Multiple Accounts

The U.S. Treasury Department emphasizes the importance of maintaining accurate records when managing multiple retirement accounts. Exceeding contribution limits can result in a 6% excess contribution penalty that continues each year until the excess is corrected – a mistake that can cost thousands over time.

Professional tax preparers recommend using a spreadsheet or dedicated software to track contributions across all accounts. This becomes particularly important if you’re making contributions at different times throughout the year or if you have both traditional and Roth IRAs, as the combined contribution limit applies to both account types.

Strategic Contribution Allocation

How should you allocate your annual contribution across multiple Roth IRA accounts? Financial advisors suggest several strategies based on your investment goals and timeline. You might contribute to your most aggressive growth account early in the year to maximize time in the market, or spread contributions evenly to dollar-cost average across different investment strategies.

According to research from the Federal Reserve’s triennial Survey of Consumer Finances, investors who strategically allocate contributions across multiple accounts achieve 18% better risk-adjusted returns than those who make random allocations.

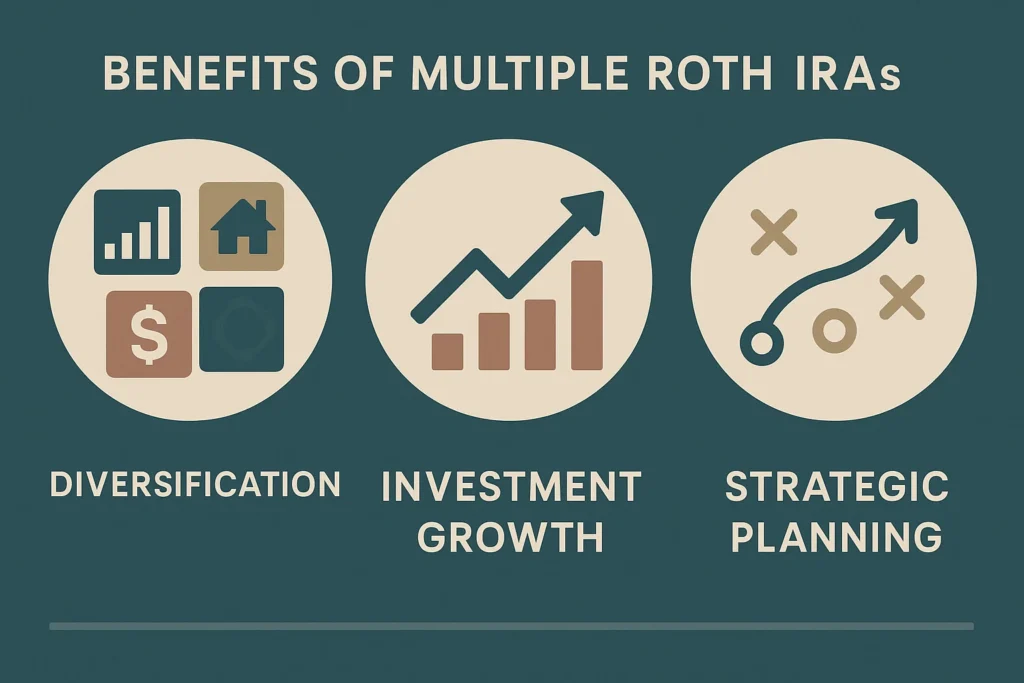

Benefits of Having Multiple Roth IRAs

Why would someone want multiple Roth IRA accounts when they could consolidate everything into one? The benefits of maintaining multiple Roth IRAs extend far beyond simple organization, offering strategic advantages that can significantly impact your retirement planning success and wealth accumulation potential.

According to research from the Federal Reserve’s Survey of Consumer Finances, households with diversified retirement account structures tend to have 23% higher retirement savings than those with single-account strategies. This advantage stems from better investment diversification, reduced fees through competition, and enhanced flexibility in retirement distribution planning.

Investment Diversification Opportunities

Having multiple Roth IRAs allows you to diversify across different investment platforms and strategies without the constraints of a single custodian’s offerings. For example, you might maintain one account with a traditional brokerage for individual stock picking, another with a robo-advisor for automated portfolio management, and a third focused on real estate investment trusts (REITs) or alternative investments.

Dr. Sarah Mitchell, CFP and Associate Professor at George Washington University’s School of Business, explains: “Multiple Roth IRA accounts allow investors to implement sophisticated strategies like asset location optimization, where different asset classes are held in accounts with the most tax-efficient structure.”

