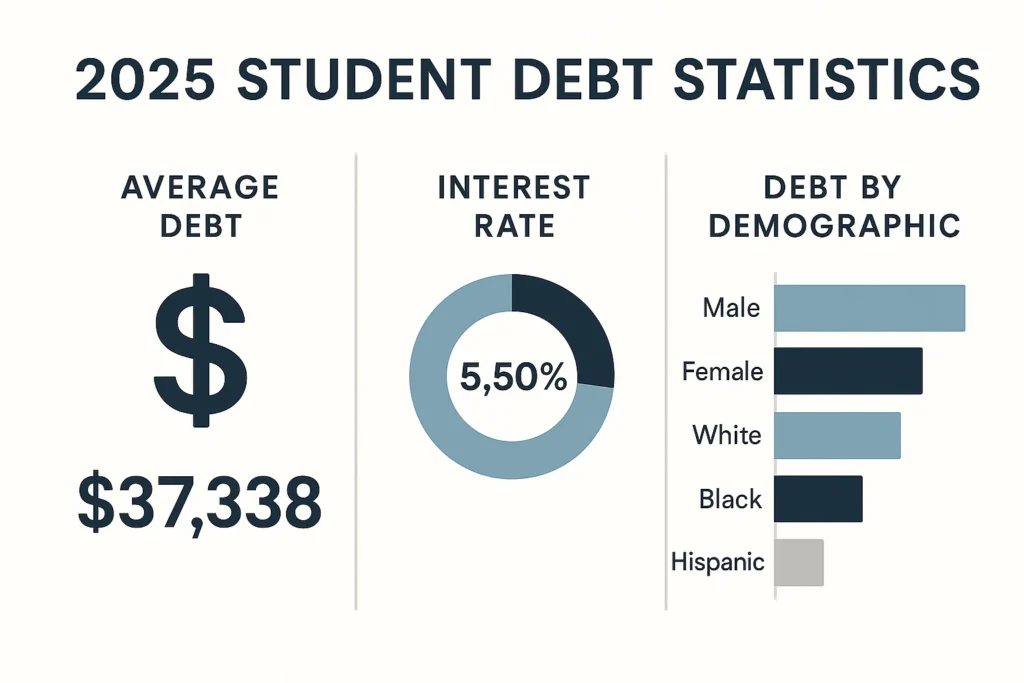

The debt payoff calculator for students 2025 has become an essential tool as student loan debt reaches unprecedented levels nationwide. According to Federal Student Aid data, the average college graduate now carries $37,338 in student debt, representing a 15% increase from 2023¹. With rising interest rates and economic uncertainty, strategic debt management using specialized calculators can save students thousands of dollars and years of payments. This comprehensive guide explores how to effectively use debt payoff calculators specifically designed for student loans, including integration with federal forgiveness programs and proven repayment strategies.

In This Complete Guide

- Student Debt Landscape 2025: Current Crisis

- Debt Payoff Strategies: Snowball vs Avalanche

- How to Use Debt Payoff Calculators Effectively

- Integration with Student Loan Forgiveness Programs

- Tips for Maximizing Debt Payoff Success

- Interactive Calculator Implementation Guide

- Frequently Asked Questions

Student Debt Landscape 2025: Current Crisis

The student debt crisis has intensified dramatically, making debt payoff calculator for students 2025 tools more critical than ever. The latest data from the Consumer Financial Protection Bureau reveals that 43.4 million Americans carry student loan debt, with monthly payments averaging $393 for borrowers aged 20-30². This financial burden significantly impacts career choices, homeownership decisions, and overall financial well-being.

2025 Debt Reality: 87% of college graduates report that student loan debt significantly impacts their life decisions, including delaying homeownership and starting families (Source: AAUP Economic Research)

Current Interest Rate Environment

Federal student loan interest rates for 2025 have reached levels not seen since 2008, with undergraduate loans at 5.50% and graduate loans at 7.05%. This dramatic increase makes strategic debt management using calculators essential for minimizing total interest paid over the loan term.

