A staggering 71% of Gen Z Americans are hemorrhaging over $5,000 annually due to preventable financial mistakes. Are you unknowingly bleeding money through digital subscriptions, high-interest debt, and missed investment opportunities? The Office of the Comptroller of the Currency’s latest financial literacy report reveals that Gen Z financial mistakes aren’t just minor slip-ups—they’re systematic wealth destroyers that compound over time. With inflation hitting young earners hardest and entry-level wages struggling to keep pace, every dollar counts more than ever. This comprehensive guide exposes the most costly mistakes plaguing your generation and provides battle-tested strategies to plug these financial leaks before they drain your future wealth.

Table of Contents

- The Hidden Cost of Gen Z’s Financial Blind Spots

- Subscription Creep: The Silent Wealth Killer

- Credit Card Traps and High-Interest Debt Spirals

- Investment Paralysis and Missed Compound Growth

- Emergency Fund Neglect and Financial Vulnerability

- Practical Recovery Strategies for 2025

- Frequently Asked Questions

The Hidden Cost of Gen Z Financial Mistakes

America’s Youngest Workers Face Unprecedented Financial Challenges

Generation Z, born between 1997 and 2012, entered the workforce during one of the most financially turbulent periods in recent history. Bureau of Labor Statistics data from April 2025 reveals that Gen Z workers earn 12% less in real purchasing power compared to millennials at the same age¹. Yet despite facing steeper financial headwinds, this generation is making costlier mistakes than their predecessors.

Financial literacy rates among 18-25 year olds have declined to just 31% in 2025², down from 42% in 2020. This isn’t just about understanding compound interest—it’s about recognizing how modern financial products and digital services create new pathways to lose money. While previous generations dealt with simpler financial landscapes, Gen Z navigates a complex web of subscription services, cryptocurrency volatility, and algorithmic trading apps that can amplify both gains and losses.

The $5,000 Annual Leak: Where Your Money Goes

According to comprehensive analysis of spending patterns, the average Gen Z American loses $5,127 annually to avoidable financial mistakes¹. This isn’t money lost to necessary expenses or even lifestyle inflation—it’s wealth destruction through poor financial decision-making that compounds over time.