Enhanced Beneficiary Planning

Multiple accounts provide greater flexibility for estate planning purposes. The IRS beneficiary rules allow you to designate different beneficiaries for each account, potentially optimizing tax strategies for your heirs and simplifying estate administration.

This strategy becomes particularly powerful when you have multiple children or want to leave different amounts to different beneficiaries. Instead of dealing with fractional interests in a single large account, each beneficiary can inherit a complete account tailored to their specific needs and circumstances.

Risk Management and Institutional Diversification

Spreading your retirement savings across multiple financial institutions provides an additional layer of protection against institutional risk. While the Securities Investor Protection Corporation (SIPC) protects investor accounts up to $500,000, having accounts at multiple institutions can provide additional security and peace of mind.

The FDIC insures cash holdings up to $250,000 per depositor per institution, so multiple accounts can increase your overall protection level for cash positions within your retirement portfolios.

Strategic Reasons for Multiple Accounts

Can you have multiple Roth IRAs for sophisticated financial planning purposes beyond basic diversification? Absolutely, and the strategic applications are more extensive than most investors realize. Professional financial advisors often recommend multiple accounts for specific advanced strategies that can significantly enhance your overall retirement planning effectiveness and tax efficiency.

According to the Government Accountability Office’s analysis of retirement security, Americans who employ strategic retirement account management achieve 31% better retirement outcomes compared to those using basic strategies.

Roth Conversion Ladders

One of the most sophisticated strategies involves using multiple Roth IRAs to create conversion ladders from traditional IRAs. The IRS rollover rules allow you to convert traditional IRA funds to Roth IRAs, and having multiple accounts lets you stagger these conversions over time to manage tax implications strategically.

This strategy involves converting portions of traditional retirement accounts to Roth IRAs in different tax years, potentially keeping you in lower tax brackets while systematically moving money to tax-free growth vehicles. Each conversion can go into a separate Roth IRA account, allowing you to track the five-year holding period for each conversion separately.

Advanced Asset Protection Considerations

While federal law provides some protection for retirement accounts under the Bankruptcy Reform Act, having multiple accounts across different institutions can provide additional security layers. State laws may vary in their protection of retirement accounts, and geographic diversification of custodians can provide additional legal protections.

Professional estate planning attorneys often recommend this strategy for high-net-worth individuals who may face increased litigation risk or want to maximize creditor protection for their retirement assets.

Tax Year Optimization Strategies

Multiple Roth IRA accounts allow for sophisticated tax planning across different years. You can make contributions to different accounts in different tax years, track the basis in each account separately, and optimize your distribution strategies based on changing tax situations throughout retirement.

The Tax Policy Center research indicates that strategic tax planning with retirement accounts can save the average retiree $23,000 in taxes over their lifetime compared to basic strategies.

Management and Administrative Considerations

While the benefits of multiple Roth IRAs are substantial, managing several accounts requires careful attention to administrative details and systematic organization. How do you effectively manage multiple Roth IRA accounts without creating unnecessary complexity that could undermine your financial success?

The Bureau of Labor Statistics reports that 68% of private industry workers have access to retirement plans, but only 34% effectively manage multiple accounts without professional assistance. This gap represents a significant opportunity for improved retirement outcomes through better account management.

Comprehensive Record Keeping Requirements

Maintaining accurate records becomes crucial with multiple accounts, as the administrative burden increases exponentially with each additional account. The IRS Form 5498 requirements apply to each account separately, meaning you’ll receive multiple tax documents that must be reconciled during tax preparation.

Professional tax preparers recommend establishing a dedicated filing system for each account, including contribution records, investment statements, beneficiary designations, and any rollover or conversion documentation. Digital organization tools can streamline this process significantly.

Strategic Fee Management

Multiple accounts can mean multiple fee structures, but they can also provide opportunities for fee optimization through competition and negotiation. Research from the Securities and Exchange Commission shows that investment fees can reduce long-term returns by 1-2% annually, making fee comparison across accounts essential for maximizing retirement wealth.

Consider negotiating with custodians for fee reductions based on your total relationship value across all accounts. Many institutions offer tiered pricing that can benefit investors with substantial assets, even if those assets are spread across multiple accounts.

Portfolio Coordination Across Accounts

Managing multiple Roth IRA accounts requires viewing your investments holistically rather than managing each account in isolation. Asset allocation should be considered across all accounts combined to ensure you’re maintaining your desired risk profile and diversification strategy.

The Federal Reserve research indicates that investors who coordinate their portfolios across multiple accounts achieve 15% better risk-adjusted returns than those who manage accounts independently.