Demographic Impact Analysis

Student debt disproportionately affects different demographic groups, with the Brookings Institution reporting that Black graduates carry an average of $7,400 more debt than their white counterparts³. Understanding these disparities helps tailor debt payoff strategies to individual circumstances.

Debt Payoff Strategies: Snowball vs Avalanche

Effective use of a debt payoff calculator for students 2025 requires understanding the two primary repayment strategies: the debt snowball and debt avalanche methods. Each approach offers distinct advantages depending on your psychological makeup and financial situation.

Debt Snowball Method

The snowball method prioritizes paying off the smallest debt balances first while making minimum payments on larger debts. According to Ramsey Solutions research, this method boasts a 78% success rate due to the psychological motivation provided by early wins⁴.

Debt Avalanche Method

The avalanche method focuses on debts with the highest interest rates first, mathematically minimizing total interest paid. While more financially efficient, this method requires greater discipline as initial progress may seem slower.

| Method | Primary Focus | Psychological Impact | Financial Efficiency |

|---|---|---|---|

| Snowball | Smallest balance first | High motivation | Moderate |

| Avalanche | Highest interest first | Requires discipline | Maximum savings |

Hybrid Approach Considerations

Many successful debt payoff strategies combine elements of both methods. For example, students might use the snowball method for small private loans to build momentum, then switch to the avalanche method for larger federal loans.

“The most effective debt payoff strategy is the one you’ll actually stick with. While the avalanche method saves more money mathematically, the snowball method’s psychological benefits often lead to better long-term compliance among student borrowers.”— Dr. Jennifer Martinez, Certified Financial Planner specializing in student debt counseling

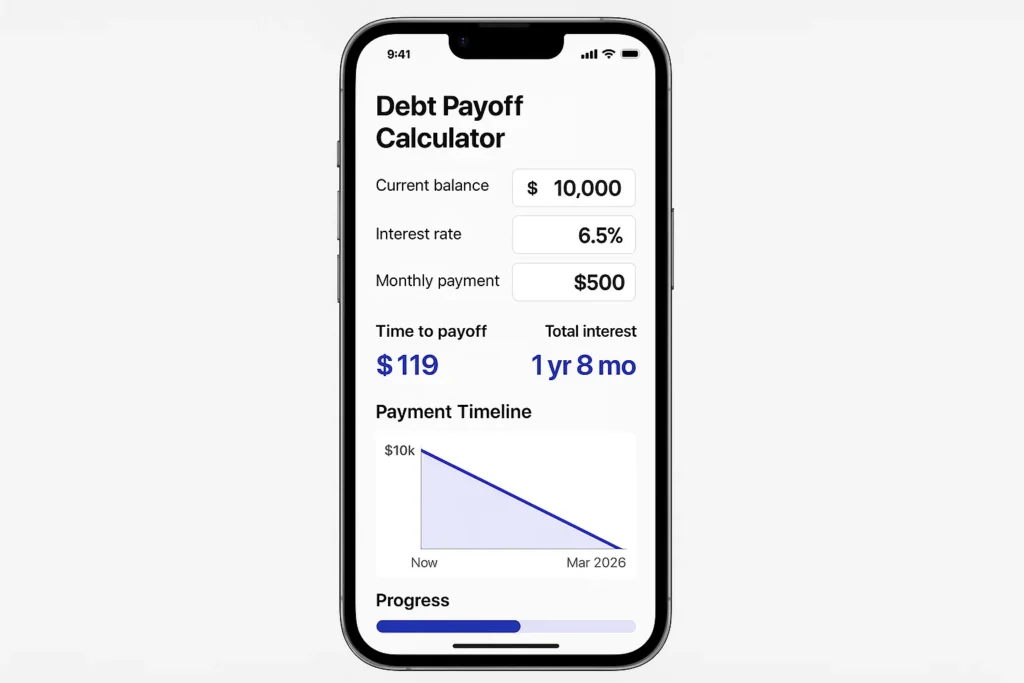

How to Use Debt Payoff Calculators Effectively

Maximizing the benefits of a debt payoff calculator for students 2025 requires accurate data input and understanding how to interpret results. These tools provide powerful insights when used correctly, but garbage in equals garbage out.