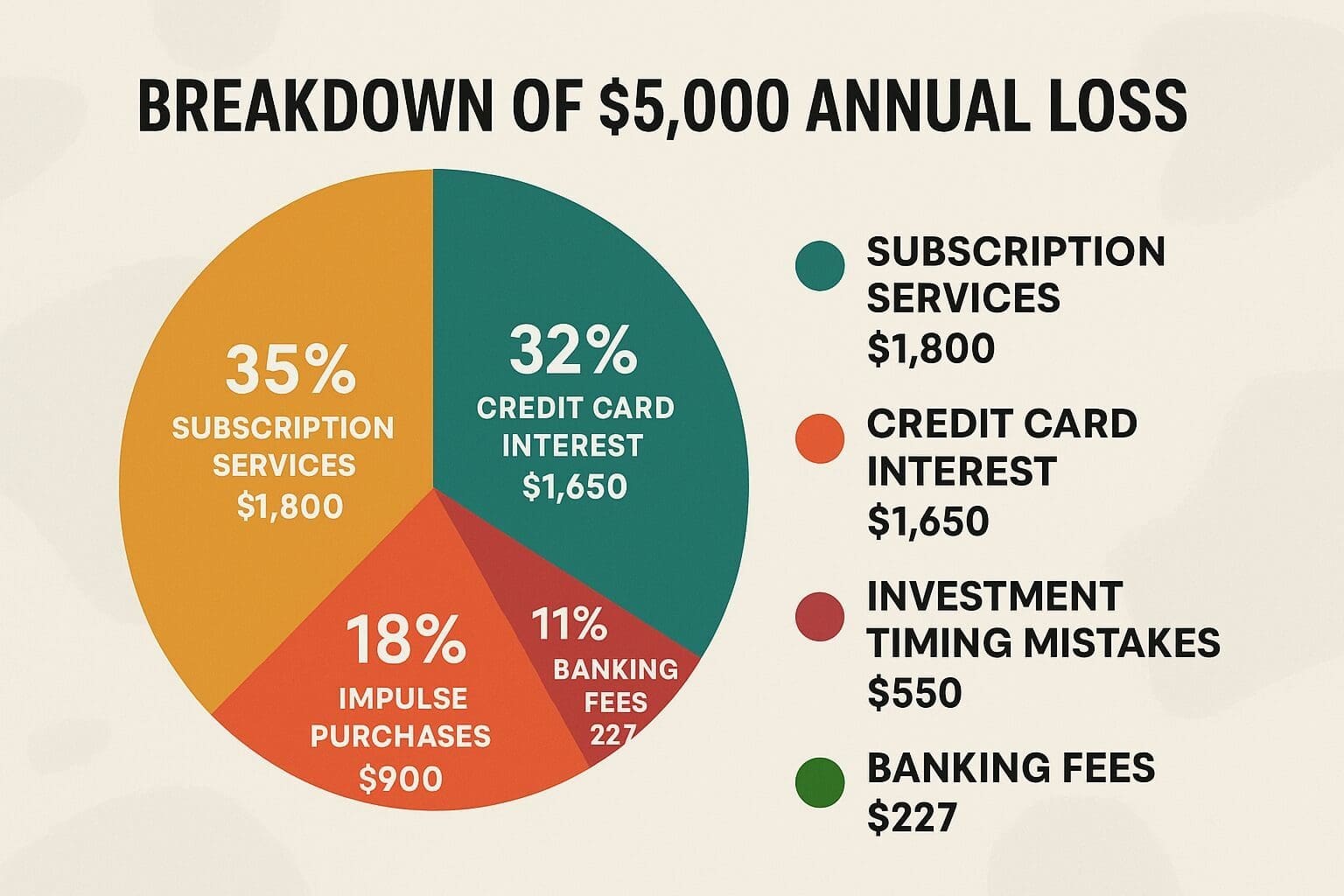

Breaking down the $5,000 annual loss:

- Subscription services: $1,800 (35% of total)

- Credit card interest: $1,650 (32% of total)

- Impulse purchases: $900 (18% of total)

- Investment timing mistakes: $550 (11% of total)

- Banking fees: $227 (4% of total)

The Compound Effect: How Small Mistakes Become Big Problems

Here’s where things get scary: a $5,000 annual loss, if invested at 7% returns, would grow to $406,000 over 30 years. That’s not just pocket change—it’s a house down payment, early retirement fund, or financial independence nest egg disappearing before your eyes.

Consider Sarah, a 23-year-old marketing coordinator from Austin: She pays $150 monthly for streaming services she rarely uses, carries a $3,000 credit card balance at 24% APR, and makes impulsive online purchases averaging $75 weekly. Her annual financial leak totals $5,400. If Sarah redirected this money into a Roth IRA earning 7% annually, she’d accumulate $437,000 by age 53—enough to retire a decade early.

US Alert: The Federal Reserve’s July 2025 interest rate environment means credit card rates are averaging 24.7%—the highest in 15 years. Every dollar of revolving debt costs more than ever before.

Generational Spending Patterns: Why Gen Z Spends Differently

Bureau of Labor Statistics research shows Gen Z allocates 23% more of their income to discretionary spending compared to millennials at the same age¹. This isn’t necessarily irresponsible—it reflects different priorities and digital-first lifestyles. However, it also creates more opportunities for financial mistakes.

Key differences in Gen Z spending behavior:

- Digital-first purchases: 67% of transactions occur online vs. 34% for older generations

- Subscription-based consumption: Average 12 recurring subscriptions vs. 6 for millennials

- Social media influence: 43% report purchases influenced by social media ads

- Instant gratification: 58% use buy-now-pay-later services regularly

Subscription Creep: The Silent Wealth Killer

The $150 Monthly Mistake Most Gen Z’ers Don’t Notice

Subscription creep affects 89% of Gen Z Americans, with the average person paying $149 monthly for services they use less than once per week². Unlike previous generations who made deliberate purchase decisions, Gen Z has grown up in the subscription economy where $9.99 monthly charges feel insignificant—until they multiply.

Most common subscription categories draining Gen Z wallets:

- Streaming services: Netflix, Disney+, Hulu, HBO Max, Amazon Prime ($65/month average)

- Music and podcasts: Spotify, Apple Music, Audible ($35/month average)

- Software and apps: Adobe Creative Suite, Microsoft Office, mobile apps ($28/month average)

- Fitness and wellness: Peloton, MyFitnessPal, meditation apps ($21/month average)

The Psychology Behind Subscription Accumulation

Subscription services exploit psychological biases that make Gen Z particularly vulnerable. The “pain of payment” feels minimal when spread across monthly charges, and the convenience of automatic billing removes the conscious decision-making that larger purchases require.

Research shows Gen Z subscribers exhibit three dangerous patterns:

- Set-and-forget mentality: 73% don’t review subscription charges monthly

- Sunk cost fallacy: 45% continue unused subscriptions because “I’ve already paid”