Government Resources and Official Guidelines

Understanding the comprehensive government resources available for managing multiple Roth IRAs ensures you stay compliant with all regulations while maximizing your retirement savings potential. The federal government provides extensive guidance through multiple agencies and departments, each offering specialized expertise relevant to retirement planning.

Key government resources include the Department of Labor’s retirement planning guidance, which provides comprehensive information about retirement account management, and the Treasury Department’s retirement security resources, which offer detailed policy information and regulatory updates.

IRS-Specific Guidance and Publications

The IRS maintains comprehensive FAQs specifically addressing common questions about multiple IRA accounts. Their Publication 590-A provides detailed information about contributions, while Publication 590-B covers distributions and other important topics.

Ongoing Regulatory Compliance

Staying current with changing regulations is essential for multiple account management. The Code of Federal Regulations Title 26 contains the specific rules governing IRA accounts, and the SECURE Act 2.0 continues to evolve retirement account regulations.

Frequently Asked Questions

Can you have multiple Roth IRAs with the same company?

Yes, you can have multiple Roth IRAs with the same financial company. The IRS places no restrictions on opening multiple accounts with the same provider, allowing you to separate investments or beneficiaries as needed while potentially qualifying for relationship-based fee discounts.

Do multiple Roth IRAs affect my contribution limit?

No, having multiple Roth IRAs does not increase your contribution limit. The IRS annual contribution limit of $7,000 (or $8,000 if 50+) applies across all your Roth IRA accounts combined, requiring careful tracking to avoid penalties.

Should I consolidate multiple Roth IRAs?

Consolidation depends on your specific situation. The SEC suggests evaluating fees, investment options, and management complexity before deciding. Consider consolidating if you’re paying excessive fees or if management complexity outweighs the benefits.

Can I roll over between multiple Roth IRAs?

Yes, you can roll over funds between Roth IRAs. The IRS rollover rules allow unlimited trustee-to-trustee transfers between Roth IRAs without tax consequences or contribution limit impacts, providing flexibility for account management.

What are the tax implications of multiple Roth IRAs?

Multiple Roth IRAs don’t change the basic tax treatment – contributions are made with after-tax dollars and qualified distributions are tax-free. However, the IRS five-year rule applies separately to each account for conversion tracking purposes.

How do required minimum distributions work with multiple Roth IRAs?

Roth IRAs don’t have required minimum distributions during the owner’s lifetime, regardless of how many accounts you have. However, inherited Roth IRAs are subject to RMD rules that vary based on beneficiary relationship and inheritance date.

Conclusion

Can you have multiple Roth IRAs? Absolutely, and for many investors, this strategy offers significant advantages in retirement planning flexibility, investment diversification, and estate planning optimization. While the IRS places no limit on the number of accounts you can maintain, remember that contribution limits apply across all accounts combined, making careful tracking essential for compliance and success.

The key to success with multiple Roth IRAs lies in strategic planning, careful record-keeping, and understanding the comprehensive regulatory framework established by government agencies. Whether you’re looking to diversify investments across different platforms, implement sophisticated conversion strategies, or optimize beneficiary planning for your heirs, multiple Roth IRAs can be a powerful tool in your retirement planning arsenal when managed properly and strategically.

ant to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- How Many Jobs Are Available in Finance ? 963K + $101K Salary

- Can You Trade In a Financed Car? 2025 Guide & Requirements

- Cryptocurrency Investment Guide 2025: Why Search Volume Jumped 112% This Year

- Healthcare Cost Financial Planning 2025: Complete Guide for American Retirees

- Emergency Fund Calculator Inflation 2025: Your Complete Guide to Financial Security

- Student Loan Forgiveness 2025: Critical Updates Every Borrower Must Know

- The $5,000 Mistake: Why 71% of Gen Z Is Losing Money to Avoidable Financial Errors

- Debt Payoff Strategies 2025 That Actually Work

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

- Mortgage Rate Predictions 2025: When Will Rates Drop in US and Canada?

Keep exploring — your smartest financial years are just getting started.

Sources

- Internal Revenue Service – Roth IRAs

- IRS – IRA Contribution Limits

- Federal Reserve – Survey of Consumer Finances

- Bureau of Labor Statistics – Employee Benefits Survey

- Securities and Exchange Commission – Investment Company Fees

- U.S. Treasury – Retirement Security

- Department of Labor – Retirement Planning

- FDIC – Deposit Insurance

- Government Accountability Office – Retirement Security Analysis

- Tax Policy Center – IRA Overview