Essential Information Gathering

Before using any debt payoff calculator, collect the following information for each student loan:

- Current balance: Available through your loan servicer’s website

- Interest rate: Both current rate and any variable rate features

- Minimum monthly payment: Required payment amount

- Loan type: Federal vs private, subsidized vs unsubsidized

- Remaining term: Years left on standard repayment plan

Calculator Input Best Practices

Accurate calculation requires precise data entry. The Federal Student Aid website provides official loan information that should be used rather than estimates⁵. Small errors in interest rates or balances can significantly impact payoff projections.

Interpreting Calculator Results

Debt payoff calculators typically provide several key metrics:

- Payoff timeline: Total time to eliminate all debt

- Total interest paid: Cumulative interest over the loan life

- Monthly payment requirements: Amount needed to achieve goals

- Interest savings: Money saved compared to minimum payments

Integration with Student Loan Forgiveness Programs

Modern debt payoff calculators must account for federal student loan forgiveness programs, which can dramatically alter optimal repayment strategies. Understanding program integration is crucial for students considering long-term repayment plans.

Public Service Loan Forgiveness (PSLF)

PSLF forgives remaining federal student loan balances after 120 qualifying payments while working for eligible employers. According to Federal Student Aid PSLF data, approval rates have improved significantly in 2025, reaching 62% for eligible applicants⁶.

Income-Driven Repayment Forgiveness

Income-driven repayment plans offer loan forgiveness after 20-25 years of qualifying payments. However, forgiven amounts may be subject to income tax, a factor that debt calculators must consider when projecting long-term costs.

| Program | Forgiveness Timeline | Eligible Loans | Tax Implications |

|---|---|---|---|

| PSLF | 10 years (120 payments) | Federal Direct Loans | Not taxable |

| IDR Forgiveness | 20-25 years | Federal Loans | Potentially taxable |

| Teacher Forgiveness | 5 years | Federal Loans | Not taxable |

Tips for Maximizing Debt Payoff Success

Successfully using a debt payoff calculator for students 2025 extends beyond mathematical optimization to include behavioral strategies that ensure long-term compliance with repayment plans.

Automation Strategies

Automating loan payments provides both interest rate reductions (typically 0.25%) and ensures consistency. Most federal loan servicers offer autopay options that can be easily integrated into debt payoff calculations.

Windfall Allocation

Tax refunds, bonuses, and gift money should be strategically applied to debt reduction. The NerdWallet analysis shows that applying tax refunds to student loans can reduce payoff time by an average of 1.3 years⁷.

Side Income Optimization

Many students and recent graduates leverage side hustles to accelerate debt payoff. Dedicating 100% of side income to debt reduction while living off primary income can dramatically reduce payoff timelines.

“Students who use debt payoff calculators regularly—at least monthly—are 45% more likely to stay on track with their repayment goals. The key is treating the calculator as a progress tracking tool, not just a one-time planning exercise.”— Mark Thompson, Student Financial Aid Administrator at State University

Interactive Calculator Implementation Guide

🎯 Ready to Calculate Your Virginia Emergency Fund?

Skip the basic examples. Use our advanced calculator that incorporates everything from this guide:

✅ Virginia Cost Adjustments

Northern VA, Richmond, Rural areas

✅ Income Stability Factors

Stable, Contract, High-risk jobs

✅ Personalized Recommendations

Virginia credit unions & strategies

To truly master debt payoff strategies, hands-on experience with calculation tools provides invaluable insights. Rather than showing you a basic example, we’ve created a comprehensive Virginia Emergency Fund Calculator that demonstrates all the principles discussed in this guide.

Payoff Results:

Frequently Asked Questions

What information do I need to use a debt payoff calculator for students?