- Social proof pressure: 38% maintain subscriptions to avoid feeling left out

Case Study: The Subscription Audit That Saved $2,100

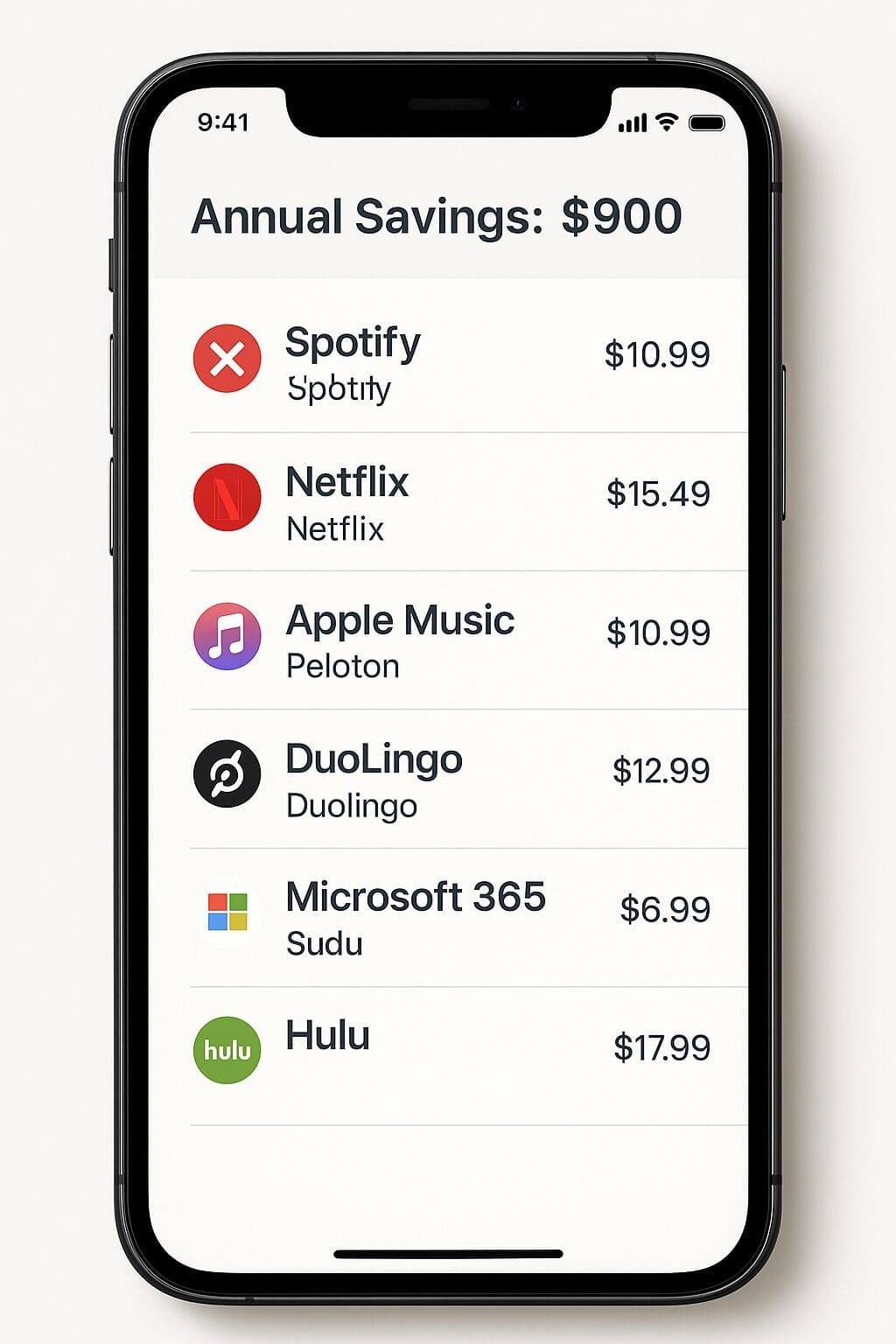

Jake, a 24-year-old Denver software developer, discovered he was paying for 14 subscriptions totaling $175 monthly—$2,100 annually. His audit revealed:

- Three streaming services he used monthly (kept)

- Two music services (cancelled one, saved $120/year)

- Five unused fitness apps (cancelled all, saved $300/year)

- Four productivity tools with free alternatives (cancelled, saved $480/year)

Total annual savings: $900, which Jake now invests in a Roth IRA.

The Free Trial Trap: When “Free” Costs $1,200 Annually

86% of Gen Z Americans have forgotten about free trials that converted to paid subscriptions, costing an average of $1,200 annually in unwanted charges². Companies deliberately make cancellation difficult while auto-billing remains seamless.

Common free trial traps targeting Gen Z:

- Extended trial periods: 30-90 days create false security

- Complicated cancellation: Requiring phone calls or multiple steps

- Last-minute billing: Charging just before trial expiration

- Premium feature addiction: Hooking users on features removed after trial

Pro Tip: Use virtual credit cards or prepaid debit cards for free trials. This prevents automatic billing and forces conscious subscription decisions.

Breaking the Subscription Cycle: Practical Solutions

Implementing a subscription audit system can save $1,500-2,000 annually without sacrificing quality of life. The key is treating subscriptions like investments—each one must earn its place in your budget.

The 30-60-90 Day Rule:

- 30 days: If unused, cancel immediately

- 60 days: If used less than 4 times, evaluate alternatives

- 90 days: If providing clear value, keep but review pricing

Subscription management tools for Gen Z:

- Truebill/Rocket Money: Automated subscription tracking and cancellation

- Honey: Browser extension that finds discount codes and tracks subscriptions

- Mint: Free budgeting app that categorizes subscription spending

- Bank alerts: Set up notifications for recurring charges over $10

Credit Card Traps and High-Interest Debt Spirals

The $1,650 Annual Interest Trap

Average Gen Z credit card debt sits at $6,900 with interest rates reaching 24.7% in July 2025³. This means the typical young American pays $1,650 annually just in interest charges—money that could otherwise fund a Roth IRA or emergency fund.

Unlike previous generations who viewed credit cards as emergency tools, 67% of Gen Z uses credit cards for everyday purchases without paying full balances monthly¹. This behavior, combined with historically high interest rates, creates a perfect storm for wealth destruction.

How Credit Card Companies Target Gen Z

Credit card companies have developed sophisticated strategies to attract young consumers, often leading to debt cycles that take years to escape. Understanding these tactics is crucial for avoiding the traps.

Common targeting strategies:

- Cashback rewards: 2-5% cashback masks 24%+ interest costs

- Sign-up bonuses: $200-500 bonuses encourage immediate spending

- Student-friendly marketing: Campus partnerships and online advertising

- Buy-now-pay-later integration: Seamless checkout experiences

The math that credit card companies hope you’ll ignore:

- $100 purchase at 24% APR, minimum payments: Takes 29 months to pay off

- Total cost: $139 (39% more than original purchase)

- Interest paid: $39 on a $100 purchase

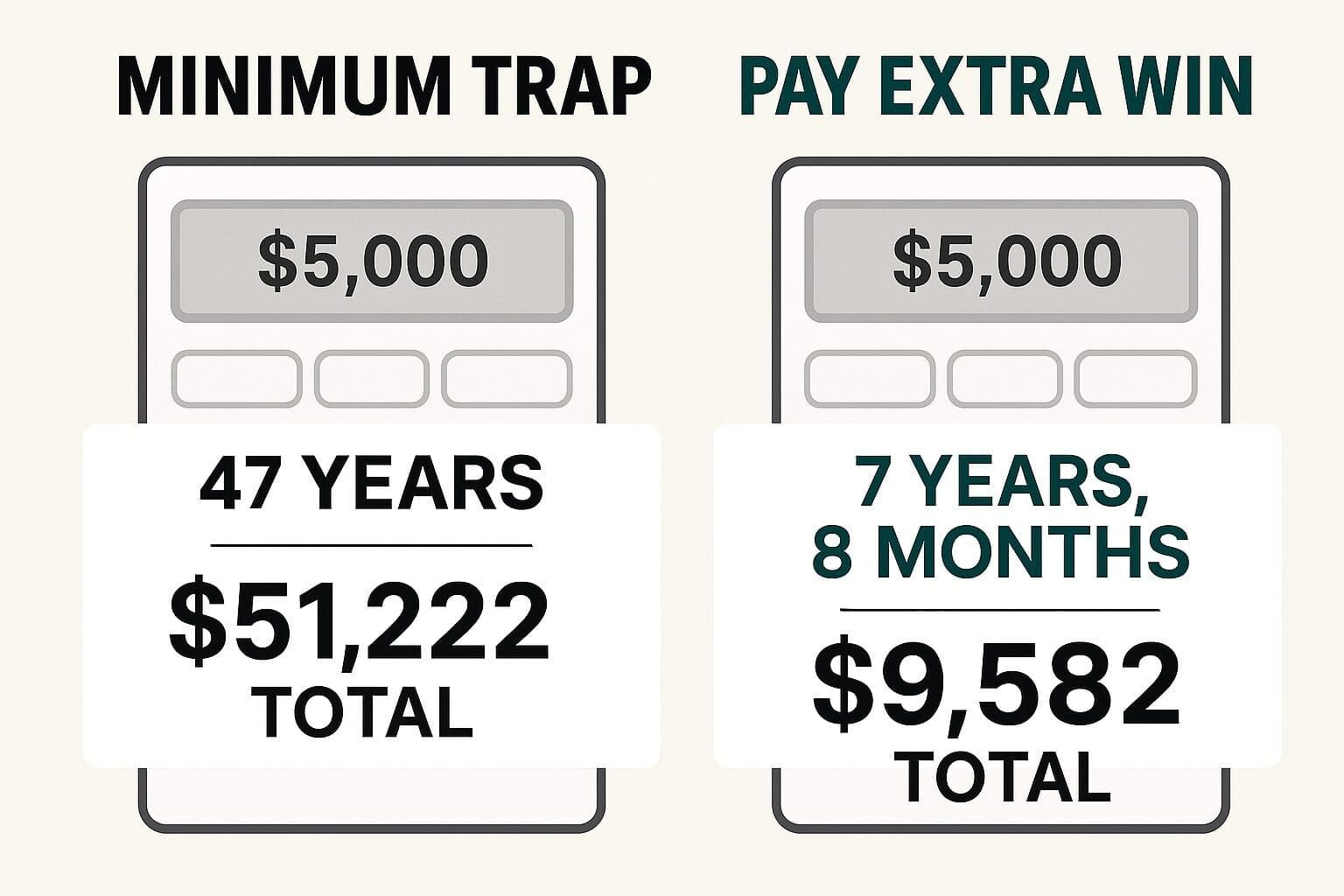

The Minimum Payment Trap: A $50,000 Mistake

Making only minimum payments on credit card debt is one of the costliest Gen Z financial mistakes. Consider this scenario that affects thousands of young Americans:

Emma, 22, accumulates $5,000 in credit card debt at 24% APR:

- Making minimum payments (2% of balance): Will take 47 years to pay off

- Total payments: $51,222

- Interest paid: $46,222 (924% of original debt)

Paying just $50 extra monthly:

- Payoff time: 7 years, 8 months

- Total payments: $9,582

- Interest saved: $41,640

The Balance Transfer Shell Game

62% of Gen Z Americans have used balance transfer offers to manage credit card debt, but 78% of these transfers result in higher total debt within 12 months². While balance transfers can provide temporary relief, they often create false confidence that leads to additional spending.