You’ll need your current loan balance, interest rate, minimum monthly payment, and loan type for each student loan. This information is available through your loan servicer’s website or the Federal Student Aid portal for federal loans.

Should I use the snowball or avalanche method for student loans?

The avalanche method saves more money by targeting high-interest debt first, but the snowball method provides psychological motivation through quick wins. Choose based on your personality: if you need motivation, use snowball; if you’re disciplined about long-term goals, use avalanche.

How do student loan forgiveness programs affect debt payoff calculations?

Forgiveness programs like PSLF and income-driven repayment forgiveness can dramatically change optimal strategies. If you qualify for forgiveness, making minimum payments on income-driven plans may be better than aggressive payoff. Use calculators that factor in forgiveness timelines and tax implications.

How often should I recalculate my student loan payoff strategy?

Recalculate whenever your financial situation changes significantly: new job, salary increase, additional income sources, or life changes affecting expenses. At minimum, review your strategy annually or when interest rates change for variable-rate loans.

Can I include private student loans in payoff calculators?

Yes, but private loans have different terms and no forgiveness options. Calculate private and federal loans separately since strategies may differ. Private loans often benefit from aggressive payoff due to higher interest rates and lack of income-driven options.

Key Takeaways for Student Debt Success

- The debt payoff calculator for students 2025 is essential given current interest rates and debt levels averaging $37,338 per graduate

- Choose between snowball (motivation-focused) and avalanche (savings-focused) methods based on your personality and financial discipline

- Federal loan forgiveness programs like PSLF can dramatically alter optimal repayment strategies for eligible borrowers

- Regular calculation updates and progress tracking increase debt payoff success rates by 45%

- Automation, windfall allocation, and side income dedication accelerate debt elimination timelines significantly

The debt payoff calculator for students 2025 represents more than a financial tool—it’s a pathway to freedom from the burden that affects 87% of graduates’ major life decisions. By understanding both mathematical optimization and behavioral factors that drive success, students can craft personalized strategies that balance financial efficiency with psychological sustainability. Whether pursuing aggressive payoff through the avalanche method or building momentum with the snowball approach, the key lies in consistent application of calculator insights and regular strategy refinement. Remember that every extra dollar applied to principal today saves multiple dollars in future interest, making these calculation tools invaluable investments in your financial future.

The Evolving Post Team

Expert financial analysts specializing in student debt management and educational finance policy. Our research combines federal student aid data with practical debt management strategies for college students and recent graduates.

📚 Essential Financial Resources for Gen Z

- Side Hustle Financial Management Gen Z: From Chaos to Wealth

- Best AI Financial Wellness Apps for Gen Z Remote Workers in 2025

- 401k Loan Calculator: Payment & Interest Guide 2025

- How Many Jobs Are Available in Finance ? 963K + $101K Salary

- Can You Trade In a Financed Car? 2025 Guide & Requirements

- Cryptocurrency Investment Guide 2025: Why Search Volume Jumped 112% This Year

- Healthcare Cost Financial Planning 2025: Complete Guide for American Retirees

- Emergency Fund Calculator Inflation 2025: Your Complete Guide to Financial Security

- Student Loan Forgiveness 2025: Critical Updates Every Borrower Must Know

- The $5,000 Mistake: Why 71% of Gen Z Is Losing Money to Avoidable Financial Errors

- Debt Payoff Strategies 2025 That Actually Work

- Best No-Penalty CD Rates of 2025

Official Data References

- Federal Student Aid – Student Loan Portfolio Data

- Consumer Financial Protection Bureau – Student Loan Affordability Analysis

- Brookings Institution – Student Loans and Racial Wealth Divide

- Ramsey Solutions – Debt Snowball Method Research

- Federal Student Aid – Official Loan Information Portal

- Federal Student Aid – PSLF Program Data

- NerdWallet – Student Loan Tax Refund Analysis

- American Association of University Professors – Student Debt Economic Impact