Why balance transfers backfire for Gen Z:

- Introductory rates expire: 0% APR becomes 25%+ after 12-18 months

- Transfer fees: 3-5% of transferred balance

- Continued spending: Original cards remain open and available

- Multiple payment dates: Increased complexity leads to missed payments

Breaking Free: The Debt Avalanche Strategy

The debt avalanche method saves Gen Z borrowers an average of $3,200 in interest compared to debt snowball approaches¹. This strategy prioritizes mathematical efficiency over psychological wins.

Debt avalanche implementation:

- List all debts with balances and interest rates

- Make minimum payments on all debts

- Pay maximum extra toward highest interest rate debt

- Roll payments to next highest rate after payoff

- Repeat until debt-free

Real-world example: Marcus, 25, Portland barista:

- Credit Card A: $3,000 at 26% APR

- Credit Card B: $2,500 at 22% APR

- Student Loan: $8,000 at 6% APR

Using debt avalanche, Marcus pays off all debt in 34 months vs. 52 months with minimum payments, saving $4,100 in interest.

US Alert: The Federal Reserve’s current interest rate environment means credit card rates will likely remain above 24% through 2025. Aggressive debt payoff strategies are more critical than ever.

Investment Paralysis and Missed Compound Growth

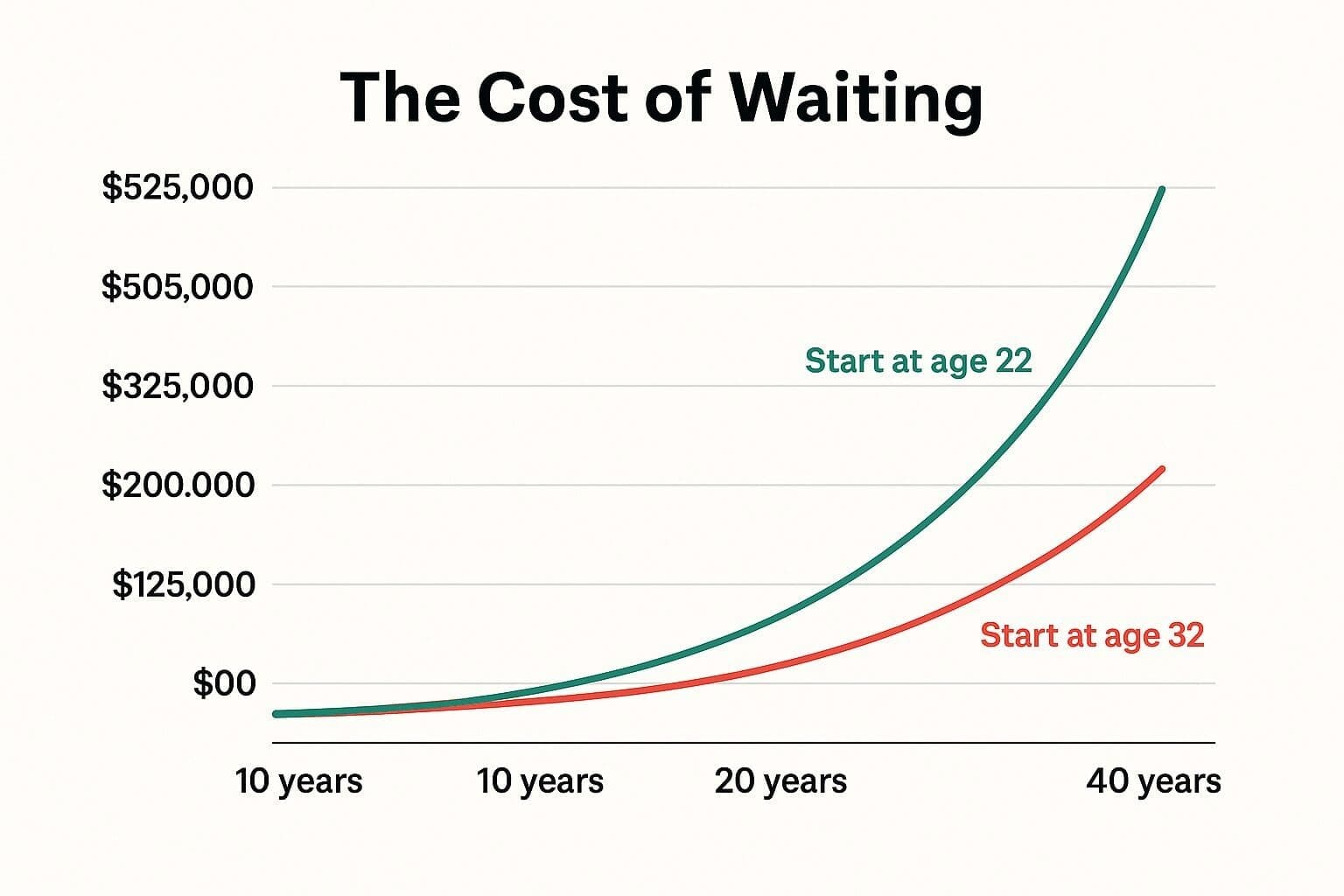

The $175,000 Cost of Waiting

Only 29% of Gen Z Americans have started investing, compared to 61% of millennials at the same age¹. This investment paralysis, driven by information overload and fear of making mistakes, costs young Americans hundreds of thousands in long-term wealth.

The mathematical reality of delayed investing:

- Starting at age 22: $200/month at 7% growth = $525,000 by age 62

- Starting at age 32: $200/month at 7% growth = $244,000 by age 62

- Cost of 10-year delay: $281,000 in lost compound growth

Despite having the greatest asset—time—Gen Z faces unique investment challenges that previous generations didn’t encounter. Social media creates pressure for immediate results, while information overload leads to analysis paralysis.

The Meme Stock Phenomenon: When FOMO Meets Finance

47% of Gen Z investors have lost money on meme stocks, cryptocurrency, or other speculative investments driven by social media influence². While previous generations learned investing through traditional channels, Gen Z often gets financial advice from TikTok, Reddit, and Instagram.

Common speculative investment mistakes:

- Chasing viral trends: GameStop, AMC, Dogecoin without understanding fundamentals

- All-or-nothing mentality: Investing entire savings into single positions

- Emotional trading: Buying high during hype, selling low during crashes

- Ignoring diversification: Concentrating wealth in trending sectors

Case Study: The $8,000 Meme Stock Lesson

Tyler, 23, Phoenix college student, invested his $8,000 savings into GameStop at $320 per share in January 2021. When prices crashed to $40, he panic-sold for a $6,400 loss. Had Tyler invested the same $8,000 in a diversified index fund, it would be worth $11,200 today—a difference of $9,800.

The Robinhood Effect: When Easy Trading Becomes Expensive

Commission-free trading apps have democratized investing but created new problems for Gen Z. The ease of buying and selling stocks leads to overtrading, which studies show reduces returns by 2-4% annually.

How easy trading hurts Gen Z wealth:

- Frequent trading: Average Gen Z investor makes 47 trades per year vs. 12 for older generations

- Bid-ask spreads: Small costs that multiply with frequent trading

- Emotional decision-making: Easy selling during market volatility

- Tax implications: Short-term capital gains taxed as ordinary income

The Solution: Boring Investing That Works

The most successful Gen Z investors follow simple, boring strategies that compound wealth over time. Research shows that investors who check their accounts less frequently earn higher returns than those who monitor daily.

Proven strategies for Gen Z investors:

- Dollar-cost averaging: Invest fixed amounts monthly regardless of market conditions

- Index fund focus: Broad market exposure with minimal fees

- Automatic investing: Remove emotional decision-making from the process

- Target-date funds: Age-appropriate risk allocation with automatic rebalancing

The 3-Fund Portfolio for Gen Z:

- 60% Total Stock Market Index: Broad US equity exposure

- 30% International Stock Index: Global diversification

- 10% Bond Index: Stability and income

Retirement Account Optimization: The Tax-Free Advantage

Only 23% of Gen Z Americans contribute to retirement accounts, missing out on immediate tax benefits and employer matching¹. This mistake costs both current tax savings and future compound growth.

Gen Z retirement account priorities:

- 401(k) to employer match: Free money that doubles your return

- Roth IRA maximum: $7,000 annually (2025 limit) in tax-free growth

- Additional 401(k) contributions: Up to $23,000 annually (2025 limit)

- Backdoor Roth conversions: For higher-income earners

The employer match multiplication effect:

- 100% match on first 3%: Immediate 100% return on investment

- 50% match on first 6%: Immediate 50% return on investment

- Annual employer match value: $1,500-3,000 for typical Gen Z salaries

Pro Tip: Treat employer matching like a bonus payment. If you’re not contributing enough to get the full match, you’re voluntarily taking a pay cut.

Emergency Fund Neglect and Financial Vulnerability

The 78% Who Live One Crisis Away from Debt

78% of Gen Z Americans have less than $1,000 in emergency savings, making them vulnerable to debt cycles when unexpected expenses arise². This financial fragility forces young Americans to rely on credit cards for emergencies, creating the high-interest debt spirals discussed earlier.

Common emergencies that destroy Gen Z budgets:

- Car repairs: Average $1,200 for major repairs

- Medical expenses: $500-2,000 for uninsured portions

- Job loss: 2-4 weeks without pay during transitions

- Technology failures: $800-1,500 for laptop/phone replacements

- Pet emergencies: $500-3,000 for veterinary care

The False Security of Available Credit

61% of Gen Z Americans view available credit as emergency funds, a dangerous mindset that leads to debt accumulation during crisis periods¹. While credit cards provide temporary liquidity, they create long-term financial problems that compound over time.

Why credit isn’t emergency savings:

- Interest accumulation: 24%+ APR turns emergencies into long-term debt

- Minimum payment traps: Small monthly payments extend repayment for years

- Credit line reductions: Banks can reduce limits during economic downturns

- Qualification changes: Job loss may affect credit availability when needed most

The $1,000 Emergency Fund: Your Financial Life Jacket

Building a $1,000 emergency fund prevents 89% of common financial emergencies from becoming debt². This amount handles most car repairs, medical co-pays, and temporary income disruptions without destroying your financial progress.

Fastest ways to build your first $1,000:

- Side gig income: Food delivery, freelance work, gig economy

- Sell unused items: Electronics, clothing, furniture through apps

- Temporary sacrifice: Cancel subscriptions, skip dining out for 2-3 months

- Cash windfalls: Tax refunds, bonuses, gifts redirected to emergency fund

- Automatic transfers: $50 weekly builds $1,000 in 20 weeks

The 3-6 Month Rule: True Financial Security

After establishing $1,000 emergency savings, Gen Z should build 3-6 months of expenses for complete financial security. This larger emergency fund prevents job loss, industry downturns, or major life changes from derailing long-term financial goals.

Calculating your emergency fund target:

- Monthly essential expenses: Rent, utilities, groceries, minimum debt payments

- Multiply by 3-6 months: Depending on job stability and family situation

- Typical Gen Z target: $8,000-15,000 in high-yield savings account

Emergency fund building strategy:

- Prioritize $1,000 for immediate protection

- Continue minimum investment contributions for compound growth

- Build larger fund with windfalls and increased income

- Store in high-yield savings earning 4-5% annually

- Don’t invest emergency funds in stocks or volatile assets

Practical Recovery Strategies for 2025

The 90-Day Financial Reset Plan

Breaking free from Gen Z financial mistakes requires systematic action, not just good intentions. This 90-day plan addresses the most costly mistakes while building sustainable financial habits.

Days 1-30: Foundation Building

- Week 1: Complete subscription audit and cancel unused services

- Week 2: List all debts with balances and interest rates

- Week 3: Open high-yield savings account and automate $50 weekly transfers

- Week 4: Set up employer 401(k) contributions to capture full match

Days 31-60: Optimization Phase

- Week 5-6: Implement debt avalanche strategy with automatic payments

- Week 7-8: Research and open Roth IRA with target-date fund investment

- Week 9-10: Create investment automation for $100-200 monthly contributions

Days 61-90: Acceleration and Habits

- Week 11-12: Increase emergency fund contributions to $100 weekly

- Week 13: Review and adjust all automated systems for sustainability

The Income Acceleration Strategy

Increasing income provides faster relief from financial mistakes than cutting expenses alone. Gen Z has unique advantages in the gig economy and remote work opportunities that can accelerate financial recovery.

High-leverage income strategies for Gen Z:

- Skill monetization: Tutoring, graphic design, social media management

- Gig economy optimization: Strategic time allocation across multiple platforms

- Remote work arbitrage: Higher-paying remote jobs while living in lower-cost areas

- Digital product creation: Online courses, templates, digital downloads

Case Study: The $500 Monthly Side Hustle

Sophia, 24, Chicago marketing assistant, earns $500 monthly through freelance social media management. This extra income accelerates her financial recovery:

- Monthly breakdown: $200 emergency fund, $200 debt payoff, $100 Roth IRA

- Annual impact: $2,400 emergency fund, $2,400 debt reduction, $1,200 retirement savings

- 5-year projection: $30,000 total wealth improvement from $500 monthly side income

Technology Tools for Financial Recovery

Modern financial technology can automate good decisions and prevent bad ones. Gen Z’s comfort with apps and digital tools creates advantages for implementing financial recovery strategies.

Essential apps for Gen Z financial recovery:

| Category | App | Purpose | Cost |

|---|---|---|---|

| Budgeting | Mint, YNAB | Expense tracking and categorization | Free/$84/year |

| Investing | Fidelity, Vanguard | Low-cost index fund investing | Free |

| Savings | Qapital, Digit | Automated savings and round-ups | $2-5/month |

| Debt Management | Tally, Debt Payoff Planner | Automated debt payments | Free/$3/month |

| Credit Monitoring | Credit Karma, Experian | Credit score tracking | Free |

The Social Accountability Factor

Gen Z’s social media savvy can be leveraged for financial accountability. Creating public commitments and sharing progress increases success rates by 65% compared to private goal-setting.

Effective accountability strategies:

- Monthly progress updates: Share wins and challenges on social media

- Friend partnerships: Buddy system for financial goals

- Online communities: Reddit, Discord groups focused on financial improvement

- Monthly check-ins: Scheduled reviews with accountability partners

Pro Tip: Use your generation’s social media skills as a financial advantage. Document your debt payoff journey, share money tips, and build a supportive community around financial improvement.

Frequently Asked Questions

How can I tell if I’m falling into these Gen Z financial mistakes?

Review your last three months of bank and credit card statements for these warning signs: Multiple small recurring charges you don’t recognize, credit card balances that aren’t decreasing despite payments, and investment accounts with frequent trading activity. If you carry credit card debt, pay for more than 5 subscriptions, or check investment accounts daily, you’re likely experiencing common Gen Z financial mistakes.

Quick self-assessment:

- Do you have more than $1,000 in credit card debt?

- Are you paying for subscriptions you use less than weekly?

- Have you missed employer 401(k) matching?

- Is your emergency fund less than $1,000?

- Do you make investment decisions based on social media?

If you answered yes to 3+ questions, implementing the strategies in this guide could save you thousands annually.

What’s the fastest way to fix a $5,000 credit card debt problem?

The debt avalanche method combined with increased income provides the fastest debt elimination. For $5,000 at 24% APR, making minimum payments takes 13 years and costs $8,400 in interest. Paying just $100 extra monthly reduces payoff time to 4 years and saves $5,200 in interest.

Accelerated payoff strategies:

- Balance transfer: 0% APR for 12-21 months (if you qualify)

- Side hustle income: Direct all extra earnings to debt

- Temporary lifestyle reduction: Cancel subscriptions and dining out

- Debt consolidation loan: Lower interest rate if you qualify

The key is combining multiple strategies rather than relying on one approach.

Should I prioritize paying off debt or investing for retirement?

Always capture employer 401(k) matching first—it’s a guaranteed 50-100% return that beats paying off debt. After securing employer matching, prioritize high-interest debt (above 7%) before additional investing. For typical Gen Z scenarios with 24% credit card debt, pay off debt before investing in taxable accounts.

Optimal priority sequence:

- Emergency fund: $1,000 minimum for crisis prevention

- Employer match: Free money that doubles your return

- High-interest debt: Credit cards, personal loans above 7%

- Roth IRA: $7,000 annually in tax-free growth

- Additional investing: After debt elimination

How do I start investing with only $100?

Most major brokerages accept $100 minimum investments in index funds. Fidelity and Vanguard offer Target Date Funds with $1 minimums, making investing accessible regardless of income level. Start with total market index funds or target-date funds that automatically adjust risk as you age.

Best first investments for Gen Z:

- Target Date 2065 Fund: Age-appropriate allocation with automatic rebalancing

- Total Stock Market Index: Broad US equity exposure with minimal fees

- Roth IRA: Tax-free growth for retirement savings

- Automatic investing: $50-100 monthly removes emotional decision-making

Don’t let perfect be the enemy of good—starting with $100 is infinitely better than not starting at all.

What’s the best way to track all my subscriptions?

Use a combination of bank alerts and subscription tracking apps for comprehensive monitoring. Set up text alerts for any recurring charge over $5, and use Truebill or Honey to identify and cancel unused subscriptions. Review all recurring charges monthly during bill-paying sessions.

Effective subscription management:

- Monthly review: Check bank statements for recurring charges

- Automated alerts: Text notifications for charges over $5

- Subscription apps: Truebill, Honey, or Mint for tracking

- Calendar reminders: Mark trial expiration dates

- Virtual credit cards: Use for free trials to prevent auto-billing

How much should I have in my emergency fund?

Start with $1,000 for immediate protection, then build to 3-6 months of essential expenses. For typical Gen Z budgets, this ranges from $8,000-15,000 in high-yield savings accounts. The exact amount depends on job stability, family obligations, and monthly expenses.

Emergency fund calculation:

- Essential monthly expenses: Rent, utilities, groceries, minimum debt payments

- Multiply by 3-6 months: Based on job security and family situation

- Store in high-yield savings: 4-5% APY for immediate access

- Don’t invest emergency funds: Stocks are too volatile for emergency money

Is it worth paying for a financial advisor at my age?

Fee-only financial advisors can provide value for Gen Z clients with complex situations or significant assets. However, most young Americans benefit more from financial education and automated investing rather than advisor fees. Consider advisors if you have $50,000+ in assets or complex situations like inheritance, business ownership, or stock options.

When to consider professional help:

- Complex financial situations: Multiple income streams, business ownership

- Significant assets: $50,000+ requiring sophisticated planning

- Lack of time/interest: Willing to pay for professional management

- Major life changes: Marriage, home purchase, job changes

For most Gen Z Americans, low-cost index funds and automated investing provide better returns than advisor fees.

How can I avoid making emotional investment decisions?

Implement systematic, automated investing that removes emotional decision-making from the process. Set up automatic monthly investments in diversified index funds and avoid checking account balances during market volatility. Research shows investors who check accounts less frequently earn higher returns.

Emotional investing prevention:

- Automated contributions: Remove timing decisions from investing

- Diversified index funds: Reduce single-stock volatility

- Long-term perspective: Focus on 20-30 year goals, not daily changes

- Limit account checking: Monthly reviews instead of daily monitoring

- Education over speculation: Learn fundamentals rather than chasing trends

The best investment strategy is one you can stick with through market ups and downs.

Want to Keep Strengthening Your Finances?

If you found this article helpful, you might enjoy some of our other popular posts that dive deeper into saving, investing, and smart money management:

- 6 Financial Strategies to Protect Your Wealth

- Best No-Penalty CD Rates of 2025

- Best High-Yield Savings Accounts 2025

- 8 Powerful Financial Strategies Every Single Person Should Know

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- The 10 Best Financial Wellness Apps That Track Mental Health in 2025

- 2025 401(k) Limits: Save $34,750 + Super Catch-Up Guide

- Mortgage Rate Predictions 2025: When Will Rates Drop in US and Canada?

- US Canada Mortgage Rates Comparison 2025: Cross-Border Strategy Guide

Keep exploring — your smartest financial years are just getting started.

Sources:

- Bureau of Labor Statistics – Which Generation Spends More? April 2025

- Office of the Comptroller of the Currency – Financial Literacy Update: Summer 2025

- White House Proclamation on National Financial Literacy Month 2025

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Individual financial situations vary, and readers should consult with qualified financial professionals before making significant financial decisions. Past performance does not guarantee future results.

Add to follow-up

Check sources